Hi karan, debt repayment will be made out of cash generated from business, so in stead of forming part of assets, this surplus will be deployed towards prepayment of debt. So its neutral event for price to book value. Its earnings, which will drive book value going forward with each of the quarter results…

1 Like

As per Goldman Sachs note - "The price dip after warnings from Beijing about speculation is a “clear buying opportunity,”

2 Likes

Hi, very insightful discussion here

@Rakesh_Arora I had a few queries based on my initial research, would love your inputs:

- How do we periodically track key pellet export customers to evaluate geopolitical risks? Are these typically spot or medium term contracts

- Recent reports that China is looking to increase steel production & also gradually move into more efficient BF operations seems to be a tailwind for Godawari vs headwinds for other domestic steelmakers, is that assessment correct?

- Does Godawari compete with other integrated players for pellets in domestic market? If yes, how does it stand vs them once domestic demand recovers?

- Major question post deleveraging would be around capital allocation. You mentioned somewhere that GPIL is looking to add additional flat steelmaking capacity at much cheaper CAPEX/t vs greenfield. Assume this would be enabled via distressed asset acquisition?

- Do your sustainable blended 800cr EBIDTA calculations account for high-grade pellets, captive mine expansion, divestments, new CPP? If not, what’s your current estimate factoring these?

Disc: Invested but looking to significantly increase exposure on dips

1 Like

- Godawari is a small fish in the ocean, total global iron trade is 1.5bnt and pellet trade is 140mnt. India total exports are not even 5-6% of global trade. Godawari does spot contracts with deliveries due in next 30-45 days. Buyers mixed between China, Korea, Japan and Middle East. Basically quantity is so small their is little customer risk.

- To reduce carbon footprint, the only way is higher grade iron ore and pellets. Coke consumption goes down.

- The market is very large as we discussed in point 1. No competition, but Godawari has the best quality pellet 65-66% Fe content and low alumina. It commands a premium of US$10-20/t over other sellers from India.

- The announced plans for capex are Rs750cr for captive solar power plant of 250MW to be completed in next 2yrs. In addition they have announced MOU for sponge iron and steel making worth Rs4000cr or so. But these MOUs have no time frame and will depend on land acquisition and environment clearances, so no capex is envisaged over next 2years atleast. They did bid for MSP Steel Rs417cr in Orissa but they lost out to winning bid at Rs470cr. Just shows that they are very cautious in committing capital.

- Rs800cr is based on Rs7000/t pellet price. No it doesn’t include gains from high-grade pellet and mine capex or divestments. This is our disclosed estimate. I will not 2nd guess the benefits, will include once they achieve it.

Buying is your decision. Please note that we are consultant to GPIL so do your own research before taking any decisions here.

