Not sure if formulaic triggers for dividends and bonus shares will be value accretive. Bonus shares aren’t value accretive to the shareholder and dividends decrease value of the share if there are better uses if retained within the business. So, expect the book value growth to slow down if dividends are high. Am I mistaken?

GNFC is growing at a healthy pace with very good balance sheet. There is nothing wrong in giving higher dividends. Generally state PSUs are run by babus who are not interested in rewarding shareholders for obvious reasons. I think its a welcome step by Gujarat Govt to formulate a policy. This will give some predictability on at least dividends.

1 Like

Central PSUs have such guidelines since quite some years now. It leads to a consistent policy at least. While yes it is not always value accretive but when they are just hoarding cash and not rewarding shareholders you have to make a firm policy otherwise the cash will just be sitting there that too at not the best yields given their treasury management is also not very good.

1 Like

Your point makes sense.

Here is an article that articulates my concern.

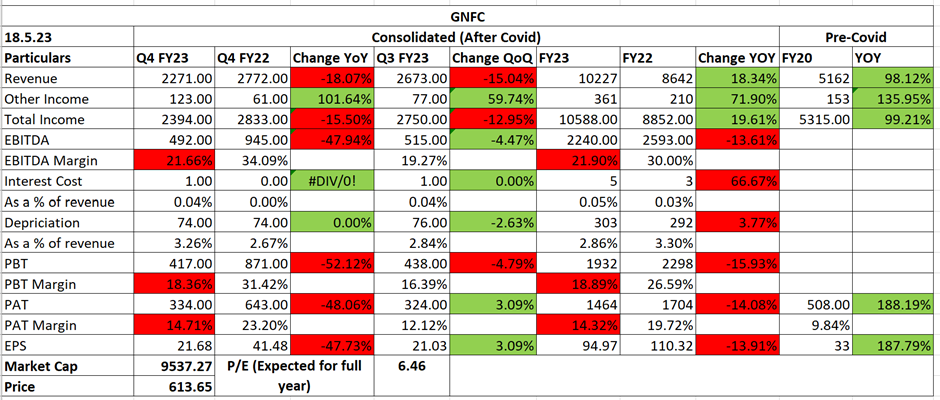

| - | During FY 22-23, GNFC has crossed over a billion USS worth of import substitution saving precious foreign exchange to the country and becoming active contributor to ‘Make in India’ initiative of Government of India. |

|---|---|

| - | During the year, new formic acid revamp project has been commissioned with 20 MTPD additional capacity. |

| - | Price levels of energy related inputs saw elevated price levels. |

| - | The Bharuch complex underwent annual shutdown from last week of March-23, which had some volume related impacts in Q-4 apart from wage revision accruals on Y-o-Y basis. In spite of these factors, the top line has improved to historical highest, whereas on absolute basis, the full year profit before tax is the second highest ever at 1,932 Crores in its history. |

| - | Revenue is driven by price realizations which are offset by offset by input costs. Input costs have been tapering off since Q4 so should see a reduction from Q1. |

| - | 100% capacity utilization in most plants. |

| - | Profitable operations supported by subsidy release support from GOI has helped improve the cash cycle. |

| - | Ammonium nitrate demand is growing around 6% per annum and is expected to remain consistent. Ammonium nitrate contributed 20% to the turnover of the chemical sector last year. |

| - | Buyback is not currently on the books but will consider at an appropriate time. |

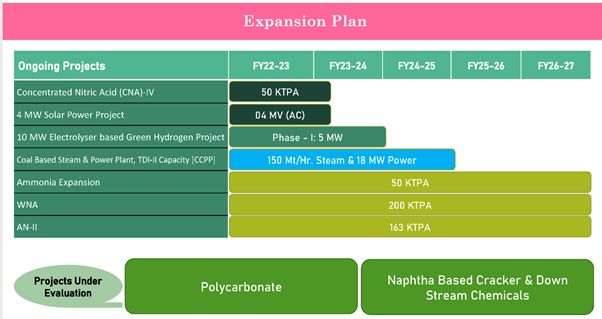

| Capex Plans: The company has committed around INR 600 plus crores of investment in the Formic acid revamp plan and coal-based power plant. The company plans to put INR 2,000 crores of capex within the next 3 years, with a potential increase in turnover of INR 1,000 crores if polycarbonate is considered. The green hydrogen project is under bidding and waiting for regulatory support before making a final investment decision. |

3 Likes

Would anyone in the group know the expected revenue of GNFC in FY26, assuming all the major CAPEX would be completed? Assume TDI prices remain the same. My understanding is that Fertilizers contribute very little towards profitability.

