with new acquisitions on mixing business is a 3bn sector and service revenue part of the business is the runaway. Revenue visibility may improve

The reason for depressed price is that market has been punishing the company since the offer for sale. OFS was at price equivalent to 1750/share which at the time was at a steep discount to market price. Since then retail investors are probably worried about company taking such decisions again.

7 Likes

Here is a summary based on the transcript of their Q2 FY24 earnings conference call:

- FY25 Guidance: The company is confident of achieving its FY25 guidance of revenue CAGR of 14% and EBITDA CAGR of 24% over FY22-FY25E.

- Market Leadership: The company intends to maintain its leadership position and increased profitability in its core glasslined equipment (GLE) business, which has a global market share of 40% to 50%.

- Diversification: The company is expanding its non-GLE and systems business by cross-selling opportunities and exploring new application areas in segments such as oil and gas, minerals and mining, lithium, etc.

- Innovation and M&A: The company remains focused on innovation and M&A to drive growth. It recently acquired MixPro, a mixing company based in Canada, to strengthen its global presence and product portfolio in the mixing business, which has a market size of $3 billion.

- Order Visibility: The company has an order backlog of INR 1,705 crores, which translates to about 6 months of order visibility in India and about 7 to 8 months in the international business. It also has a strong opportunity pipeline across all business platforms and expects some large projects to materialize in the coming quarters.

6 Likes

3 Likes

4 Likes

1 Like

Source: Con-call decoder

GMM Pfaudler LtD

Current Operational Performance:

-

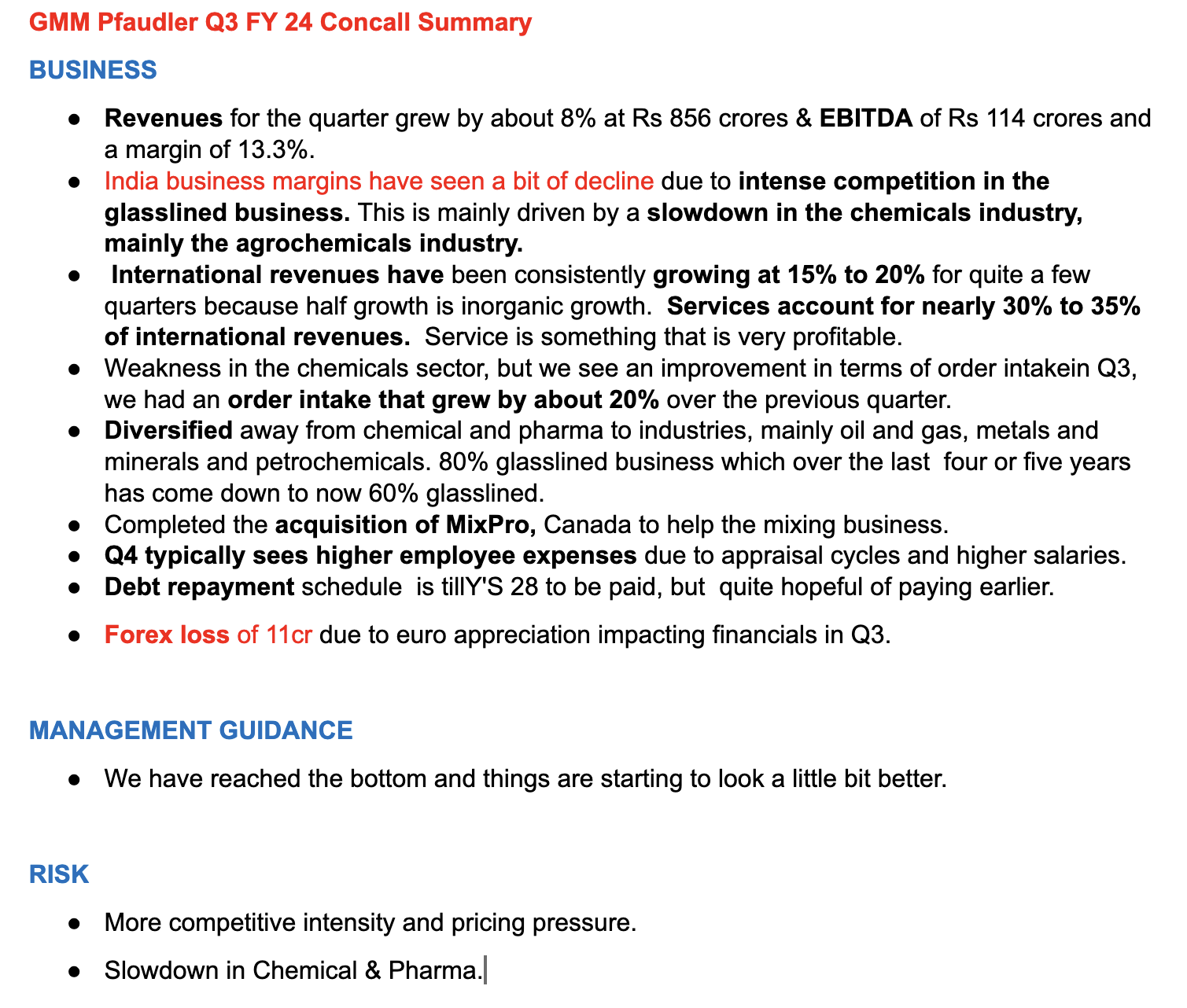

The order intake in Q3 displayed a substantial 20% growth compared to the previous quarter, boosted by a significant systems order worth $11.4 million from the U.S. market.

