The performance of the company’s stock price is very weird, it has not really moved since the covid crash, but whereas the NP CAGR and Sales CAGR have outperformed the stock price, anyone wonder why?

Probably it ran more than it should in everything bubble and now in time correction. One can always observe most of the chemical stocks were in multi year consolidation phase prior to 2020 esp. COVID era darlings. We never know when they will break out again. Especially now that Chinese factories are back online they are exporting their deflation mainly in all commodities. This is hurting our companies as well.

the stock was very overvalued back in 2021 or so when it peaked. A capital good can not command 50-60 PE multiple. It’s just that the earnings are finally catching up to the stock performance. Its fairly valued now I think

Earnings have been in negative growth from last few quarters. Order backlog is falling from almost an year. New order intake is lower than the revenue, for the last quarter order intake is around 750 crore while revenue is 850 crore. Unless the order intake shows growth there is no way stock price can move up.

is there any other reason for stock price degrowth?

Reason being rich starting valuations (Marcellus owned stocks trade at premium)

GMM and HLE’s business is front ended and you would have seen these guys getting business from chemical and pharma players as they were setting up capacity in 2019-2020. So their fortunes are closely tied up with these guys doing well and setting up capacities of their own. But hopeful of their revival in coming Qtrs. Tracking closely.

GMM is also focussing on non glass lined businesses, therefore there margins and revenue not picking up due to slowdown in chemical & pharma (though looks like improving gradually) and capex in non glass lined.

The guidance itself is very conservative which means they don’t want to create unnecessary hype.

What drives me towards the company is the management (acquiring the parent company) and expanding overseas. Sooner rather later the glass lined business will perform. The OPM is around 14% since 4 FY’s and not so volatile since 8 quarters, that proves management’s calibre.

Invested and tracking closely.

They are currently working on diversifying the business away from the usual end user industries. Which increases their terminal value and makes them less volatile. Optionalities have increased which should be something a Long term investor should like

What exactly happened today? Market started off with ~12% upswing on very high volumes, but as the day progressed, it fell down and closed with mere 2-3% gain. As per Trendlyne data, there has been change of hands, Geranium Investments has sold ~37 lakh shares and Infinity Partners has bought ~41 lakh shares

Also, I think people who have been caught up here since a long time got an opportunity to off-load their “Coffee Can” stock after long period of frustration, which is what lead to day-close being significantly lower than day-high. I have recently picked up “Profiting in Bull and Bear Markets” by Stan Weinstein, and am trying to connect dots on the stage analysis framework for this counter, based on today’s action. Anyone one who has practised his methodology longer - can please shed some light?

GMM Pfaudler has had 50% sales cagr and 30% profit cagr in both last 3 and 5 year periods. Sales is 6X in last 5 years but the stock price is flat. This is one of the dangers of buying stocks at high P/E. This stock has almost no analyst coverage despite having such good sales and profit growth numbers

