GMMPFAUDLER chart and key-numbers:

What could be the reason for market not appreciating GMM’s performance wrt stock price. Inspite of Good results, earnings growth visibility, market leader in its segment, underperformance to HLE the stock price is not moving. Is there a concern on corporate governance due to the last OFS which happened which can explain this ?

IMHO, the bull case around GMM hinges around their successful integration of the acquisitions they’ve made and deliver promised revenue and ebitda numbers. With a global acquisition, especially in high labour cost countries like Germany, etc., integration and labor cost savings are not a given; they really need to execute well. If market sees good execution and consequently much higher EPS because the # of shares haven’t increased but revenue/profit should increase substantially, the stock should re-rate.

Disc: Invested

5 Likes

GMM Pfaudler appoints Kotak Mahindra Bank Chairman as an independent director

GMM Pfaudler announces 1:2 bonus shares

1 Like

A session worth watching @ Webinar with MD of GMM Pfaudler, on ‘How has GMM successfully used Acquisitions to create value’

Mr. Tarak Patel looks super confident as always… stock is technically trying for a breakout too…

2 Likes

Read in Bloomberg Quint that Indian promoter[Patel Family] bought 1%.

3 Likes

Is reduction in Promoters share from 56.06% to 38.74% a sign to worry?

Hi Arpit,

That’s PE investor who is liquidating his shares. That’s y Promotor shares came down.

