As promised, entire long term debt is repaid by company…

32ee2941-5963-42db-a466-1d3296997a0b.pdf (478.8 KB)

7 Likes

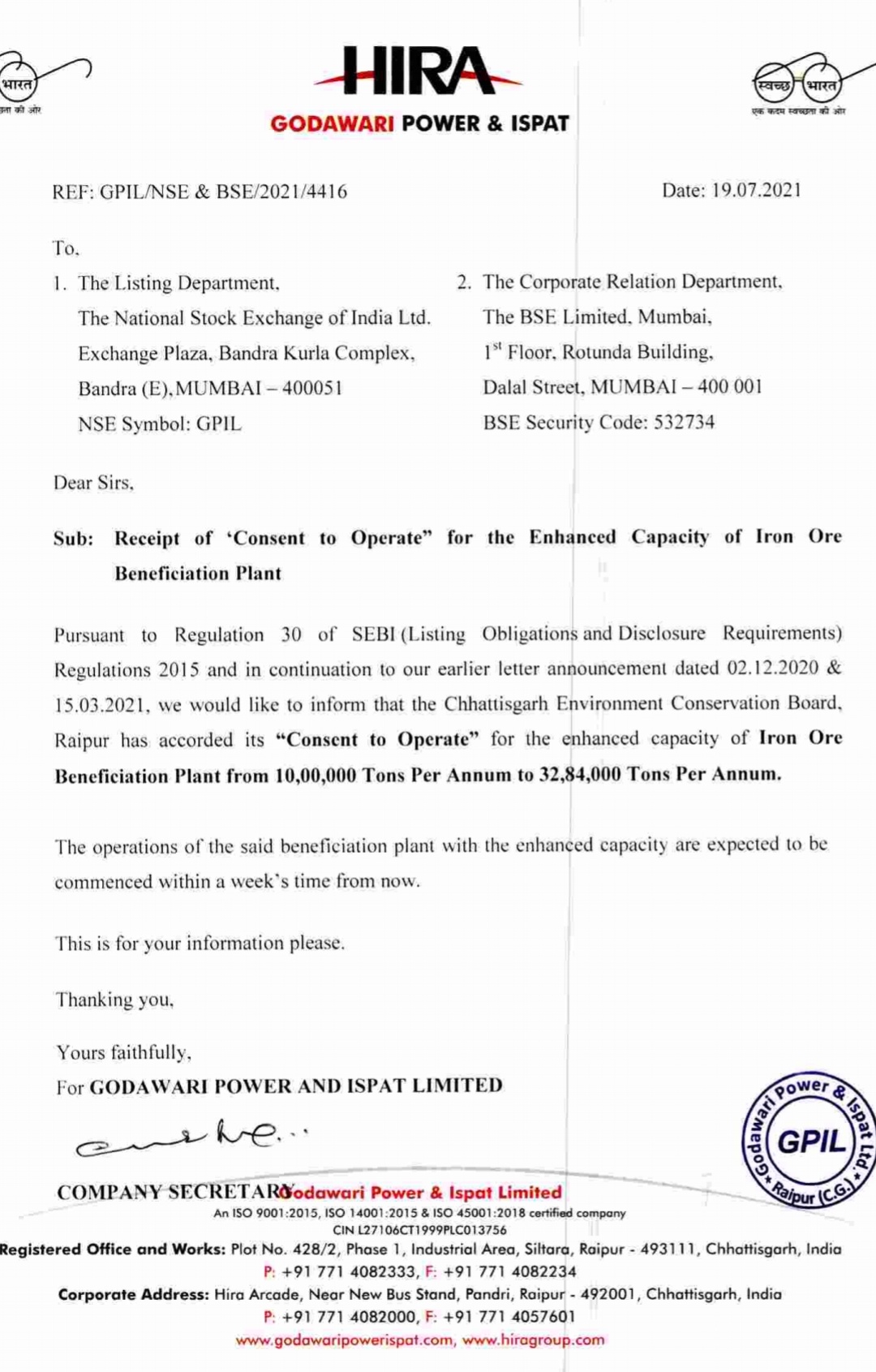

Iron ore beneficiation plant capacity has been increased as promised. Operations of enhanced capacity to be commenced within a week.

