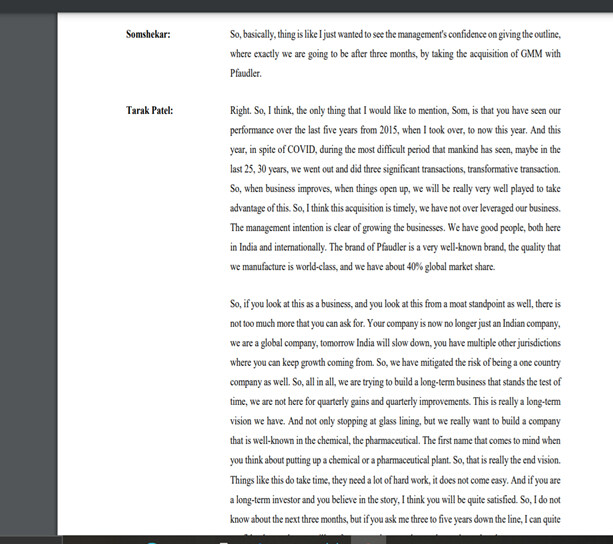

Management interviews

1 Like

1 Like

GMM Pfaudler commences manufacturing operations at its facility at Vatva, Ahmedabad.

Commenting on the occasion, Mr. Tarak Patel, Managing Director – GMM Pfaudler, said: “We are extremely happy to have commenced manufacturing operations within such a short period of time. Over the last few months we have seen signinficant improvement in order intake and the quick start-up of this facilty will go a long way in growing our Heavy Engineering business.”

3 Likes

As per the Concall after Q3FY21 Consolidation was to start from 01st of Feb this year and Q4 will get Feb and March this year. However the execution was completed on 17th Feb. So the Q4 would have all of march and some of Feb…

Finally, most awaited nos. arrives. While the result seems okayish, I am concerned about employees costs becoming 6X. Moreover, as per investors presentation rate of growth of pfaudler international is considerably slow than our local GMM.

Present valuations aren’t providing any comforts.

At annual EPS of 50 Rs. stock is trading at 100+ PE.

Could you explain over 6X employee cost, was present in the concall maybe I missed that part.

The plan is to bring synergies & change the way international business would be conducted going forward so the state of international business doesn’t matter as long as the company is able to deliver what they promise.

100+ is trailing or forward looking?

They have presented insight into the international business numbers & I see it being profitable & descent enough to bring the FY22 PE much lower to what it is now.

Also the employee cost for international business is high & they promised to bring them down.

I hoping another concall with better future visibility very soon since they somewhat escaped couple such questions & promised to do them later

Their team in Europe is relatively very expensive and that is driving the 6X employee cost.

Are you sure, it wasn’t a one time employee benefit?

one of the analyst had asked this question - Management said it is combination of both - but largely it is their international resources are very expensive - to rationalize this, they have 2 options - rationalize the resources - number of resources, their cost, etc or keep the same headcount and expand the business. They said they will go for the later - this approach had worked during their MAVAG take over.

1 Like

Thanks Tbhavesh for adding this information. Major takeaway for me was that India business has been quite strong. Whereas, the International business is a drag, given the expensive valuations the stock is currently trading at. I think smart money may move to HLE Glasscoat, and keep it more expensive than GMM in near-term.

Or wait for the management to bring the same level of efficiency in medium to long term . Depends on one’s faith over management.

Everything boils down to the management. In their concall, the regime has pointed out an expected revenue of 2,800cr by 2023-24. Supplementing the income that HDO will generate (a company who used to do a turnover of 1,000 odd crores a few years back); therefore if the company can even succeed to generate a revenue of 400cr, which seems reasonable–due to the heavy order queries for heavy engineering, GMM can generate a revenue of 3100cr.

This, of course, hinges upon the chemical, pharma, & agrochemical boom that our country is going through; provided there’s a more significant jump in the sectors mentioned earlier, GMM will generate even more revenues due to the heavy CAPEX these companies are encountering.

This year, due to the acquisitions and increased employee costs, the company couldn’t churn sufficient profits. This former has been pointed out in Point No.9 on the Consolidated P&L, under exceptional items.

GMM looks well-poised to progress at a reasonable rate, and the management’s bullish prospects strengthen my faith in them.