Any view on how Methanol for fuel is going to impact GNFC positively?

1 Like

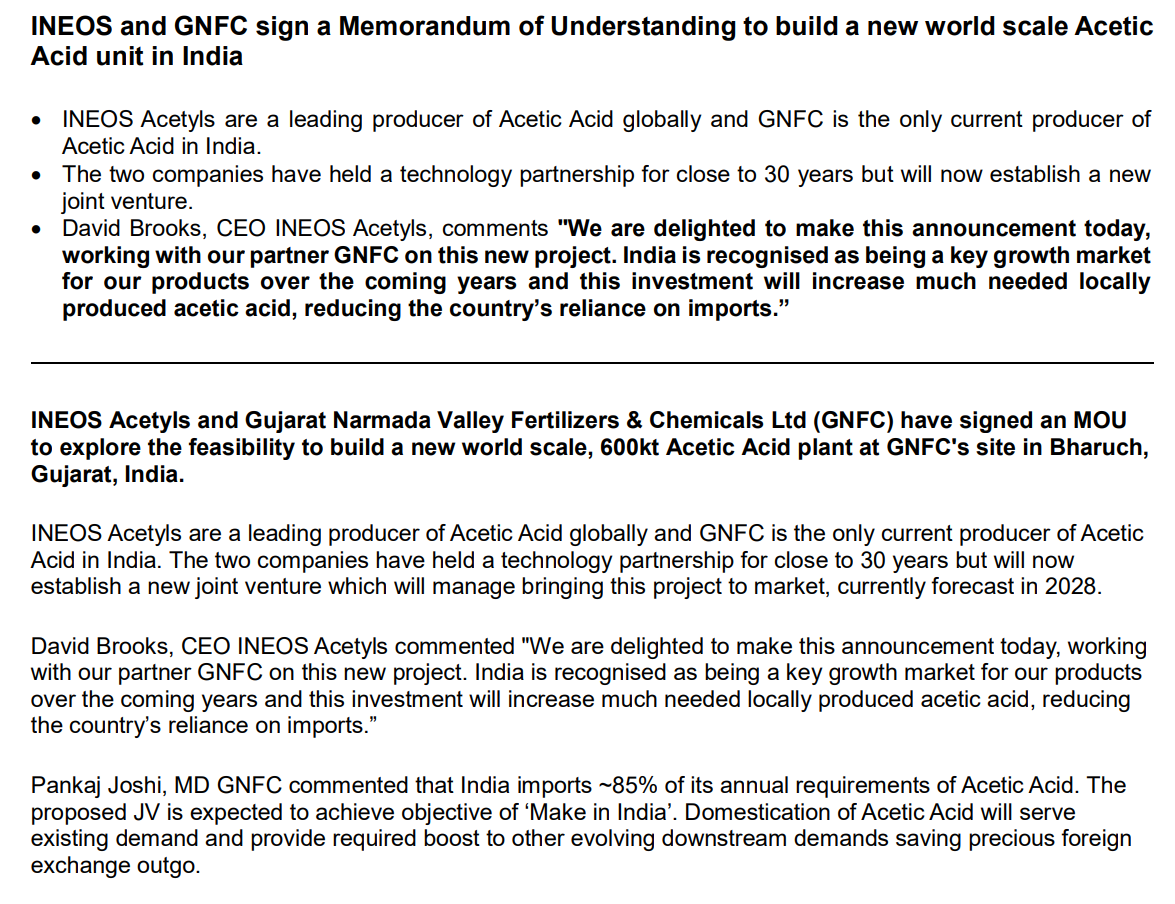

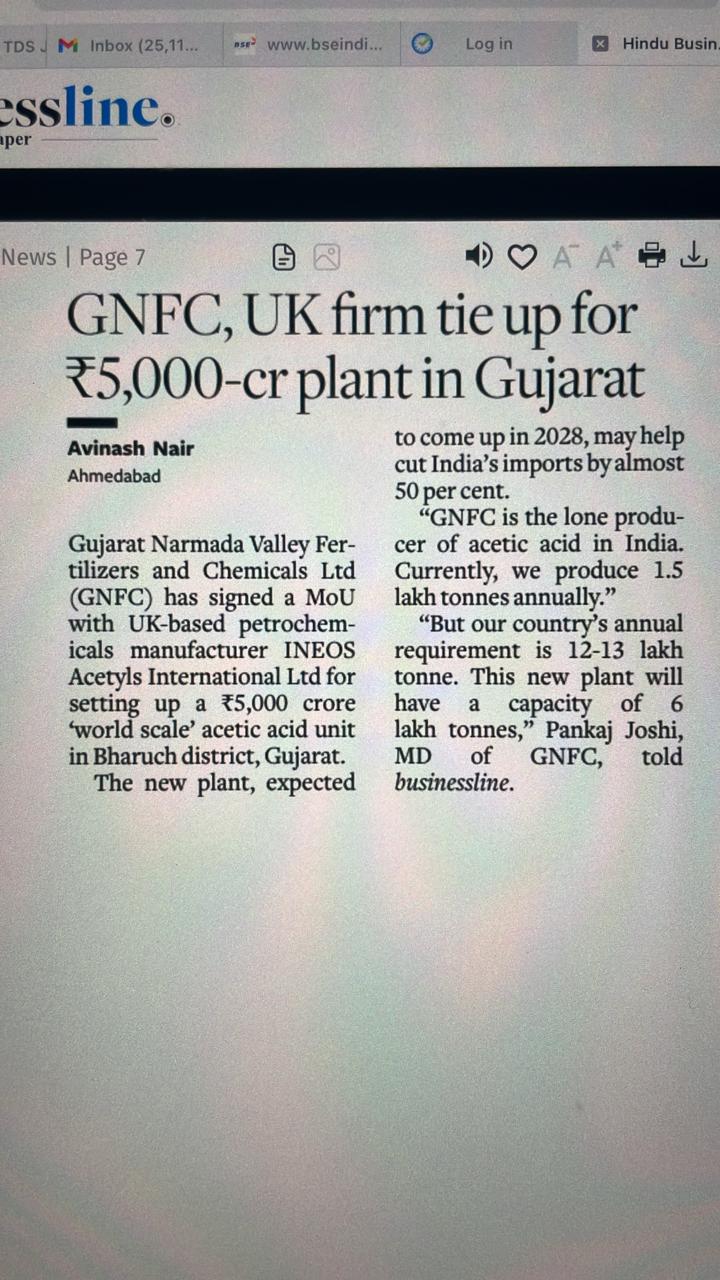

GNFC signs MoU with INEOS to form a JV and possibly build a 600kt acetic acid plant at Baruch by 2028.

4 Likes

GNFC - Got into my reading filter

Investing model(Now reading) - Value + Growth

Interesting trigger

Current P/E - 18 (21/11/2024)

Price (558) is less than book value (560)

Current dividend yield - 3%

Also

Massive capex of 5000 Crore

Few Concerns

#Only capex announced but outcome wait and see

Capex completion says 2028 (Too long)

But definitely should study

It is crucial to thoroughly review a company’s annual report, especially off-balance-sheet items, when considering long-term investments. Based on screener data, this company appears excellent from a valuation standpoint. Additionally, its capital expenditure (capex) trends indicate strong potential for future growth.