5 Likes

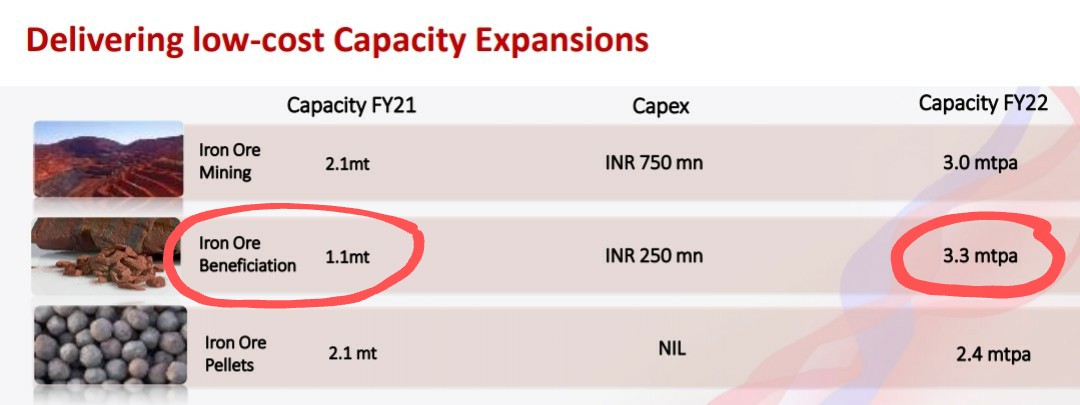

Some highlights from the investor presentation aside from the numbers:

-

Pledged promoter holding likely to be released in Q2FY22 as there isn’t any more long term debt.

-

Setting up an integrated steel flats plant under the PLI scheme, with a capacity of 1.5 - 2 million tonnes, and expenditure of 3000 - 4000 crores. I assume it’s the same MoU that was spoken about in the last concall, and higher up on the thread. Hoping for more details on the PLI scheme from the concall.

-

NCLT hearing has been concluded for the proposed merger with Jagadamba power (from 2017). Convening meetings with creditors before posting updated financials.

-

Have acquired 56% stake (8% more than currently held) in Hira Ferro Alloys in order to finance 70MW solar power captive plant.

5 Likes

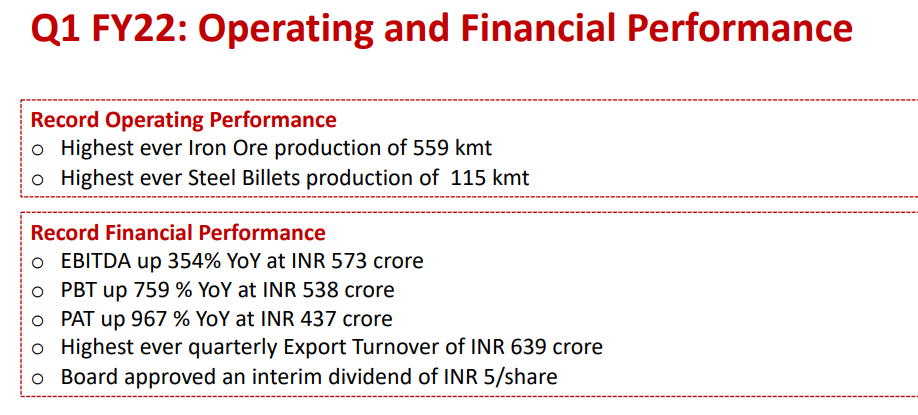

Highlights from the concall, and always nice hearing familiar Valuepickr seniors asking questions.

- Prices are currently a few ticks higher than in Q1. Q2 mining will be in line with Q1.

| Product | Current | Q1FY22 | Q4FY21 | Q2FY21 |

|---|---|---|---|---|

| Iron Ore Pellets | 15,250 | 13,942 | 10,365 | 7,059 |

| Sponge Iron | 29,000 | 28,693 | 24,591 | 17,854 |

| Billets | 42,500 | 41,292 | 38,386 | 29,298 |

-

Coal prices are up significantly, but management has been smart and has planned additional inventory until November, and will not be affected.

-

For the 3000 crores of capex, since they are currently debt free, will try to maximise internal accruals. Should there be a need for debt, it will not be substantial. Land has already been identified, environment clearance is going on, will announce complete plans in Q2.