5 Likes

Q4 call based Future outlook Upside triggers for mgmt guidelines of FY24 2800 Cr revenue and 16% EBDITA -

-

GMM standalone performance to continue at similar rates of last few years i.e. Revenue 25-30% CAGR - i.e. FY 21 Revenue of 650 Cr to 1300-1500 Cr + 300-400 Cr of topline from recent acquisition in Vatva (mgmt agreed in concall that guidance will be revised to include this acquisition as it was post initial guidance) - for FY 24 we are looking at 1600 to 1900Cr number from standalone business from India + Mavag.

at current margin profile(EBDITA of 25%) this would translate into 240 to 280 Cr PAT in FY 24 -

International Biz - there were lot of Questions on future margin profile of acquired biz - two months of pflauder is run rate in this year (Feb & march) is Approx 120 Cr/mo revenue run rate - with a very low margin profile of single digit. If we go by Mavag acquisition history - the EBDITA margin profile currently stands at 15-16% - mgmt call out to participants of same tells that they would be looking at similar trajectory of margin improvement in coming years for acquired biz , and a modest revenue growth rate (they did 8% this year) of 10-12% range i.e. 1400 cr FY 21 revenue at 8-9% EBDITA - moving to FY24 at 1800 Cr at 14 -15% EBDITA - i.e. 150 to 200Cr PAT

-

FY 24 View summary - strictly back of envelope calculations

India + Mavag +Vatva - Revenue of 1600 to 1900 Cr , Ebdita 25%, PAT 240 to 280Cr

Pflauder/Int biz - Revenue of 1800-1900 Cr at , 14 -15% EBDITA - i.e. 150 to 200Cr PAT

Consol Potential is - Total 3400 Cr to 3800 Cr revenue, 18% EBDITA and 390 Cr to 480Cr PAT

Management Guidance as of now is 2800 Cr Revenue at 16% EBDITA ( vatva to be added)

Current market cap is 7000 cr, Business has technology Moat and thus entry barriers, has tailwinds of sector (Pharma/chem/Heavy engg…), very long growth runway with quality management …

One of participant asked question about next quarter guidance - for which Tarak gave a long answer - IMO this tells a lot about management thinking, vision and aspirations