-

The international business experienced a noteworthy increase in order intake, placing a strong emphasis on establishing a robust backlog for the upcoming year.

-

A dedicated effort to diversify away from GlassLine was visible in the international business, particularly through advancements in non-GlassLine technologies, specifically the mixing platform.

-

Verifiable efforts to enhance profitability and cost efficiency were observed in the international business, focusing on consolidating footprint and improving profitability in the GlassLine business.

Future Outlook:

-

Management expresses confidence in the future outlook, with a clear focus on enhancing profitability and cost efficiency.

-

The priority is to build a robust backlog for the upcoming year, with a strong emphasis on enhancing order intake and sales performance.

-

The international business is anticipated to continue its growth trajectory, with a targeted approach to diversify away from GlassLine and improve profitability in non-GlassLine technologies, particularly in the mixing platform.

-

Management is optimistic about the growth potential in the service business, emphasizing response time and spare parts availability.

Concerns:

- While the international business faced some pricing pressure, it was not as significant as the pressure experienced in the Indian market.

- The Indian market saw pricing pressure, especially in the GlassLine business, due to intense competition.

- The chemical sector’s challenges resulted in a slowdown in the GlassLine business, particularly within the agrochemical industry.

Other Points:

- The international business remained focused on diversifying away from GlassLine, demonstrating significant advancements in non-GlassLine technologies, notably in the mixing platform.

- Efforts to improve profitability and cost efficiency were evident in the international business, with a strategic focus on footprint consolidation and enhancing profitability in the GlassLine business.

- The international business saw a substantial increase in order intake, emphasizing the establishment of a strong backlog for the next year.

- Emphasis on diversification away from GlassLine was consistent in the international business, particularly with notable strides in non-GlassLine technologies, specifically in the mixing platform.

10 Likes

My initial impression was that the company is doing too many acquisitions in a short span of time. But looks like there is a very clear strategy of seismic shift of focus towards mixing solutions, coz it opens up more avenues for the firm. I had a question on valuations - seems like there is a downwards trend in the stock since the last six months or so. Part reason is clearly the slowdown in mother industry for their largest revenue segment - chemical and pharma. Is there something else the market is factoring in?

Also - besides expanding avenues, is the focus on mixing solutions a part of managements plan to be less dependent on cyclicality in pharma and chemicals?

Expert views awaited - cheers!

3 Likes

@Mayank_Bajpai please elaborate more on what is Con-call decoder

1 Like

Back in FY21-22, company was growing in excess of 80% YOY topline, thus market was rewarding it with a Pe of 80-100.

Problem with growth stocks is when growth rate slows , their Pe de-rating starts happening.

Even though company is growing for last 3 years the rate at which it grows has significantly tapered.

Thus price and time correction has happened.

For earnings to catch up with the price of the stk.

Same thing has happened with Dmart and bajaj fin over the last few years.

8 Likes

Given the flat guidence for both FY-24 & 25.

It’s a simple guess that stock won’t do much for next 12 months, provided margin expansion happens in FY25.

Hope the PE re rating happens, since they have diversified the portfolio and has a leadership position in the segment.

Disclosure : Invested.

2 Likes

Managment is focussed on progressing on allied segments while maintaining dosmetic market share in Glass lined segment. Management being very conservative in the guidance makes me think that it can be well achieved or may be exceed.

Pharma and Chemical cycle looks to be bottomed out too which further can accelerate GMM’s performance.

Though easier said than done but I’m hopeful and bullish on the management.

Disc - Invested

4 Likes

I too have been closely following Gmm pfaudler. After years i am seeing this below 30 pe now and my guess is that this is because of pharma downturn, too many ownership transfers. It does feel that there might not be exciting growth for next few quaters but certainly seems like good opportunity to start creating position. Lot of growth triggers are there per my opinion - leadership in glasslined equipment, good growth in the mixing portfolio, higher share coming from services which is high margin and also repeatable/ less cyclical business.

Disc - Biased and tracking closely with minor position

9 Likes

Sometimes back (Can’t recall clearly) in one of the concall, I heard that they are also working on lab grown meat.

