Revenue growth is subdued for this quarter. Let’s wait for the management explanation.

The results did not excite the market considering the sharp upmove the script had in recent past. However, it was their highest H1 PBT and PAT and higest Q2 PBT and PAT.

They are also very keen to change their revenue mix from Fertilisers to Chemicals which is very much evident in Q2 revenues as well. Chemicals are high margin business for them compared to fertilisers.

Going forward TDI, Acetic Acid and few more chemicals where GNFC enjoys leadership position should help to drive the revenue growth. Not sure how much that Neem FMCG business can contribute but they have very ambitions target of 500Cr revenue in next three from there.

We can have more details after the concall on Monday 13th Nov.

Regards,

Suhag

1 Like

Q2 results are dampener . In spite of good rains ( fertilizer offtake) and skyrocketing of TDI and acetic acid prices , it is disappointing to note the Q2 results are flat. Management commentary is not throwing light as to why results are flat… In their AR 2017, they informed TDI plants frequent disruptions is causing concern. Perhaps this may be the reason why they are not able to harness the Bullishness in TDI prices.Perhaps market has read the signals which reflected in the southward movement of stock.

Check the management commentary in many media forums. CMD was clear that GNFC cannot be assessed only based on TDI. There are many chemicals where GNFC is a leading player so TDI is only one part of the story. I agree to the point that management should indicate whether they passed on TDI price hike to customers or not. I think this question should be asked in the concall tomorrow.

For fertilisers, they are no longer targeting to increase revenues there. They are clearly focused on Chemicals and to some extent FMCG going ahead.

Regards,

Suhag

Did anyone get a chance to attend the concall? Please share the details if available.

Regards,

Suhag

03b36e63-eb26-4aa4-90d4-b96afe7c090a.pdf (227.3 KB)

GNFC Concall transcript.

Management is very optimistic and committed to debt reduction and have shown their focus towards Chemicals and reducing their focus on Urea and Fertilizers. Cash flow is going to be strong and Accounting profits dont show complete picture on improving margins, topline etc. Should do great from a next 2-3yr perspective.

2 Likes

Hello everyone. I would like to highlight some key points which I came across in the concall. Feel free to correct me wherever I am wrong :

-

The q2 numbers contain a provision made of Rs. 38 crore. This means the actual pat should be 165+26.6 =191.6 crores.

-

The TDI utilisation for the 50000 mt plant was at 75% in q2 and Average realisations were at Rs. 200000 (two lac) per ton.

-

The company has a pending order of 2500 mt which it aims to fulfill by Dec 31.

-

In q3 till date the company is operating at 90%+ utilisation levels for TDI and Average realisations are at Rs 300000 (three lac) per ton. The MD had given a figure of 200 mt per day.

A rough calculation will show that even if the plant was operational for 40 days it means 8000 mt was produced. Extra realisation of Rs One lac was there. It translates to 8000mt * 100000 = Rs. 800000000 EIGHTY CRORE excess in the profit before tax. -

All chemicals other than TDI are operating at 100%+ levels. Prices are also increasing steadily for many of them.

This is my first detailed post. Constructive feedbacks are welcome

4 Likes

Even there is a one time increase of 4cr for Employee expenses which I believe should add to PBT in next qtr. Further I too believe q3 will be a blockbuster qtr. Cash flows seem to be very positive too.

Q2 included a one time 10 cr donation for those impacted by a natural calamity.

Management is ultra conservative with no major expansion plans on the anvil other the DCP plant in March 19.

Hard to see topline growth in fy19. Bottomline should grow by interest cost savings.

Thanks for the details. I too went through the details of concall and agree to whatever you have posted here.

Few queries from my side.

1 - The interest outgo is very small. So now the debt-free by FY18 story is getting to its end.

2 - Company is shifting towards Chemicals and focusing less on fertilisers. Even though this is a good sign, with all chemical plants operating at 100% what will be the trigger for the stock to get higher price from here. Yes majority of their chemicals are trading higher currently but shall we buy just based on higher chemical price?

3 - As you mentioned, no major capex planned in near future. They mentioned some greenfield/brown field expansion but no details are available on that. Even the JV with the Belgium company will have very small impact on topline as their share is just 15% in that.