However, despite these positives, I am not interested in this company due to two major red flags:

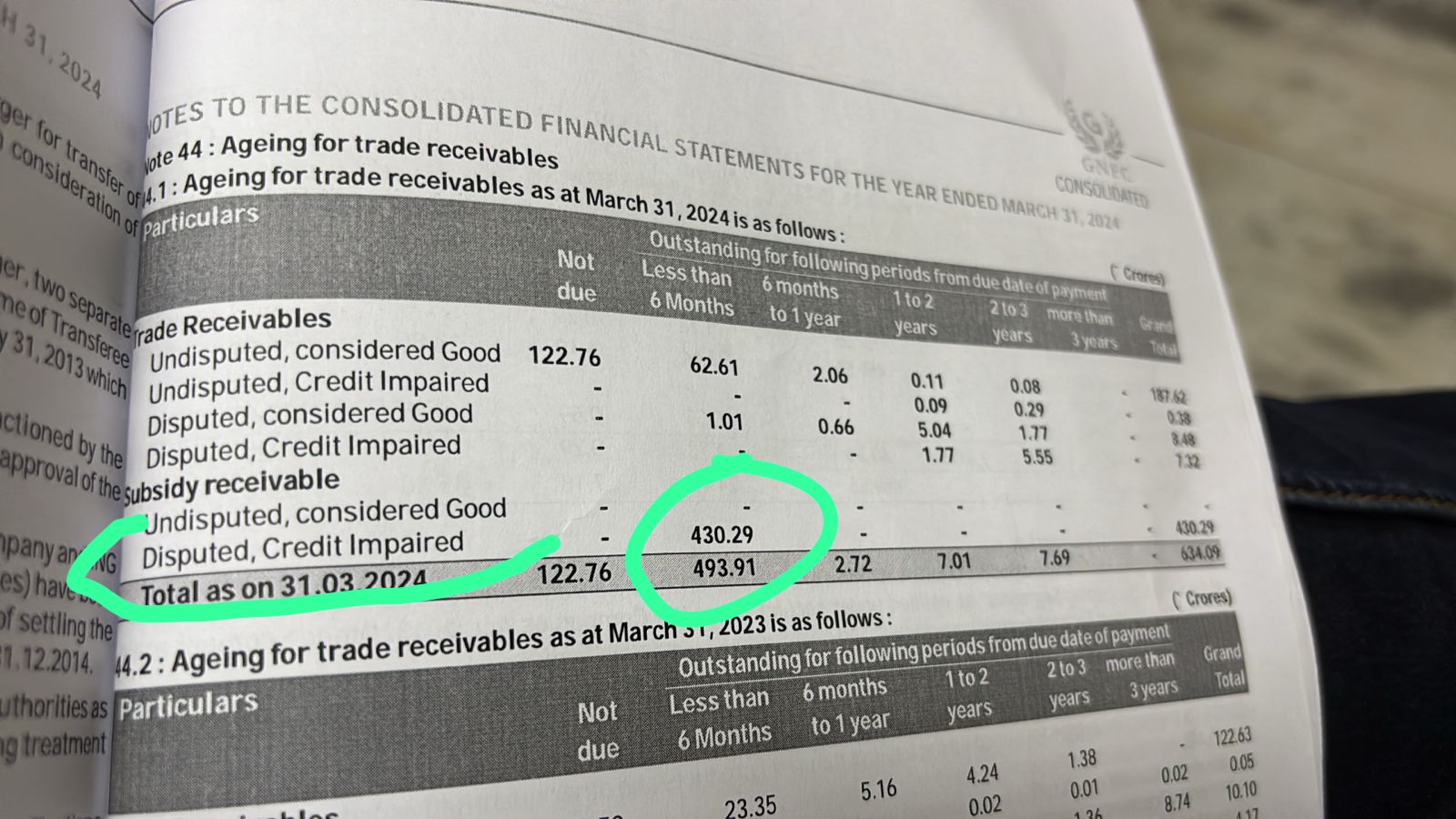

- The company has recognized ₹430 crores of subsidy as income, which is now under dispute.