prashant

1 Like

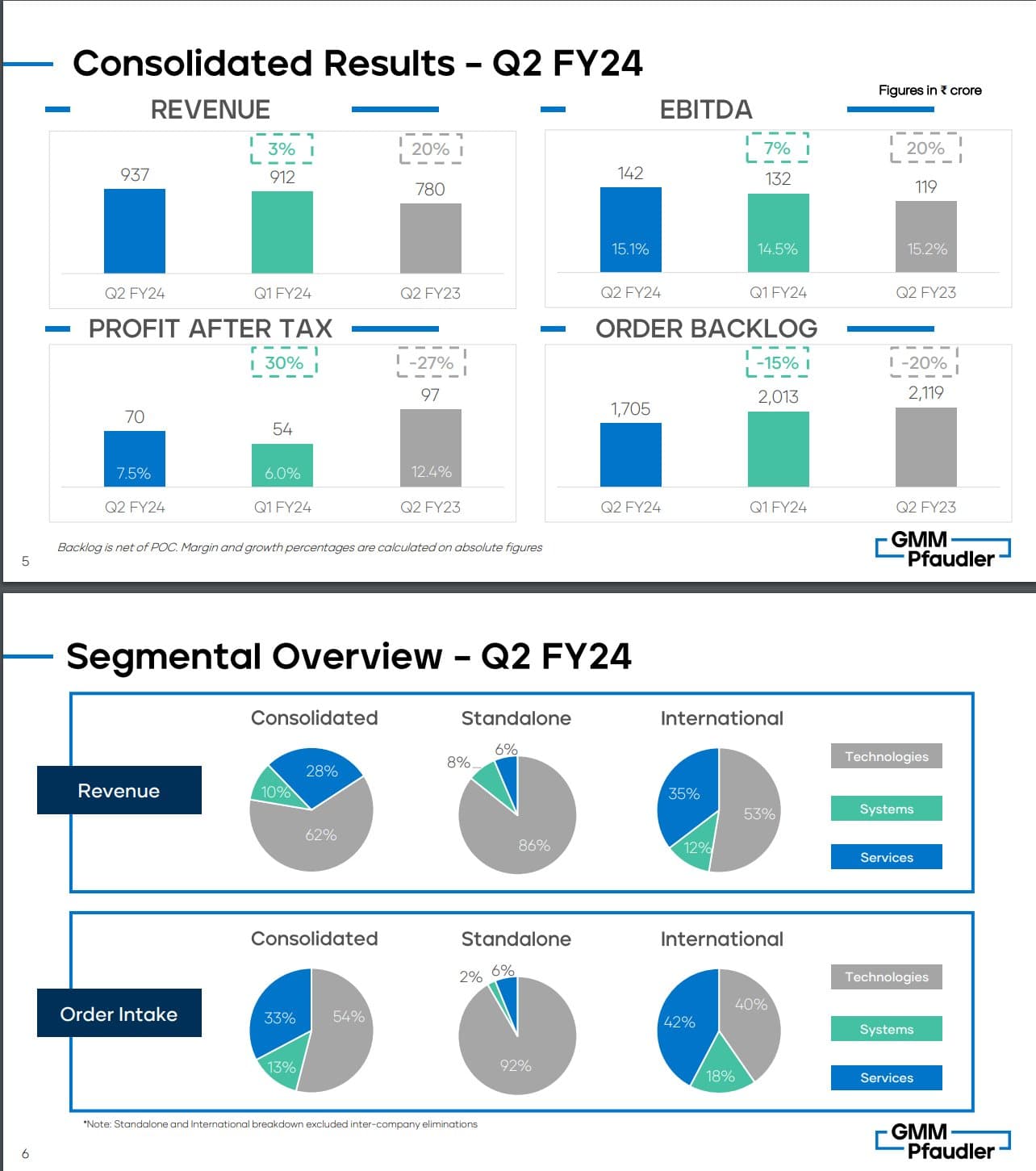

Q1Fy24 - Rev - 912 CR PBT - 86CR EPS - 12.22

- 23.41% Revenue growth YoY. OM margins seem to have improved marginally to 14% yoy.