I am basically looking for triggers at current market price can justify the recent run up and can give comfort for future.

Please feel free to share views/questions/queries.

Disc: Not invested. Sold after Q2 results.

Regards,

Suhag

Is there any site / source where we can track TDI prices preferably TDI prices in INR

1 Like

This looks extremely extremely cheap to me. Because of the peculiar structure of the industry and the business model, it is much more important to look at the cash flows than the accounting profits. The operating cash flow for FY17 was around Rs.1500 Crores. Considering the buoyant demand for most of its products, the operating cash flow this year is expected to be more than Rs. 2000 Crores…As against this, the market cap currently is around Rs.6500 Crores. In a market full of so much froth, this look like a beautiful island of value to me. Market Cap/ Operating cash flow of 3x would be a treasure even in bearish market conditions. In the kind of markets that we are currently, this should have been trading substantially higher.

Business Risk Profile: This has been very well explained by the esteemed boarders in this thread. I was gong through the last three con calls and did some scuttlebutt and my sense is that Q3 will be the best ever quarter in the history of the company. In the industrial/ speciality chemical segment, around 70% of the chemicals that it manufactures is trading at highs or close to recent highs. The industrial/ speciality chemicals segment has been chugging along very well. In FY18, the industrial/speciality chemicals segment is expected to contribute to about 65% of the turnover and around 80% of the total profits. So, shouldn’t it be trading at the valuation of more like a speciality chemicals company rather than fertilizer company. It is worth highlighting here that it is actually trading cheaper than most of the fertilizer companies of similar size and pedigree. In the speciality chemical segment also, it manufactures many complex speciality chemicals and is not a 1 or 2 trick pony like many of the storied speciality chemical players trading at exorbitant valuations currently.

Financial Risk Profile: I expect the company to report PAT of around Rs. 500 Crores in FY18. However, as mentioned above, the CFO is expected to be around Rs.2000 Crores and that is where the treasure is. As the management mentioned during the last 2 con calls, the company likes to expense a lot of provision during the good times in line with the best practices. These are essentially non cash items and hence does not impact the cash flows. Hence, optically the PAT would not be as high expected. This sort of conservatism in reporting the numbers surely gives a lot of comfort. With same set of numbers and business conditions, I know many managements in India who would have reported PAT of Rs. 750 Crores in FY17. The dividend payout ratio is consistently increasing and was at 50% in FY17. This being a government owned entity, the dividend is expected to remain high. If you divide the P&L in two parts , the speciality chemical segment performance is as good as any other speciality chemical player currently. The speciality chemical segment top line is growing at 25%, bottom line at ~50% at a margin of around 25%. Now coming to the fertilizer segment, this is where I expect the results to improve substantially in H2 as the Gujarat elections will be done and dusted with. There is no reason why the company should report losses here, despite being one of the most well entrenched and efficient players. Also, from FY16 onwards, under the current dispensation, the subsidy payout timeline has substantially improved, thus reducing the working capital burden of fertilizer companies. The company has stated its intention of being a debt free company by H1 FY19. In fact the total dues and subsidies pending with the government is sufficient to wipe out its entire debt. So, the company should not have any problems in achieving this objective. FY19, in all probability should be a bumper year for the company as the upcoming budget is expected to have strong rural push due to it being a pre- election budget.

The management is very conservative in giving out targets. By observing them in various forums, I feel they want to take the debt off the books on a priority basis and want to be a debt free company.

Overall, I feel it is one of the most efficient players in its segment with a 60-70% share in TDI segment (whose prices are rocketing by the way) and is among the top 2-3 players in all the key speciality segment divisions that it has presence in. Along with the rapidly improving business profile and economics for the fertilizer players, this I feel is great story to play both the rural growth and speciality chemicals boom…and if such a company is available at Market cap/ Cash flow of 3x, it is literally a steal in my humble view.

