Godawari Power and Ispat Ltd has informed BSE that a meeting of the Board of Directors of the Company is scheduled to be held on September 14, 2021, inter alia:

To Re-consider the Scheme of Arrangement of Godawari Power and Ispat Limited with Jagdamba Power and Alloys Limited.

To consider the proposal for sub-division / split of the equity shares of face value of Rs. 10 each of the Company in such manner as may be determined by the Board of Directors.

To consider the proposal for Issue of Bonus Shares;

Further, pursuant to Company’s Code of Conduct for Regulating, Monitoring and Reporting Trading by an Insider and SEBI (Prohibition of Insider Trading) Regulations, 2015, ‘Trading Window’ for dealing in securities ofthe Company will remain closed from September 08, 2021 to till 48 hours after the conclusion of the Meeting of the Directors / KMP and other designated

employees etc. covered under the Code.

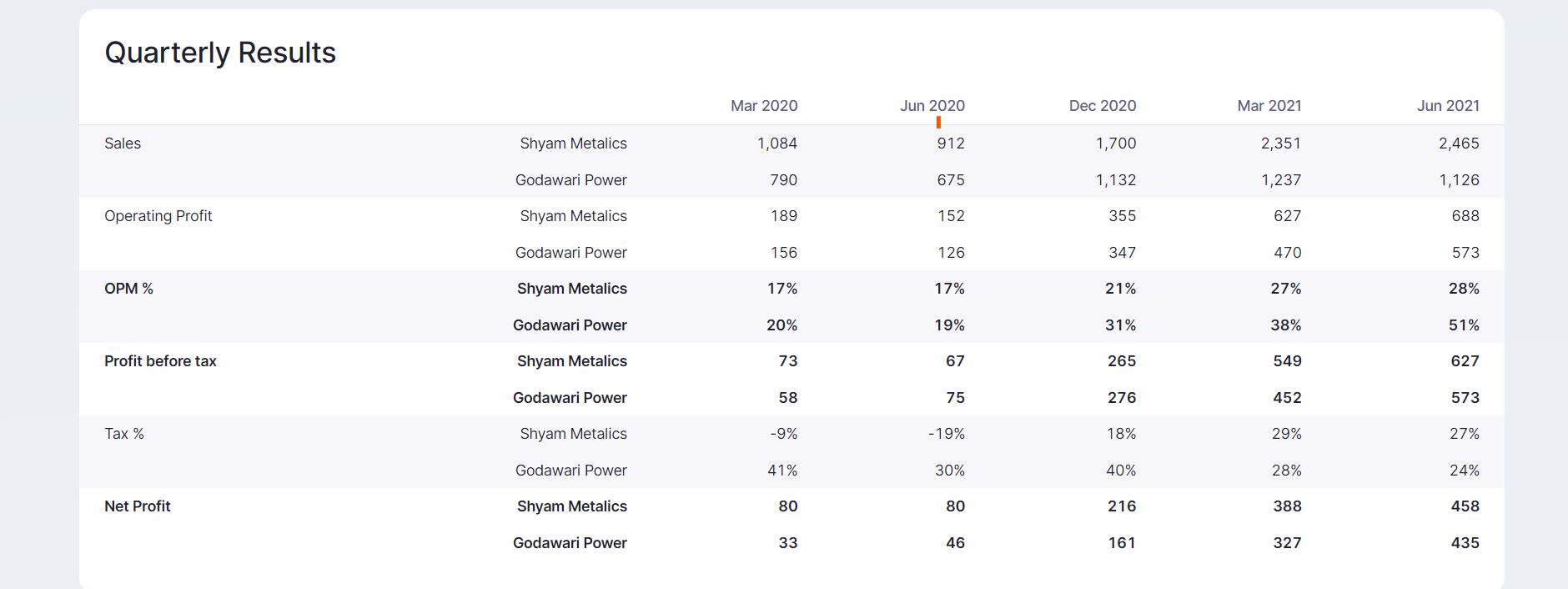

I have compared Shyam and GPIL QoQ basis, and if you see operating profit or Profit before Tax of GPIL is 10-20% lower than Shyam in most quarters. In one or two quarter, GPIL is higher than Shyam.

GPIL is debt free while shyam is not.

So, why is market cap of Shyam more than double of GPIL?

Both are pretty comparable businesses with very similar nature of business.

If their operating profit and profit before tax is in 10% range for many quarters, then why is mkt cap 110% away?

Thank you, but even existing cos like sarda energy have higher valuations than GPIL.

In addition to these profits, GPIL also is a call option on iron ore prices. Shyam or even Sarda (buys 50% iron ore from outside) don’t have this call option upside on iron ore prices.

Also, GPIL has low depreciation and is debt free compared to Shyam.

So, it should rather get higher valuations.

Yesterday, the promoters came on TV - https://twitter.com/blitzkreigm/status/1438030574665408512?s=20

Even now, they are getting 12000 value for pellets in exports because they produce high iron pellets and 11500 in domestic market.

This translates to EPS of 100-110 range per quarter (interest cost will be zero now), or 400-450 annual EPS.

I don’t think any other company is at such low valuations.

Morever, they will be having a big specialty steel plant in place by 2025 which is likely to increase revenues and profits substantially.

No other company like sarda or Shyam are doing such a massive capex and GPIL will be funding the capex by internal accruals most likely as it has very high free cash flows because of zero debt and low depreciation/maintenance capex unlike other steel companies.

One of the major reason for this could be the past Management Quality Issue. Earlier management has taken some decisions which we can say is not very transparent -

Earlier they were divesting GGEB stake which was being done at lower valuations now they have cancelled

JPAL earlier plans of divestment and then amalgamation with GPIL now

Also, have read somewhere about the thrift personal spending of the promoters earlier and some fishy transactions done in the past.