Invested

13 Likes

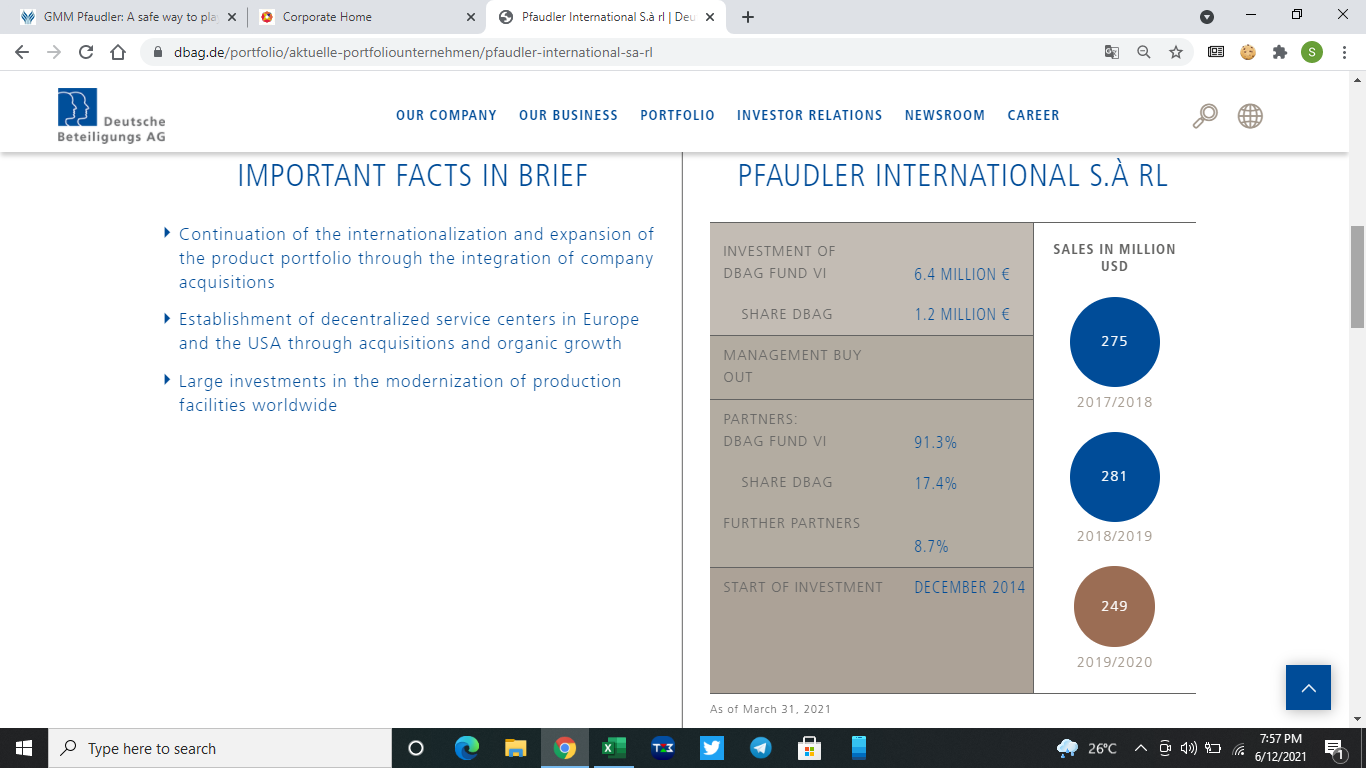

A question to everyone tracking GMM. Did you know that the Pfaudler Inc has almost not grown or even de grown revenues since 2018?

Pfaudler International S.A RL as per my knowledge is the holdco of Pfaudler group and that as per DBAG website has a poor record. The recent number available in GMM Presentation.

As per [DBAG exepctation in 2014] when they acquired Pfaudler, they had a guidance of 180Mn USD sales in 2014.(https://www.handelsblatt.com/unternehmen/industrie/deutsche-beteiligungs-ag-finanzinvestor-kauft-maschinenbauer-pfaudler/11121518.html)

Even in the hands of a PE Fund, there has been very poor performance.

The big bet here remains on the Patel Family to turnaround the growth prospects of the company, it would be highly difficult considering the unit economics of running a manufacturing biz in Europe is a lot tougher than India.

If it was so easy, BKT would have had set up 2-3 plants in europe by now.

9 Likes

Yes. Even the management has guided lower margins in medium term. Existing shareholders like me have seen the mgmt. walk the talk and the market seems to have forgiven the recent PE exit shenanigan too (although the mgmt wasn’t involved in that and they didn’t hide their faces during that time). Waiting for SEBI to come out with results on that shenanigan too though. The play is long term costs being brought down using GMM Pfaudler and gaining global exposure.

1 Like

Yes, management will try their best as they are invested in personal capacity in Pfaudler Inc apart from GMM.

Can you explain how long term costs will be brought down using GMM Pfaudler?

Because if they needed technology transfer, they could have done it without the acquisition as well.

Costs would be brought down if the base of the international manufacturing is shifted to India, but here, they are running at near full capacity, meaning they need to do a mammoth CAPEX here in india. Now i dont think they want to stress the balance sheet more at this stage.

They could do something like what Honeywell is doing or what Grindwell wants to do but it will take a lot of time and effort for it.

Management said they want to bring around the change like they did with mavag. Mavag had a low ebidta before acquisition and they did turn it around.