The key risk here is the sustainability of speciality chemical prices, but that is true for every speciality chemical player in the market. In my view, this is slowly evolving into 2-3 years kind of story with the balance sheet improvement of most of these players. Just check what happened with Avanti feeds from 2012 to 2015. The market kept giving it subdued valuation till FY15 expecting the supply to bounce back in other competing countries, which has still not happened by the way. So, one fine day the valuation moves from 10x to 30x as the markets realized that the supply is not going to come back in a hurry and the growth is sustainable. So these cyclical trends can also evolve in to structural trends sometimes depending on how the demand side of the market behaves. Off course it goes without saying that the management team needs to execute to capitalize fully on the opportunity. Otherwise, all bets are off. I feel at the current valuation, GNFC is one of the very few mid sized companies currently available at such an attractive valuation, considering the wonderful demand scenario for its products and its perpetually increasing market share.

13 Likes

Thanks for a good details note. Just one query. Do you know about the speciality chemical te GNFC manufactures? Is there any differentiating product. I have heard about TDI which is used in foam mattress among others. I feel the market would look increasingly to more complex speciality manufacturer as the low hanging fruits of general commodity chemical boom (mostly due to China issues) gets over.

1 Like

Yup. that’s precisely what differentiates the company from others. Almost 70% of its speciality chemicals business are very complex chemicals. In fact, for TDI, it is the sole manufacturer in entire South Asia. So, it is literally a monopolistic business. In such a business and economic situation where TDI prices are skyrocketing, you can imagine the margins they will be earning in this. They are targeting a market share of 75% by end FY18 in TDI. With depreciating rupee, imports will become increasingly expensive for TDI. With the secular increase in foam usage due to lifestyle changes, the demand for TDI is expected to grow at a healthy rate. But it would be wrong to focus only on TDI. Most of the chemicals that they manufacture are at lifetime highs. The names of all the industrial chemicals is given in the opening post. I am pretty confident that Q3 will the best ever quarter in the history of the company and it will be a sight to behold. The speciality chemicals business is a treasure in itself, but I would also urge you to closely look at their fertilizer business. Due to the policy changes done by the government, the fertiliser industry dynamics are much more sustainable now. The most substantial impact of these policy changes is reflected in the operating cash flow of the company.

If I tell you that there is this debt free company with operating cash flow of around Rs.2000 Crores, with blended margins expected to be more than 25%, ROE more than 18%, operating in two exciting sectors (more than 30% market share in key revenue driving chemicals) with bright prospects for the next 2-3 years at least, how much will you be willing to pay?

I will be willing to pay at least Rs.15000 Crores for such a company. It will be exciting to see whether the valuation rerating will be immediate or will be gradual over the next 6 months. Let Mr. Market decide. I am sure one fine day , the analyst community will shift its focus from PAT to cash flow for this company.

P.S: Their neem coated product for which they have a target of Rs. 500 Crores by FY20 can turn out to be the joker in the pack if they execute well. This segment will command a FMCG kind of valuation and will have attractive earnings. Keep an eye out for that one. It will only sweeten the story.

2 Likes

Thanks for the response @maverickroger. It is a pretty interesting pick in speciality chemical. I guess market is tracking a breather after giving the company a good price upgrade in recent months There isnt much to do with this co apart from waiting.