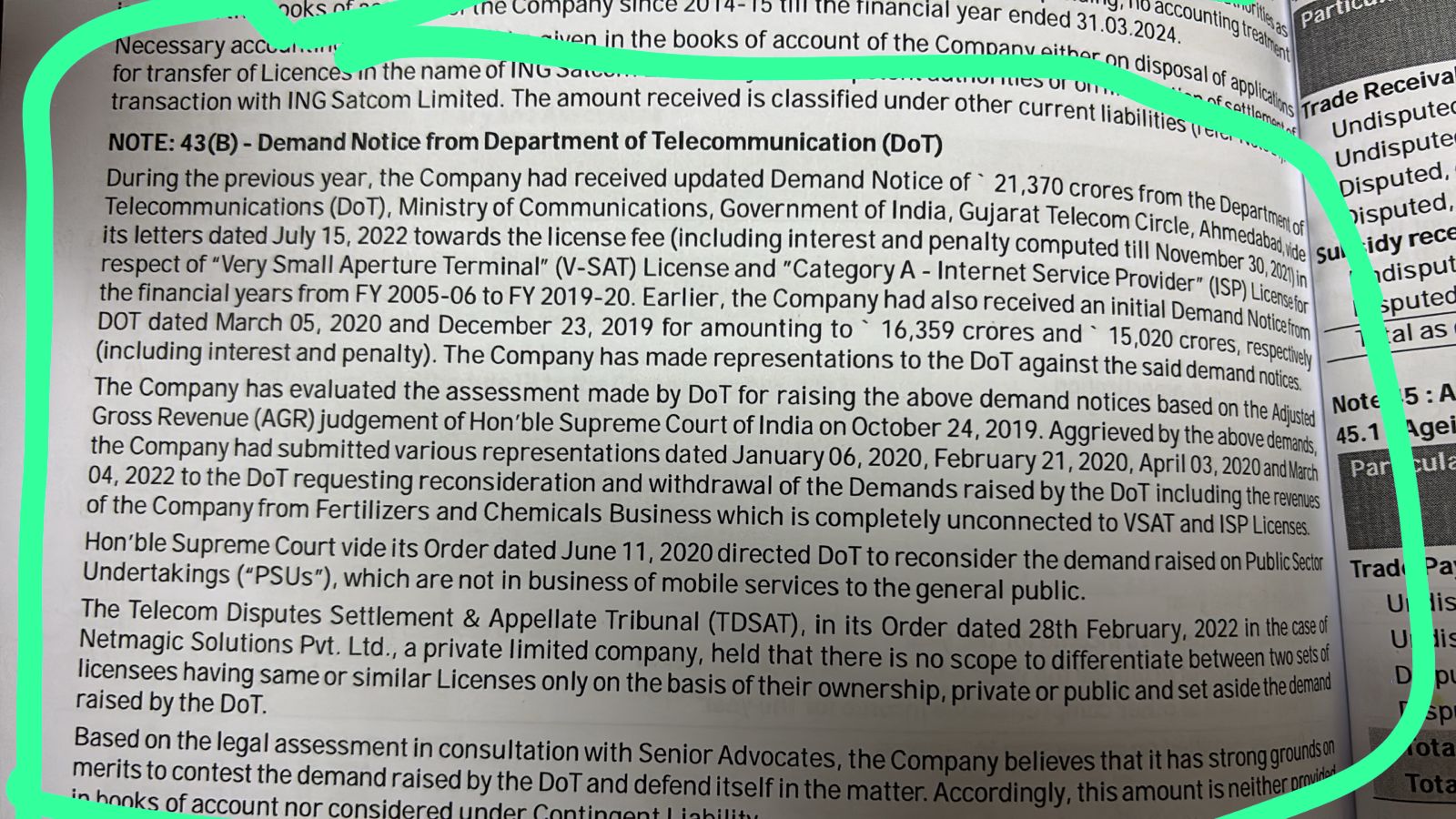

- The auditor has highlighted concerns regarding contingent liabilities. The company has received a demand of approximately ₹36,000 crores from a government department.

The company is nearly debt-free, boasting reserves of over ₹8,000 crore. Despite the sharp drop on December 27, 2019, when a notice caused the price to fall to ₹169.25, the stock has since multiplied significantly and never returned to that level. This week, it has risen by over 11.5%. Additionally, the company continues to reward shareholders with dividends exceeding ₹200 crore.

Don’t be swayed by news unless it is verified and reflects the true picture.

https://www.gnfc.in/wp-content/uploads/2021/04/GNFC_REG30_DemandNotice.pdf

Note: I’m not even invested in this stock—just sharing the facts. No recommendation.

demand may or may not sustain since my investment period is long term more than 5 years. so i am not interested. Additionally, the subsidy recognition issue has escalated into a dispute, raising further concerns.

Also it is a govt. company

I am deserved to be wrong

1 Like