GNFC

M.Cap: 1150 Cr CMP: 74

Introduction

I have started a brief discussion about the topic in my post “Profit Lies Where One Is Watching”.

Since then the company has show a remarkable turnaround. it has turned profitable. So I have started a new topic for this so that a more concentrated view about the company can emerge and we can discuss the prospects.

COMPANY

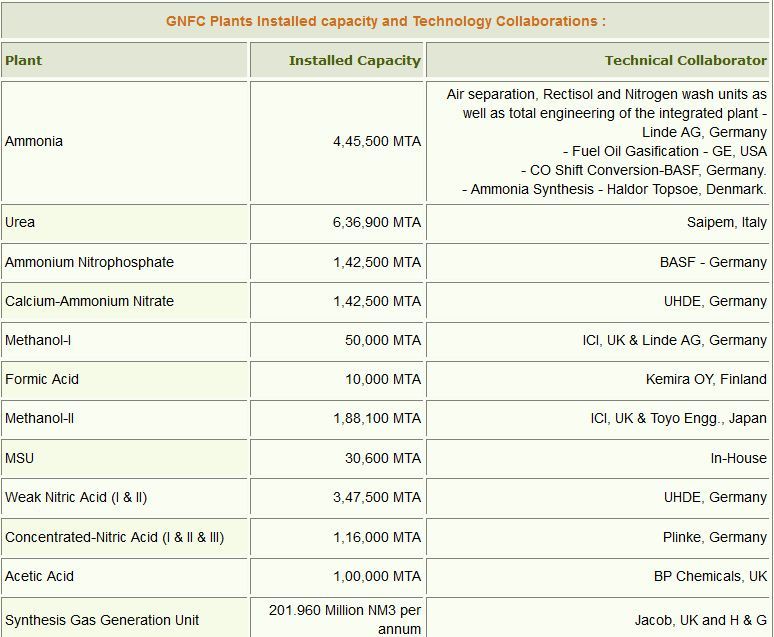

Gujarat Narmada Valley Fertilizer Company is a Government of Gujarat joint sector company with Gujarat State Fertilizer Corporation. It deals in fertilizers and chemicals.Plants are designed by reputed builders and Capacity data is given below:

GNFC lso ensures very high throughput.

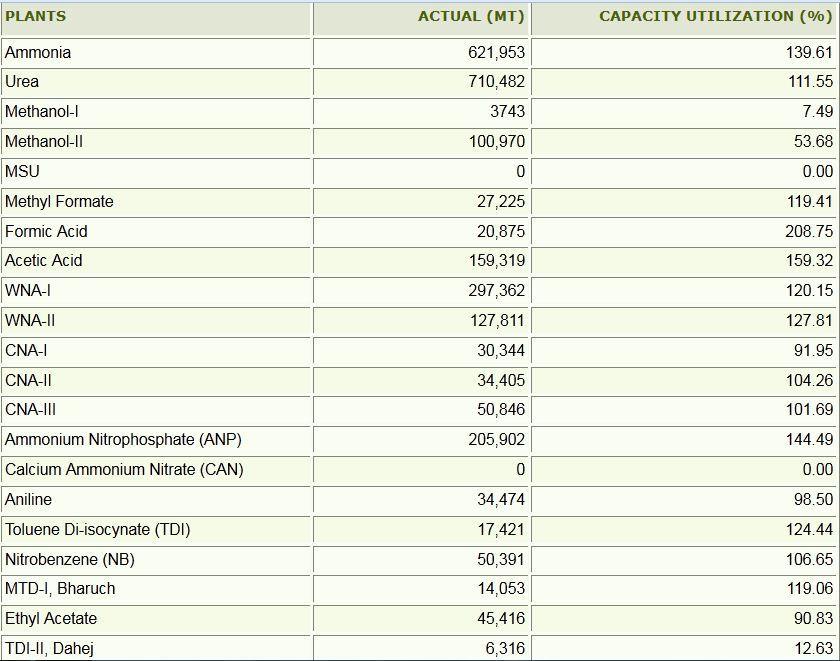

PRODUCTION FOR YEAR 2014-2015

Agile Management

Now as you can see its Methanol production is low because its not feasible to produce Metahnol in India because of unavailability of natural gas. So Management started import of methanol. DIsplaying management agility.

A Blast and Share goes to ashes

India imports 500000 tonnes of Toulene Di-Isocyanate (TDI) , a raw material to manufacture Foam and import is ever increasing due to high demand. GNFC is the only producer of TDI. It goes on to establish a new plant of 50000 tonnes at Dahej (mentioned as TDI-II in above report), increasing its capacity to 65000 tonnes from 15000 tonnes (mentioned as TDI-I in above report).

On The Fateful Night of January 9, a phosgene gas leak takes place at TDI-II plant leading to closure of the plant for a year due to Pollution Control Board notice leading to a loss of 789 cr, including 330 cr writeoff.

Glommy Days are Behind

In the previous two quarters, its has turnaround to profits as chemical business start outperforming. Also losses at TDI plant is reduced and will turnaround as soon as startup phase is over.

Also interest cost is reducing as it has started paying off debt. Also it also include a insurance award of 34 cr pending since 2008. But still it is a good turnaround.

Acoording to management commentary the TDI plant will break even this quarter as it has started operating at more than 100% efficiency.

Dividend Yield

The company continuously pay a dividend of Rs 3.5 per share, except previous year due to losses. At current price, it translate into 5% yield.

Growth Ahead

The Gujarat Narmada Valley Fertilizers Company Ltd (GNFC) will be implementing a Rs 4,463 crore expansion project in Bharuch district of Gujarat, where it will increase the existing production capacity almost three times for Urea, Ammonia and Aniline at the Narmadanagar plant. The Union Ministry of Environment and Forests and Climate Change accorded environmental clearance to the brownfield project where company plans to hike the existing production capacity of Urea from 7.2 lakh MTPA (million ton per annum) to 21.25 lakh MTPA, Ammonia production from 6.3 lakh MTPA to 16.52 lakh MTPA and Aniline production from 48,000 MTPA to 1.26 lakh MTPA.

As part of this expansion project, the company has also planned to set up a Water Soluble fertilizers (NPK) plant having a capacity of 5000 MTPA, and another plant for TDI-MDI blends of 7800 MTPA capacity. The water soluble fertilizer plant is being set up with an eye on the fast expanding drip irrigation network in Gujarat and other states.

Its quiet economical as Chambal Fertilizers is adding 1MTPA capacity at Rs 6700 cr.

Disclosure: i personally doesn’t have any stake in the company.