1 Like

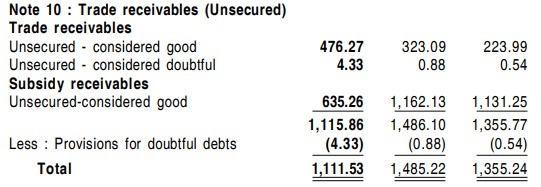

For FY16-17

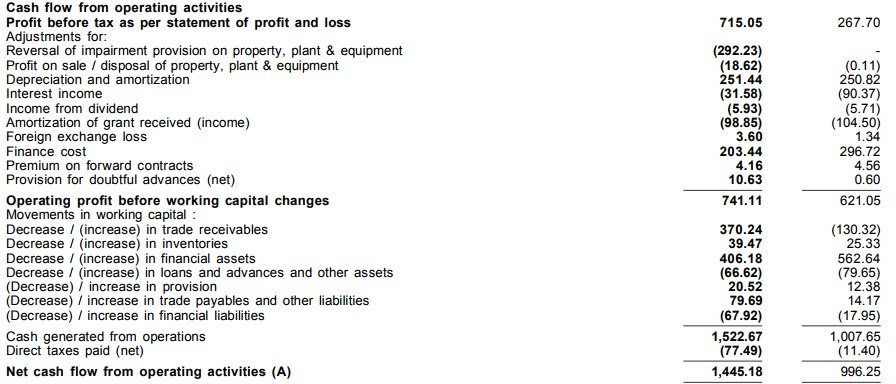

If we remove capital subsidy (other income ~ 225 cr) and one time exceptional item of 292 cr, this isn’t trading cheap at all. Cash flows have become better in 2017 due to couple of reasons -

- Receivables have come down by ~500 cr (predominantly due to timely payment of subsidies from the government) which is very good, and lower tax outgo due to MAT credit (actual tax paid in CFO is just 77 cr whereas in P&L it is close to 193 cr). Going debt free won’t have any impact on CFO, though it would definitely result in more free cash flows and PAT, as interest component will reduce (though they will still take large working capital loans in my opinion). Depreciation will be more or less same going forward.

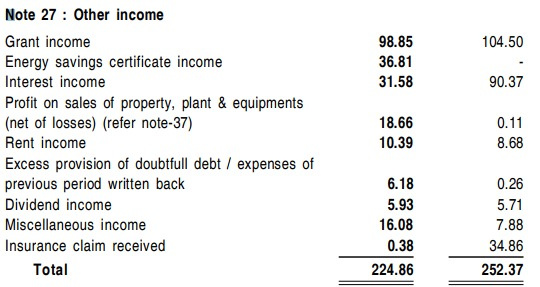

When we look at other income closely, i am not exactly sure what is one time and what is permanent (if you can help me here).

As per q2 concall, they are probably going to book contingent gains ~ 240 cr for energy consumption sometime in the future (as it is approved the government). Further, till Oct 2018, they will receive 287 cr in capital subsidy distributed equally in next 4 qtrs. So, in next 1 year, they will receive close to 530 cr other income, which is sufficient to wipe out quite a bit of debt. Then, they are making provisions, which is not effecting CFO. They said this will continue for next few qtrs at least. So what i mean with all this is -

-

Chemical prices are at its peak/near peak probably.

-

Once they receive these subsidies, other income will come down drastically. Just look at their other income till 2015 (was less than 50-60 cr). In 2016, it was close to 270 cr, and in 2017, close to 520 cr. This is predominantly due to subsidies and impairment reversal. If you remove this other income from 2017, PBT comes down to 200 cr (instead of 715 cr). p/e happens to be 34 in that case instead of 13. Though, how CFO will be effected needs to be evaluated. There will be one more year of high other income i.e. 2017-18.

In the below image, extraordinary gains are removed from PBT, as well as government subsidy is amortized. This means, there will be no impact to operational cash flows.

-

Fertilizer situation is improving due to timely release of subsidy payments. Though, with DBT implementation, urea consumption will go down. ANP (complex fertilizer) is under cost pressure as per mgmt in Q2 concall. This being a highly regulated sector, i am not too hopeful of increase in profitability here, though cash flows might improve due to further reduction in receivables.

-

Capacity utilization except for TDI is at its peak. No major capex on the horizon in next 2-3 years. DAP plant is going to contribute nothing significant. They said they might go for some capex to increase TDI capacity as per demand, though nothing on horizon as of yet. Moreover, they said they might go for debottlenecking projects which may increase capacity by 15-20%. Didn’t specify for which chemical.

So, my question is - Isn’t this already at very high valuation already? If you leave abnormal q3 which is on the cards due to very high TDI prices and skyrocketing chemical prices, things are not going to improve drastically post q3 apart from this becoming debt free (which market already knows), and subsidies they are going to receive. DBT is a wild card, and how successful it becomes, and how does it really impact fertilizer companies is yet to be seen. SO is their Neem venture.

Also, predicting cash flows here might be very difficult, if we take a cue from the past.