15 Likes

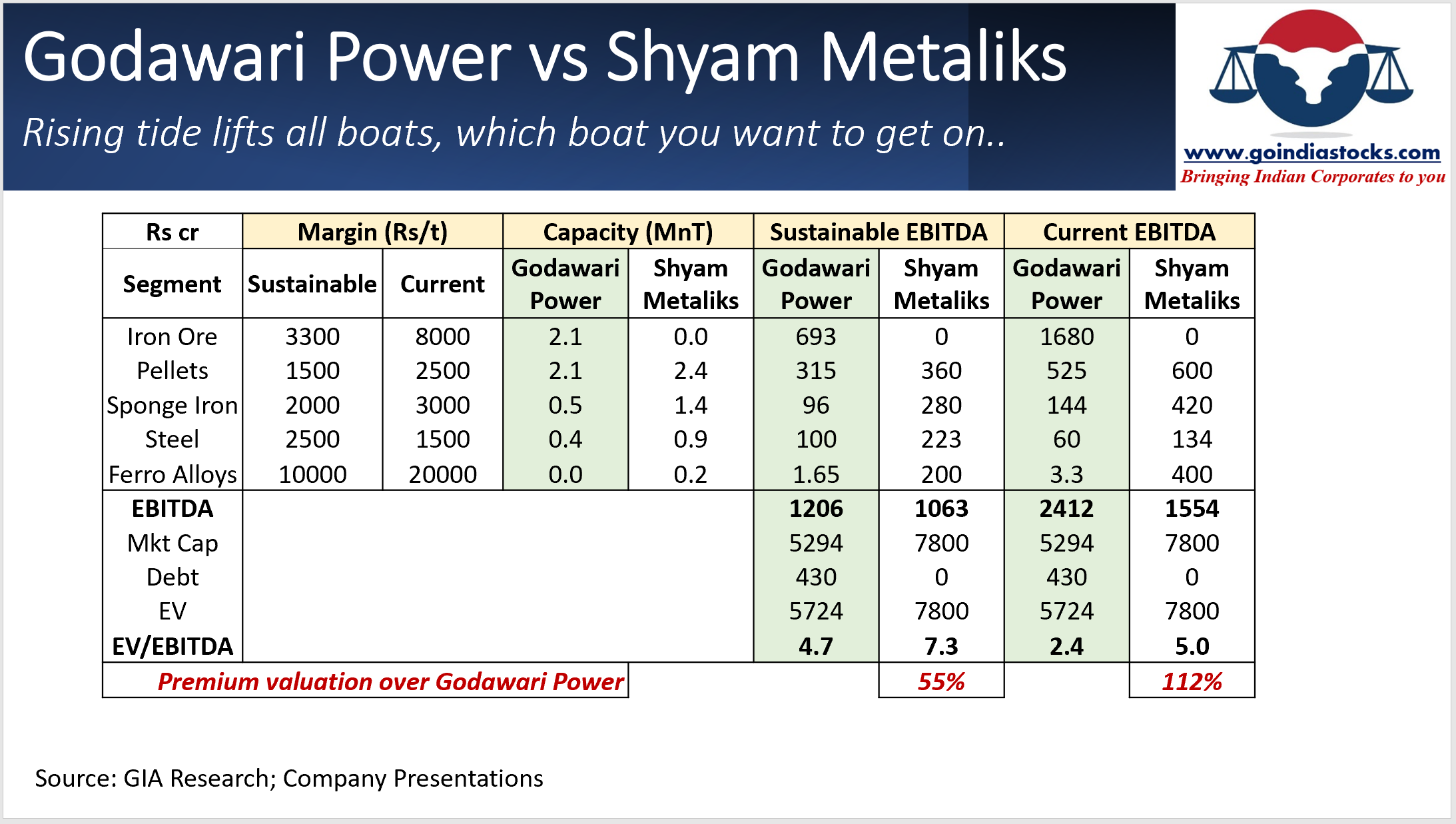

@Rakesh_Arora Sir can you give your expert comparison between shyam metallics and Gpil on basis of operation , valuation, future sustainability of earnings if iron ore prices comes down to more sustainable level and also extent of integration and timing of leases ??

Thanks in advance sir this Willi help everyone understand extent of overvaluation of upcoming ipo and step treatment with listed peers …

2 Likes

24 Likes

Thanks @Rakesh_Arora, this is super useful for a quick comp study, also good to see that you’ve substantially raised sustainable EBITDA estimate for GPIL  , assume you’ve now factored in higher pellet prices & capacities

, assume you’ve now factored in higher pellet prices & capacities

-

Though was wondering whether it’s fair to simplistically assume same margins for both given GPIL’s significant captive mining advantage? Does SMEL have other strategic locational or RM (CPP) or logistics (captive railway siding) cost advantages to offset this?

-

Also, shouldn’t the debt figures be reverse? I’m assuming GPIL will clear all debts H1FY22 whereas SMEL will still have ~500 cr debt post IPO

-

Is it fair to assume 100% util on sustainable basis? GPIL might have buffer with added FY22 capacity but can we assume same for SMEL

Even with the recent runup, GPIL still seems much more attractively priced. SMEL IPO seems to have unlocked value discovery for GPIL but will it be able to command 6X+ multiple remains to be seen

7 Likes

Sustainable margin has gone up as we assumed higher iron ore production and slightly higher iron ore prices. It is indeed very simplistic assumptions but won’t be material to change things significantly. Btw the major advantage of iron ore for GPIL is separately captured. Debt for SMEL is also for capex which would lead to higher earnings so not fair to add that.

See have given an idea, built on it to make your own decision.

8 Likes

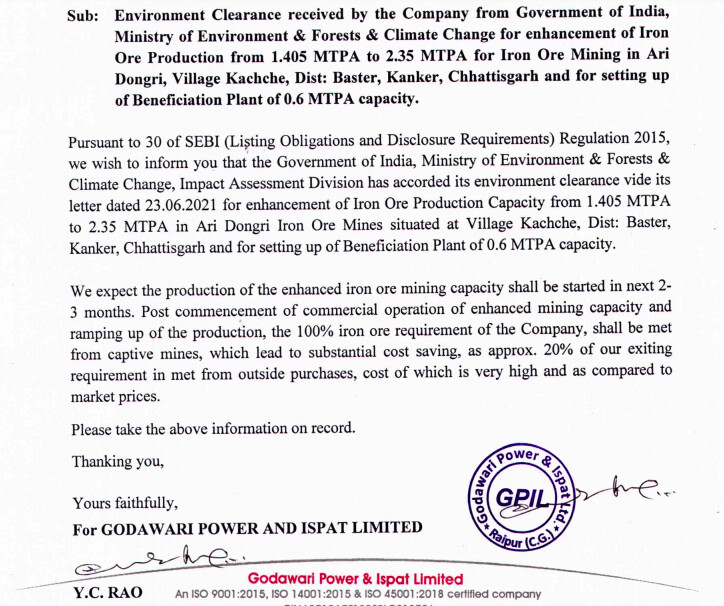

@Rakesh_Arora ,Your views on the valuation impact of the Company due to current development on enhancement of Iron ore mining.