Am I in my senses? ![]()

2 Likes

Yes, I remember this from one of Marcellus’s webinar with Tarak Patel. As far as I can recall, they mentioned working with a US company (possibly Beyond Meat).

2 Likes

Disc: Biased and invested. not a buy or sell recommendation

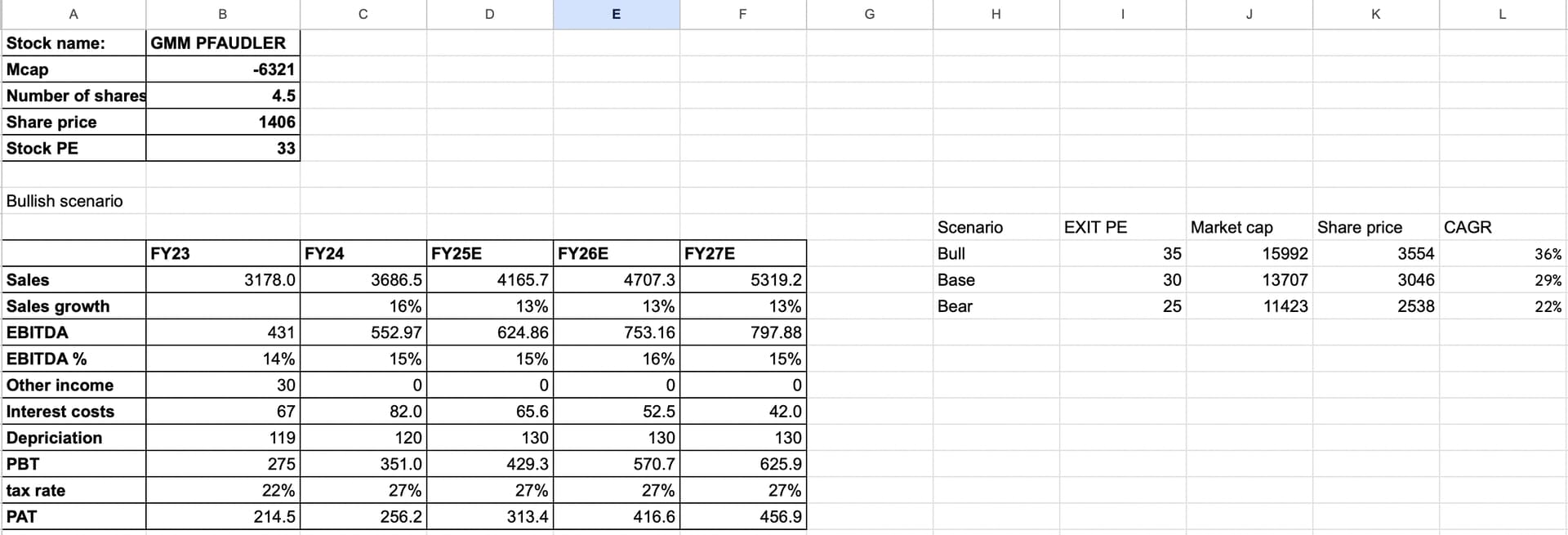

Thesis

The business is on track to reach 3700 crore revenue by end of FY24 as the first half suggests(This was written before Q3 FY24 results, if one thinks 3700 might not be possible, we can assume 3600 as well)

They do expect a 13-15% revenue guidance and 18-20% improvement EBITDA. I am not concerned about revenue growth as chemical cycle should turn some day, I am fine waiting for it.

The promoters are already conservative but I still took the lower end from FY26 onwards

EBITDA margins too should improve as the share of services and high margin businesses like mixing increase.

I don’t expect them to go down unless chemical and pharma sector continue their slowdown or steel price rises rapidly

Which is a bit unlikely

I again went a little conservative and went to about 15-16% compared to the 14% last year

50% of EBITDA is free cash flow and hence, interest costs should go down, they expect to be completely debt free in 2-3 years but I only decreased it by 20% each year

64 crores is interest cost, 16 crores is related to forex so that might still stay.

Depreciation might increase a bit as capex will be required to meet these goals and they do plan to acquire mixing businesses

And 27% tax rate as the company stated

Possible antithesis

The business is largely dependant on Chemical and pharma sector. Any slow down in these businesses will mean that all proxy manufacturers fight for the same order book and hence margins get depressed, which is what has been happening in FY24.

Another issue is the impact of commodity price of Steel.

They have exposure to a lot of international markets, China and Germany are both showing signs of slowing down with chemical companies in Germany moving their manufacturing to other countries

However, they are well diversified and such issues could be offset by other countries.

Moreover, acquisitions in mixing businesses and other industries have a high profile margin, so even that picking up will offset these setbacks.

4 Likes

Can you please share your CAGR calculations? As per me if earnings is growing from 256CR to 456CR over 3 years it is a 21.22% CAGR, so assuming PE remains same at 33 the share price growth should be the same right?

1 Like