7 Likes

I had similar thoughts after going through the Q2 Concall which i posted in one of my posts. No major capex on cards. One question which is puzzling me is why they are so much after becoming a debt free company than doing some capex to add capicity when their realization is at peak for all of their chemicals. In fact, if we observe clearly, interest outgo is not that great so this craze of becoming a debt free company is completely misplaced IMHO.

For TDI, as per their own admission they can operate at max 90% capacity due to the complex nature of the chemical.

Their share is only 15% in JV with the Bulgarian company so i am not sure how much that will contribute to their top-line. If you have more details on that please share.

They are very ambitious about their neem products and have a target of around 500cr revenue by FY20. They are aggressively opening small stores and tying up with retail chains for their neem products. However, in such competitive industry, how much margin that will fetch is to be seen. As of now company has not shared any road-map on that.

Regards,

Suhag

There are 2 things here which will aid margins. Actually they are paying 2500 inr per tonne to lift HCL from their premises. For 200000 ton, this means 50 cr. This cost will be saved starting Jan 2019. ALso, they might be making some bucks out of it, though not much. SO, this will add to bottomline. (i missed this in my earlier post). So this is more about saving than earning. But penny saved is a penny earned!

Neem project is more of a forward integration for urea. They are also looking at is as a socioeconomic project, which is good. Right now they are not incurring losses, though not making much profits either. Management pointed that the target of 500 cr is pretty ambitious and they won’t be able to attain it within this year (i think they meant 2017-18?, or 2018-19). I am not very hopeful on this front to be honest. If it works, it is good, though they are also planning to open 1000 stores in Gujarat. I am not sure if entering in retail on their own is such a good strategy. May be they can have these products in their existing fertilizer stores, though i do not know the dynamics here.

Going debt free is not bad imho! It is a conscious decision as memories of 450 cr losses due to trouble at TDI plant has haunted them. Going debt free will result in lots of free cash which can result in increased dividend yield. ALso, i like their decision to do any expansion from now on through internal accruals. That is actually best for us shareholders. Interest outgo isn’t much and debt equity is already comfortable, but i like this as this makes me more comfortable. Being conservative is a good thing. They might be able to do well even if they maintain some debt, so in any case your point is fair. In fact in the last concall, a guy from Reliance MF asked about his particular thing. Mgmt just replied what i mentioned above.

Regarding new capex -

Well, their first priority is going debt free, so all free cash they are generating is going towards debt repayment. This will improve PAT going forward, which is good. They will think about expansion once they are debt free. May be there are some plans but they don’t want to divulge that at the moment. First things first! They can still improve their numbers by improving TDI plant utilization. They said they are going at 90% at the moment. Though, this plant being technologically challenging, i am not sure if they can milk it like they have been doing with many other chemical plants (over 100% utilization).

One more thing (about their IT business), which posted 51 cr PAT last year. This is a high return business, and they are doing very well on this front. Lots of opportunities galore in this realm.

Fertilizers, i am not too hopeful on realizations, though, it will improve their cash flows quite a bit due to DBT model. But no impact on profitability (PAT).

All in all, this is a decent company with some moat. Though, realization are at cyclical peaks already, and with crude and gas prices rising, margins may come down. So, despite increasing cash flows, market may not take margins and realization reduction lightly.

2 Likes

They are not entering in retail on their own. Check recent interviews of CMD. He has mentioned that they have their products listed on Bigbazaar, Star bazzar and other retail stores. Login to twitter and just search GNFC, you will see they are opening small stores almost daily on different locations.

CMD clearly mentioned many times that TDI cannot be operated at 100% Capacity. Due to its complex nature, the plan needs to be shutdown periodically for maintenance and hence going even till 100% is almost impossible. Also, they do not want to take any chances due to the incident in past at their TDI plant.

I never concentrated on their IT business even though i did my final year project there ![]() Thanks for pointing this out. Shall check on this going forward.

Thanks for pointing this out. Shall check on this going forward.

Regards,

Suhag

2 Likes

Please check recent concall. They said they have plans to have 1000 stores in Gujarat for this project.

Yes, that is what i said. TDI project being technologically challenging cannot be operated at full capacity. Max they can attain is 90-95%.

Regarding GNVFC (their IT wing), i as well did my internship there way back in 2004. ![]()

1 Like