-

The new integrated steel plant will focus on API grade of steel, used in oil/gas transportation, and coated steel, used in roofing. Aiming for the 4-12% PLI bracket.

-

Solar plants will significantly bring down operating costs, in the range of 50p per unit, compared to 5.50 rupees per unit from the grid.

-

Captive costs of iron ore going forward will be around 3,000 per ton.

-

After clearances, will have a higher contribution of 70% from high grade pellets, from around 45% at the moment. This is roughly 7-8% higher revenue, and are hopeful that it will increase with brand recognition.

Disclosure: invested

13 Likes

Thanks, though ore/pellet prices have tanked in last few days on China steel production cuts. Since GPIL is a small player in global context as Rakesh mentioned above, don’t think it’s a material impact on sales volumes but realization will likely be lower than Q1 if this sustains. Q3 onwards, I assume domestic volumes should balance this somewhat when construction picks up. Views invited

5 Likes

In the quarter gone by (Q1FY22), how many months were they operational, all three months or less ? I am asking this to estimate if we can see more volume growth from here.

1 Like

At present pellet prices are ruling at 10% premium to Q1 prices. So I do not anticipate any dip in realisation for Q2 at least. From Q3 onwards, we will have to track development in China and how unlocking goes forward World over. That will be a worse can scenario. Moreover, Q1 production was more than 10% below Q4 of last year. With higher production capacity coming on, Q2 earning looks positive.

3 Likes

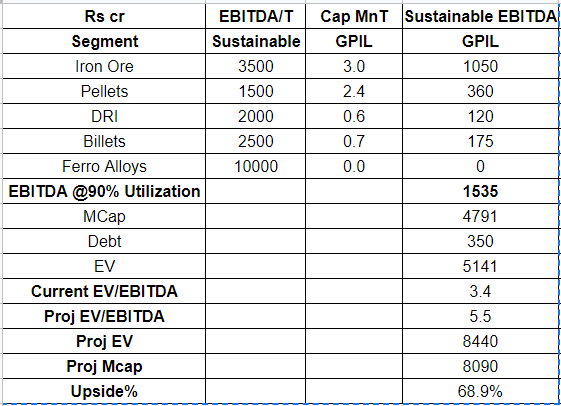

@Rakesh_Arora with ore prices falling sharply and since most of the triggers (CAPEX or clearances) are either already live or will be live shortly, I tried to come up with a revised valuation estimate based on your model. Have assumed slightly higher sustainable ore margins (6300-2800=3500/T)

Margin of safety factors - 90% capacity utilization, higher realization of beneficiation, HFAL contribution, ignored solar PV benefits from FY23, EV multiple of 5.5 vs 6

Assuming ore prices crash to 6300/T, this still suggests sustainable EBITDA of 1500cr+. Your thoughts on whether this sounds fair or if I may have missed something?

14 Likes

Seems right except that take iron ore capacity at 2.6 or so. While approval is for 3mnt but production will be less. Also remember that they have merger of Jagdamba power coming up which would mean 9% equity dilution.

5 Likes

@Rakesh_Arora Sir,

What is the annual power requirement of the Company.

- The Company is operating 73 MW of captive power generation

capacity out of which 42MW is waste heat recovery, 11 MW

thermal coal based and 20 MW bio mass power. The overall

production volumes increased marginally by 1.49% as

compared to previous year. In addition to same the Company

has long term contract for supply of power with Jagdmaba

Power & Alloys Ltd (under merger with the Company) to meet

long term power requirement of the Company

Also the Company is coming up with Solar project of 250 MW.

Would like to know your view on the valuation in which merger of Jagdamba Power and equity dilution is being made by Company.

Further

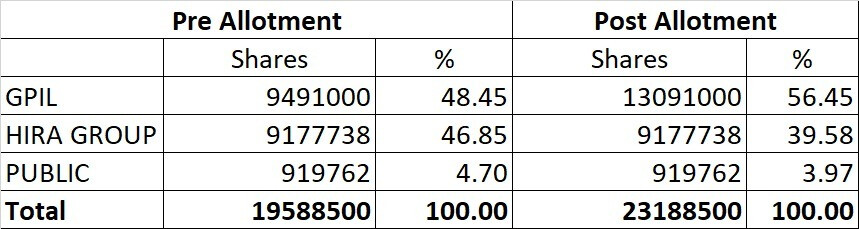

Increasing stake in Associate company Hira Ferro Alloys limited (‘HFAL’) to 56.45% from 48.45% currently by subscribing to preferential issue of Rs70cr. To be utilised for setting up captive Solar power plant. Hira Ferro Alloys to turn into subsidiary of GPIL.