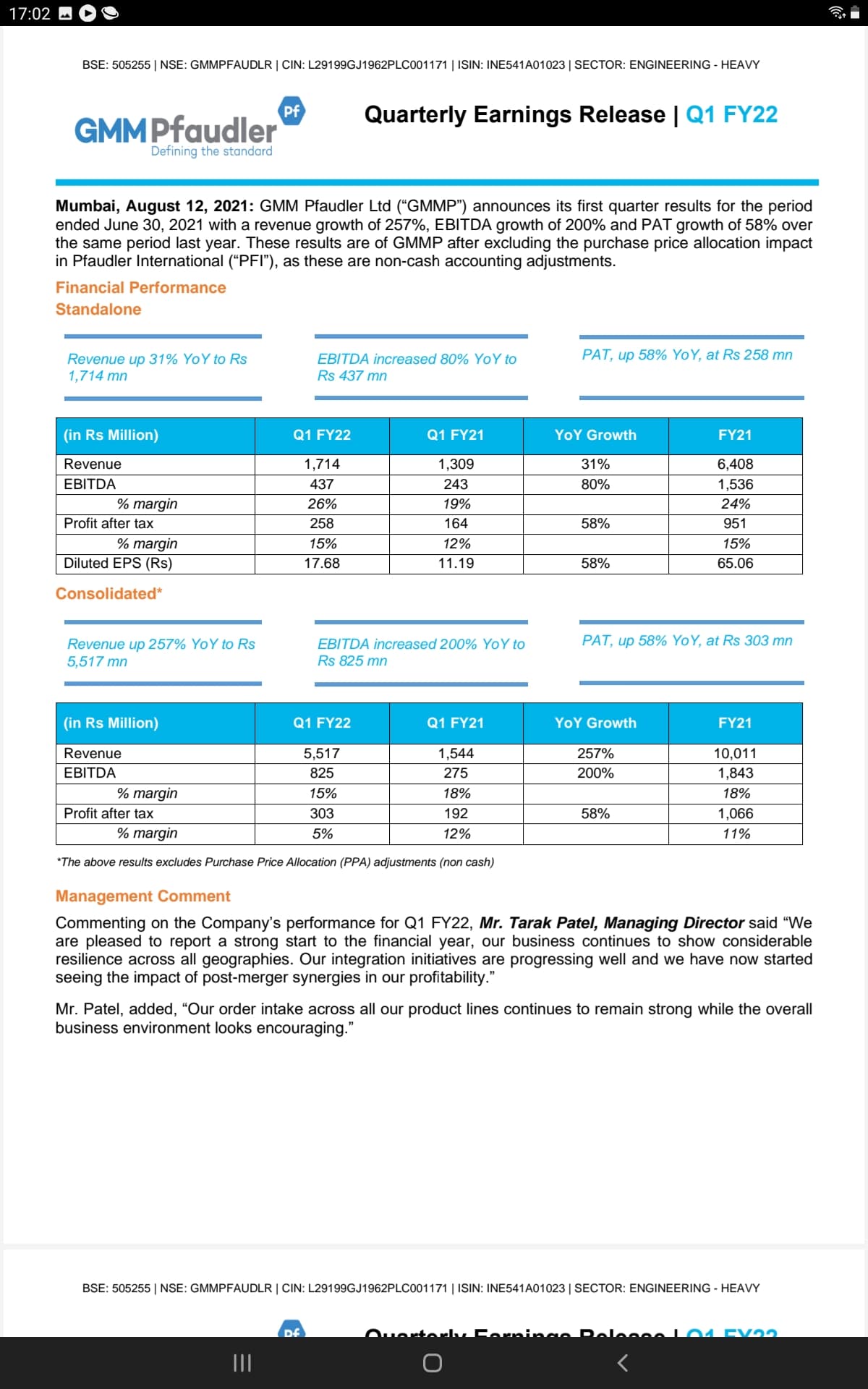

Q1 FY 22

Standalone performance is as expected very good on YoY 171 cr revenue, 26% EBDITA, 25.8 cr profit.( though decline on QoQ 190 cr rev/28% EBDITA/31cr profit )

Consolidated performance ( without PPA adjustment ) 551 Cr revenue, 15% EBDITA, 30.3 cr PAT.

Presentation with more details on integration and performance

In last concall management had said that 457 million will be charged for two months in this quarter.

Due to dollar increase it has become 465 million

First full quarter for integrated Organization, Execution delivery efficiency of management is visible across the board

- Sector tailwind Strong order books across geo - Consol group level backlog of 1700cr+, India/Mavag/Pflauder int- supported by industry CAPEX cycle of pharma & chemical.

- Increasing opportunity size - New vertical of Heavy engg is doing well, got large order from L&T for 100 Cr. This takes care of opportunity size in GLE space, They are also interested in growing “after service” part of biz which is higher margin( value adds)

- Pflauder performance turn around better than expectations ( good signs of conservative approach of mgmt in previous quarters), all signs visible of cross sell , EBDITA margin of international already near 10%( original guidance of consolidated 16% by FY 24, they will likely revise upwards soon)

- Synergies exploitation - standalone biz used to sub 20% margin historically, with global exports from India to contribute meaningfully, now standalone Biz EBDITA guidance is 24%+ going forward.

- Capex for two furnaces in India at Hyd and Guj, also in Brazil to support US demand

- Vatva facility contribution in HE segments and expanding more bays to accommodate backlog

- Past acquisition performance - Mavag was $5M revenue rate during acquisition, near future will do $25M run rate and now has $38M (swiss frank currencies )backlog - will leverage India

- Vatva at full capacity can do 400 cr+ revenues in near future

- PPA impact goes away from next Qtr, Amortization will be Q2-18Cr, Q3&Q4 6Cr/Qtr, 5cr/qtr for FY23

- Tax guidance of 25.6% in future for Int biz

- Consol Gross Debt $70M+, Net debt after cash $30M+

- Demand and backlogs - mgmt is extremely bullish and hence capex

Understandable that this is a complex acquisition scenario and markets don’t like uncertainty( plus episode of OFS pricing to significant discount to mkt price), however looking forward things are looking good and stable, signs of mgmt execution succes were visible in past( Vatva, Mavag), Pflauder is delivering too. Market may use its own wisdom and timing for performance/valuations over next 1-2 Qtrs, IMO agree with Tarak closing comments ONLY WAY FROM HERE IS UP

Invested - posted in past for projections here ( of course upside visible ) GMM Pfaudler: A safe way to play the Pharma/Chemical cycle - #187 by Dev_S

10 Likes