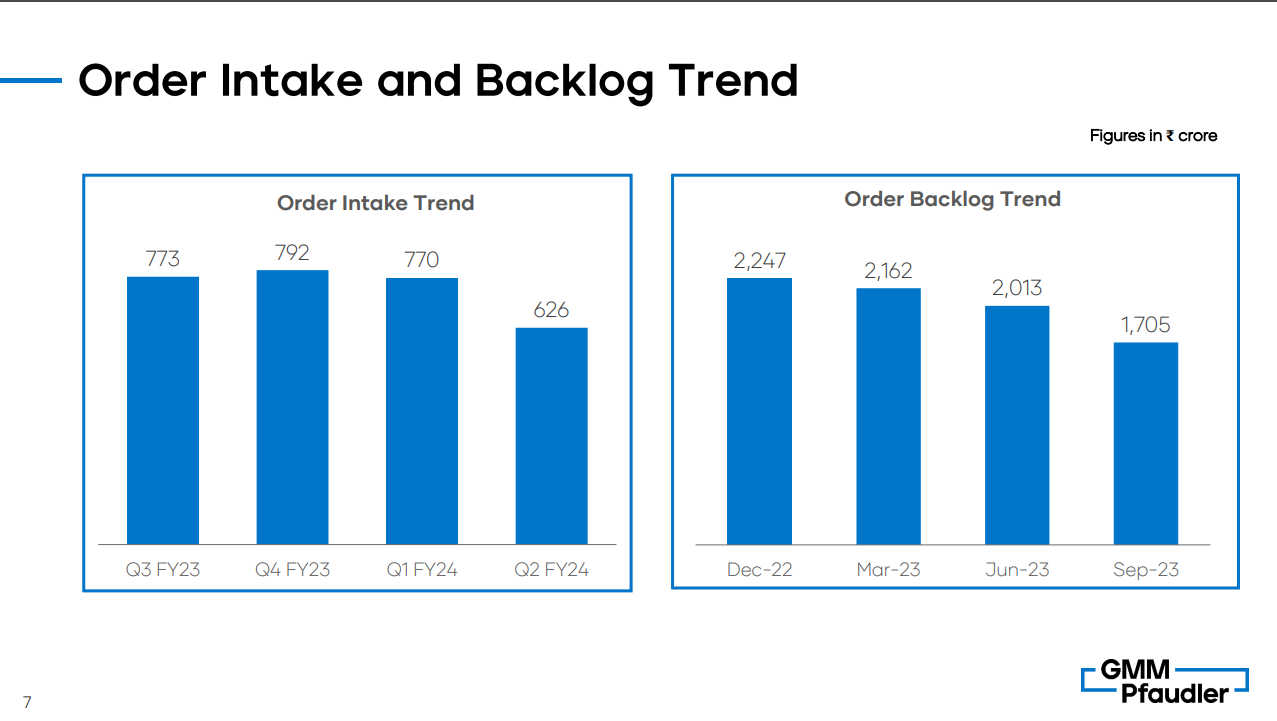

- There is slowdown in chemical industry and this is impacting the order book but are hoping that order book will pick up in Q2. Systems business is underperforming.

- Order back log is currently 9 months

- EBIDTA is 35% higher YoY however other income and PAT is lower, if PAT is lower how is EPS higher? - values have been rebased, so in JuneFy23 the actual profit was higher but amount to group was smaller, this is worrying though as it means profit has regrown YoY but this is primarily due to higher tax, PBT is more or less level.

- On track for EBIDTA guidance and will surpass Revenue growth.

- Confident of Similar levels of growth going forwards - Consolidated 13-15% Revenue growth and EBIDTA growth 18-20%.

- India business to growth 17-18% Rev and 20% EBIDTA.

- Future CAPEX they are saying 3-5% including maintenance for future growth targets.

- He is committed to increase stake by 1% at 1700Rs/share. Shows management commitment to this.

- Currently there is overhang in share price due to anticipated stake sale by institutional investor hopefully this should clear soon.

- They feel they are growing market share vs the likes of Glasscoat

- Debt 800CR - net debt 500CR - in 2 years they should be able to clear the debt completely with 800cr of free cash flow vs generating roughly 1600cr of EBIDTA. Any reduction in debt could provide a 10-15% pump up to PAT.

- Focusing on service centres - will try to make 15-20% of total revenues in india and china.

- Tax should be 26% yearly this Q is higher.

- Other expenses - repairs, consumables, legal professional etc

- North America acquisition for mixing company is in final stages

—————————————————————————————————

| FY23 | Q1FY24 | FY24E | FY25E | FY26E | |

|---|---|---|---|---|---|

| REV | 3178 | 912 | 3500 | 4000 | 4500 |

| EBIDTA | 431 | 132 | 550 | 630 | 750 |

| EPS | 37.06 | 12.22 | 52 | 65 | 72 |

4 Likes

I doubt that, Chemical companies are suffering due to destocking in Major Markets.

Some of them already did Capex or in middle of it. They are incurring increased interest cost as well.

New orders will take quite some time for GMM and GLE.

My Observations could be wrong, Pharma Revival Could be a side kick.

Bottom line is in Covid + 1.5 Years Lot of Capex happened hence Orders were booming.

Pfaudler sold 13.5% shares yesterday… balance 1% is supposed to be bought by promoter Patel at 1700 once FDI france approval. Likely to happen by sept as said in concall.