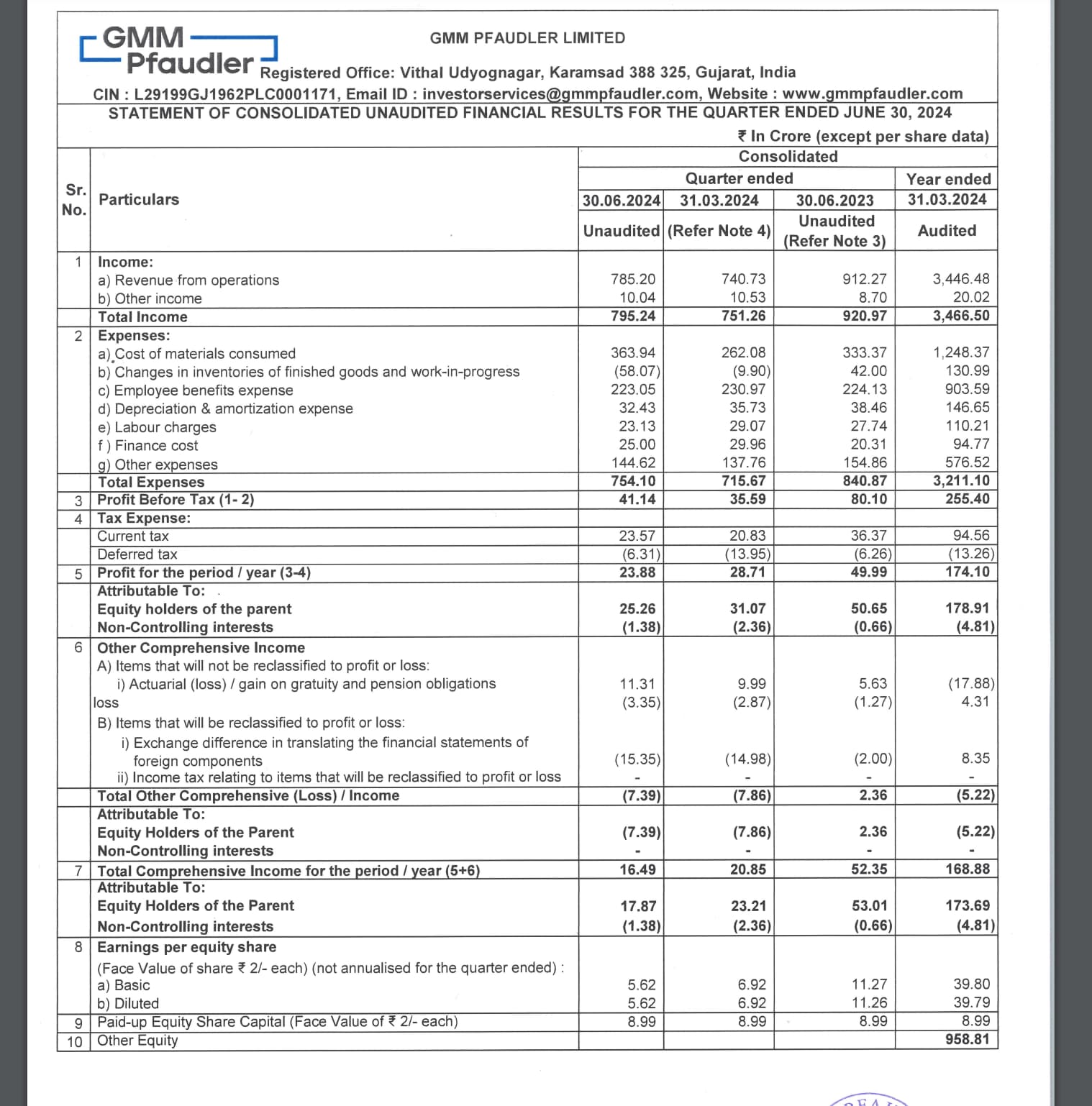

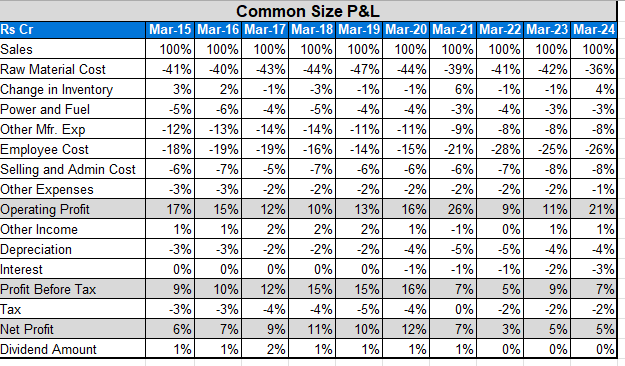

The common size P&L is very confusing. Looks like raw material cost came down in last quarter and that led to OPM improvement. However in the past raw material costs were higher and still OPMs were higher. Don’t know why SG&A expenses are increasing rapidly

Very low Net profit margins that are now 5% or so from 12% when it was growing sales rapidly. There has been an increase in interest expense from the capex expansion that happened in 2021 of 963 cr. The capex has brought in additional sales as we see in the sale cagr but the interest has hit the NPM %. Decline in market cap is due to P/E contraction as the earnings growth is very good in 1-3 years periods.

This seems like a good pick now

At a price of ~900, this seems to be a ‘fallen angel’ stock with a global leadership position. Order book rapidly growing in non-Pharma/Chemicals sectors.