GGEB divestment was being done at 650/675 cr, which is actually a very fair price. In comparison, they are buying 22% stake in just 57 crores. So, sale price looks very good in comparison.

JPAL merger deal was done when stock price was at 150-180 range, so 233/share price was fair then. The stock price rose later because iron ore price rose and debt reduced. Nobody knew that iron ore price will rise in 2020-21 and stock will become 7x from deal price. The merger price was arrived SEBI formula based on avg mkt price.

The promoters have been very transparent for last few years, and share all details in their investor presentation and concalls.

The details were very granular when stock price was at Rs. 150, and are still very granular, when stock price is at Rs. 1400.

However, even at Rs. 1400, it remains so cheap at current valuations, that I can’t find a cheaper stock in the market, and that too for a debt free company that is doing a very big capex from internal accruals in next 3 years.

wrong fact. GGEB was divesting on higher valuation. Management was expecting 675 cr+ but buyer was looking to buy stake on 600 cr. It is good decision to cancel disinvestment plan.

There is no idea about fishy transaction etc now company is performing well and doing good for shareholders.

As far as i know, company stuck in debt trap and was unable to pay interest. it got turnaround in this steel cycle and managmenet paid off all debt before starting new capex. Now managment is very clear and saying will do in phase wise through internal accruals. Even Company has approved to install 750 MW solar plan on its own land to reduce operating cost. It’s good decision for long term to survive in any bad cycle for a debt free company.

So, why is market cap of Shyam more than double of GPIL?

Both are pretty comparable businesses with very similar nature of business.

If their operating profit and profit before tax is in 10% range for many quarters, then why is mkt cap 110% away?

The enigma remains!

If steel plant works out well, the EPS in 2025 may touch 800 per year. As, it is a 1.5 million ton specialty steel plant. They will share detailed plans soon. This is just my hypothesis. Actual can be higher or lower.

However, next 5 yrs growth is likely to be 20% CAGR atleast due to this steel plant in my view.

We are getting this company at 1350/400-450 = 3 PE and it is likely to grow at 20% CAGR for next 5 yrs.

Either, my calculations are crazy or markets are crazy!

I think, for commodities PE is a wrong metric. You should look at Price to book. PB currently at 2.31 which is the highest ever in the history of the company

The key earnings of GPIL come from license to iron ore mine. It is an intangible asset like a patent.

That license value is not accounted in book value.

Hence, price to book will not be a fair metric here.

Also, book value in 6 mths (end of current financial year), will be 1000+ (current book value is 578), so it is trading at 1.3 Price to book, (without accounting for license to iron ore mine), and 3 PE right now.

Probable reason for valuation gap was addressed by Rakesh earlier - “I think market assumes that GPIL profits are going to be more volatile as they are driven by iron ore prices whereas some of the other peers are just convertors and can have more stable margins. Eventually earnings will decide who trades where”. Another factor could be ‘perceived’ capital misallocation by entering specialty steel segment as they don’t have any prior expertise in that

Aside, I’m actually quite surprised at GPIL’s current pellet realization spreads - despite ore crashing to 6500 levels, they claim to have orders at 12000+. If this persists, I wouldn’t be surprised if they easily do 2000cr+ EBIDTA in FY22

Even when iron ore prices were low, 2018-20, the difference of operating profit between shyam and GPIL was consistent at 10-20% range.

You can check from my post above in year on year comparison.

On the other hand, having license is like having an additional call option of massive upside when iron ore prices rise, which shyam does not have.

Plus points of GPIL over shyam-

Debt free

Low depreciation

Iron ore mine license

Huge specialty steel plant coming up in 3.5 yrs, which will likely double revenue/profits.

Plus point of shyam-

10-20% higher operating profit (consistent difference over last 4 yrs, and 6 quarters)

However, Shyam has 2.2x mkt cap vs GPIL. Why Shyam would have 10,400 cr mkt cap for nearly the same profits, also have debt, high depreciation and no big growth plans.

Also, note that no decent company trades at 3 PE even in commodity stocks.

We have examples of Rain ind, HEG, Graphite, Coal India, MOIL, Maithan Alloys, IMFA, and many others.

Attaching image for year on year comparison (even when iron ore prices were low, GPIL was still making same 10-20% lower profits than Shyam)

Yes, however, this 13000 pellet range may not come again.

My calculations in this post Godawari Power - Any Trackers? - #227 by Kumar_manas are done on the basis of current pellet prices they are getting- 12,000 for export and around 11300-11400 in the domestic markets based on the TV interview yesterday only.

At peak pellet prices touched 16500.

The 3 PE calculation are based on current low prices, and not based on peak prices.

In addition, GPIL also sells Billets and Wire rods, prices of which remain high. GPIL is also expanding capacity of billets from 0.4mt/annum to 0.7mt/annum in next 3 months- this will reduce dependency on pellets and increase sales of high margin, high priced stable steel products.

Also, in my view for current quarter results, GPIL Net profit should be higher than Shyam metalik profits for the first time ever. There is not much difference anyways between the two, except the market cap.

Main problem is that higher pellet price was temporary. and now price are getting stabilised and where it will get stabilised we don’t know. This quarter or may be one more quarter they might avoid effect of price erosion but after that profit will certainly get hit.

It will be good if anyone can estimate the profit at pellet price around 5k-6k level. I think at that level also they will be able to generate profit of around 700 cr plus with current capacity and 1000 crore Plus with extended capacity of iron ore…

Article almost 2 years back

Article almost 2 years back