1 Like

@VALUE2017 overall mining capacity of GPIL will go up from 2.1mnt to 3mnt. Their cost of mining + transportation to their plant comes to around Rs2200-2400/t. Current market rate is closer to Rs9000/t. Even longer term I think this will not come down below Rs5500-6000/t. So you can calculate the advantage.

4 Likes

@Rakesh_Arora how much of the extra mining capacity can we assume can be utilized to calculate EBIDTA benefit given current beneficiation and pellet capacities limited to 1.1 and 2.4MTPA? Have limited knowledge of process value chain and conversion factors from ore to pellets

@Piyush_Anand they are increasing beneficiation capacity also from 1.1mtpa to 3.3mtpa. And pellet capacity from 2.1mtpa to 2.4mtpa currently. So one can assume 2.4mtpa for near future. GPIL did 1.7mnt of iron ore production in FY21, so in FY22 we can assume 2.4mnt, an increase of 0.7mnt

3 Likes

If I make a calculation - EBITA expected for 2021 is 2.4(capacity at 100% utilization) * (6000(avg. cost assumed per ton) - 2400 (cost) = 8,640 Cr. Whereas current market cap is ~ Rs. 4,700 Cr. Even with conservative price estimates, current market cap is at 0.6 time EBITA. @Rakesh_Arora - Am I missing something?

@manoopatil you are missing one decimal point. 2.4mnt when u multiply gives you Rs8640mn as answer which is Rs864cr.

10 Likes

@Rakesh_Arora Sir why KIOCL is valued at a higher multiple than GPIL despite having lower profitability and return ratios?

just check the promoter holding of KIOCL - 99%! It’s not a freely traded stock

2 Likes

Thank you sir…I was also thinking that this might be the reason

1 Like

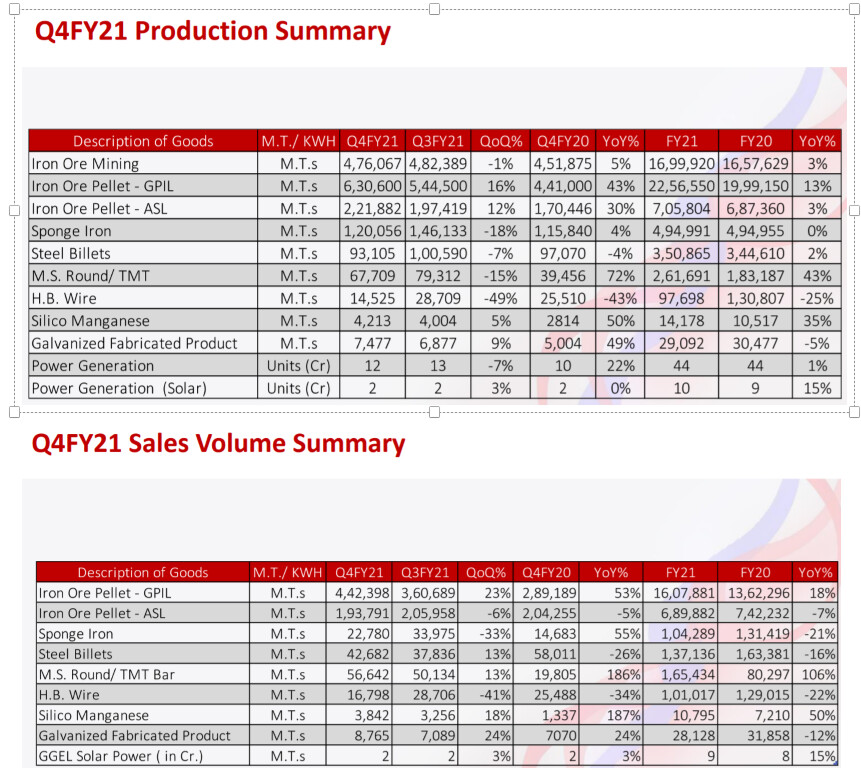

@Rakesh_Arora could you please throw some light on difference between production vs sales discrepancy for GPIL, it seems to be quite a wide gap for two consecutive years. Where is the extra production being utilized?

Also, any thoughts on why market is still valuing GPIL almost half of peer valuations despite a clear debt free roadmap, especially with newly listed SMEL?

4 Likes

@Piyush_Anand the difference in production and sale of iron ore pellets is due to captive consumption for steel making. Last year this self consumption was close to 0.6mnt and will gradually increase with increase in steel capacity to 0.9mnt.

Valuations - I think market assumes that GPIL profits are going to be more volatile as they are driven by iron ore prices whereas some of the other peers are just convertors and can have more stable margins. Eventually earnings will decide who trades where

10 Likes