4 Likes

3 Likes

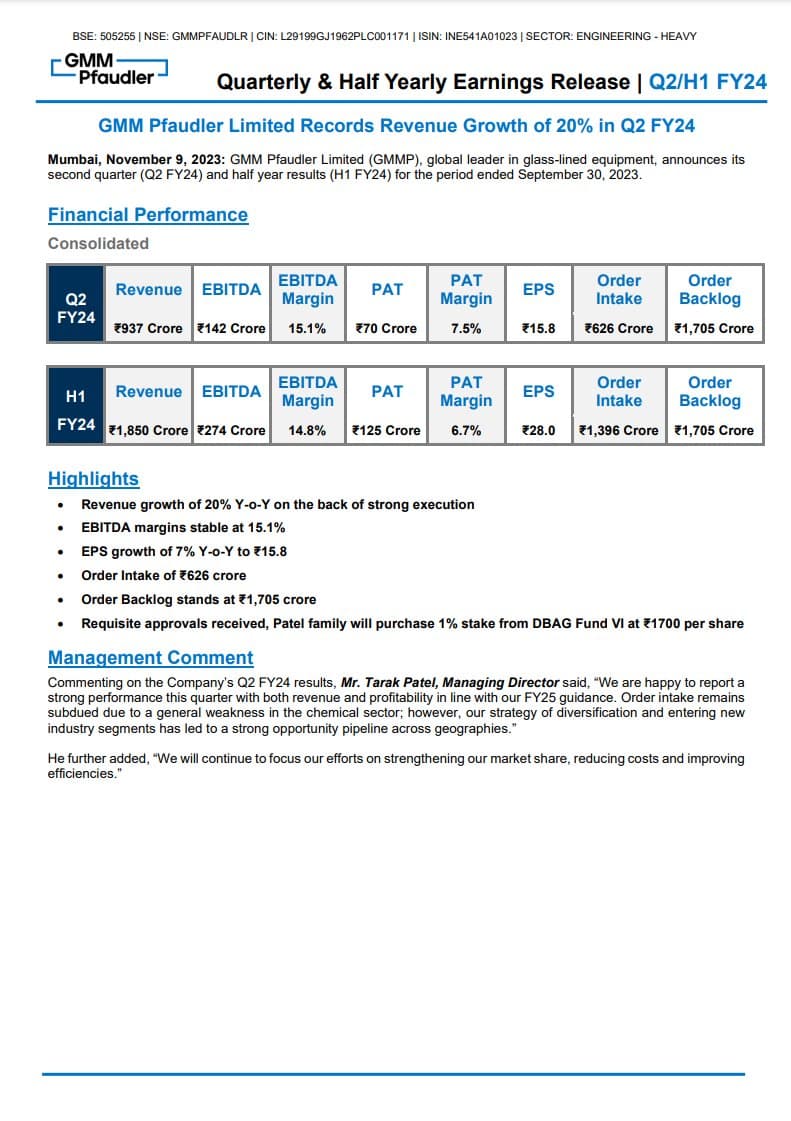

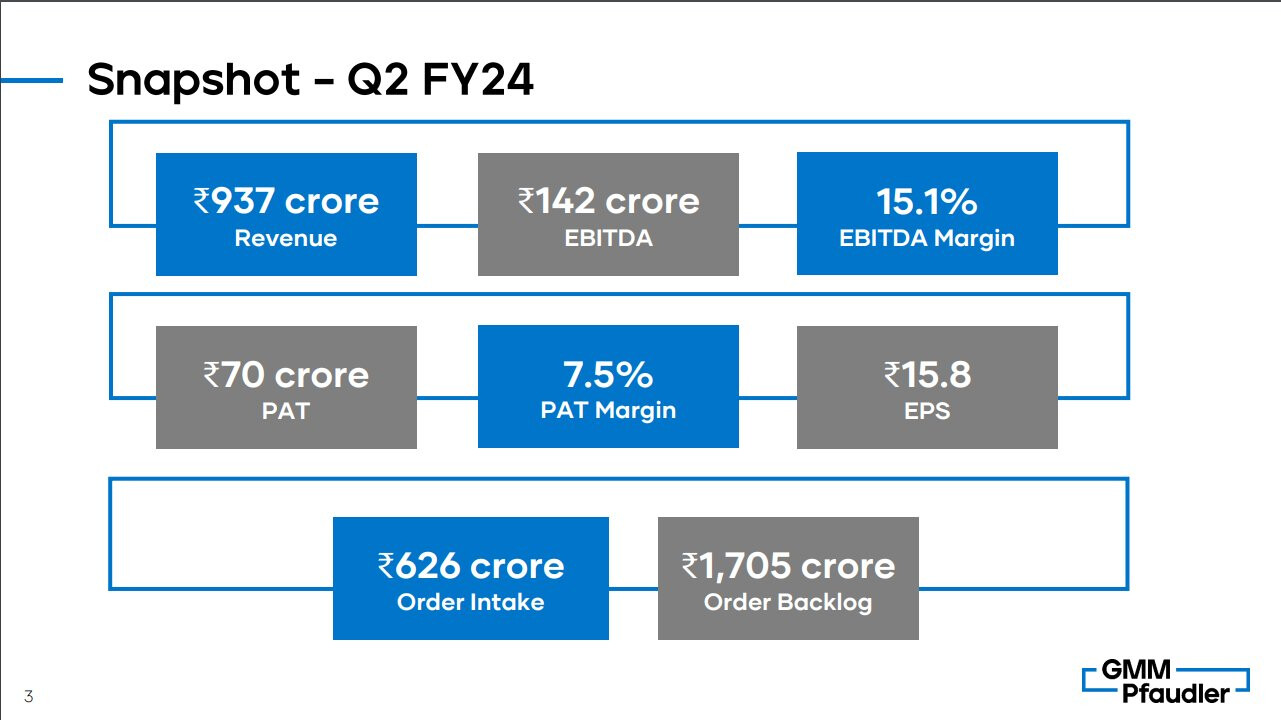

GMM Pfaudler Limited Powers Up Q2 FY24 with 20% Revenue Growth!

Consolidated Q2 FY24 Highlights:

- Revenue: ₹937 Crore, boasting a robust 20% YoY growth.

- EBITDA: ₹142 Crore with a stable EBITDA Margin at 15.1%.

- Profit After Tax (PAT): ₹70 Crore with a PAT Margin of 7.5%.

- Earnings Per Share (EPS): ₹15.8, marking a solid 7% YoY growth.

- Order Intake: ₹626 Crore, reflecting a strong demand.

- Order Backlog: Stands tall at ₹1,705 Crore, indicating a promising future pipeline.

H1 FY24 Performance:

- Revenue: ₹1,850 Crore, showcasing a substantial 20% YoY growth.

- EBITDA: ₹274 Crore with a consistent EBITDA Margin at 14.8%.

- PAT: ₹125 Crore, maintaining a PAT Margin of 6.7%.

- EPS: ₹28.0, exhibiting a steady 7% YoY growth.

- Order Intake: ₹1,396 Crore, demonstrating sustained demand.

- Order Backlog: Continues to stand strong at ₹1,705 Crore.

Strategic Achievements:

- Stable Margins: EBITDA Margins hold steady at 15.1%, showcasing operational efficiency.

- EPS Growth: Impressive 7% YoY growth in Earnings Per Share.

- Order Book: Healthy order intake of ₹626 Crore and a substantial backlog of ₹1,705 Crore.

Management Insight:

- Tarak Patel, MD: Reports a strong performance, aligning with FY25 guidance.

- Order Intake Strategy: Despite a chemical sector slowdown, diversification strategy leads to a robust opportunity pipeline.

- Future Focus: Continued efforts on market share, cost reduction, and operational efficiency enhancements.

Global Leadership:

- Industry Standing: GMM Pfaudler, a global leader in glass-lined equipment, maintains a strong position.

- Geographical Diversification: Strategy of entering new industry segments proves successful, contributing to global opportunity pipeline.

Strategic Move:

- Ownership Transition: Patel family to purchase a 1% stake from DBAG Fund VI at ₹1700 per share, indicating confidence in the company’s growth trajectory.

Management Quote:

- Tarak Patel: “We will continue to focus on strengthening market share, reducing costs, and improving efficiencies.”

2 Likes

All parameters good, however Order intake would be key monitorable thing going by next few quarters…

Last quarter exited at 1.7k level. would want to re enter if revenue visibility is more

4 Likes

Its sales have been growing at 20.9% CAGR over the last 10 years, which is a good sign for someone who has 50% market share. More recently, its profit growth of 40% CAGR over last 3 years has been impressive where as the stock has given -5% returns (since Nov 2020 till date). On paper, this does look like a very good investment candidate from a risk to reward perspective as the business seems to be doing well but the market is skeptical. I know this is a very simplistic way of looking at things but is something wrong with this view? Is order intake the only thing that the market is worried about?

1 Like