Is the valuation of Hira Ferro Alloys (around Rs 875 Cr ) justifiable.

(sales FY 20-21 Rs 314 C and PAT Rs 21.13 Cr i.e PE of 41.41)

1 Like

Current power requirement of the company is 100MW and it will increase by another 30MW with expansion of Billet capacity. The upcoming 250MW will generate around 45MW of power and this will be used to feed the additional 30MW requirement and replacing the inefficient 11MW thermal coal based power. Jagdamba Power becomes critical to the company as it’s 50% cheaper than grid power and secondly, due to pollution limits, no approvals are being given for thermal coal based power plant in Raipur. The valuations are looking a bit rich given current GPIL stock price but this merger was decided almost 2years back. Management has to honour the commitment. However, it will come up for shareholder vote, so they will have a say in deciding this.

Hira Ferro Alloys valuation pre money is Rs380cr and post infusion of Rs70cr has become Rs450cr. Apart from highly profitable ferro alloys business, it also holds 12lac shares of GPIL which today is worth Rs170cr. Below is the shareholding of Hira Alloys and transaction happened at Rs195/sh of HIra Alloys

6 Likes

Thanks for your clarification …Regarding Jagdamba I remember that merger was proposed around 3 years back also when GPIL shares were trading at around Rs 550. The merger was finally not approved by Jagdamba management as there was a fall in share price of GPIL from peak to around Rs 200. I think now its GPIL shareholders turn to disapprove this demerger.

I agree that Environmental clearence will not be given for any Coal based power plant in Raipur, however in todays world it does not amke sense to invest in thermal power. Instead of diluting its equity for acquiring thermal asset it can come up with QIP and go ahead for enhanced capacity of solar plant. Company has already advised that they are getting a good ROCE in soar project and it is in the direction of clean and green energy.

3 Likes

Dear @Rakesh_Arora ,

Listening to the JSPL Management interview on BloombergQuint , it seems that there are currently few headwinds for steel/iron ore exporters

- Logistics delays with inventory stuck at various Indian ports , it was mentioned that some countries have imposed a “quarantine” policy around ships from Indian locations which has affected the WC as well . Wouldn’t this be an issue for GPIL given they export a significant chunk of pellets ? If the end customer cant receive this stuck raw material/pellets is there any risk of contract cancellation or is this risk more about the sales getting shifted by few quarters till the time this whole issue is sorted out ?

- The interview also mentioned that his view is iron prices are on a decline (down from $220/t to $160/t) , so with pellet prices correlated with iron prices and with bulk of the current Ebitda accounted by pellet segment , can this be another reason for the current Mcap softness ? I think the sooner the company commences its pellet to steel (value-addition) operations this volatility will go away . Is this the way to interpret this situation ?

Thanks , enjoy your crisp commentary around some of these commodity names

1 Like

Both are true to some extent. On logistic delays, haven’t had much feedback, GPIL does 1-2 ships a month so not big quantities in global context. All sales are FOB India, so it is sold once loaded. And it’s cargo by cargo sales, not long term contracts, so chances of any cancellation are very slim. Domestic demand is picking up, so in any case sales will shift more towards domestic market.

On iron ore prices correcting, pellet prices are also correcting but at a slower pace. However Q2 is already sold, so impact will be in Q3.

8 Likes

Grant of Permission to Establish cum Consent to Operate received by the

Company from Chhattisgarh Environment Conservation Board for

enhancement of Iron Ore Production from 1.405 MTPA to 2.35 MTPA for Iron

Ore Mining in Ari Dongri.

Consent.pdf (186.1 KB)

4 Likes

As per todays steel Mint report the prices have further been lowered by Rs 1200/t by GPIL. Fresh offers are being given at Rs 12300/T.

The fall seems to be steeper then the rise was.

4 Likes

Hi, do you have the report/link? can you please share?

Thanks,

Kumar