Absolutely right choice for long term

1 Like

1.Like Radico Khaitan, they are also trying for Prestige and above segment but have not yet created their own market. In the Value segment market, pressure on margin still exists.

2.Management seems to be comfortable with revenue from sub-contracting work for Diageo , Bacardi and bulk Alco.

3. Ready to drink segment: very early-stage funding and small market as compared to Alco market.

5 Likes

Concall notes FY24 Q2

Resilience Amidst Supply Disruption:

- Overcame 18-day supply halt from FCI swiftly.

- Bengal plant adapted, produced ethanol from maize.

Market Dynamics and Adjustments:

- Faced FCI ban during peak rice and maize prices.

- Despite customer price revisions, experienced margin compression.

Outlook for Margin Improvement:

- Anticipating increased margins in Q4 with favorable kharif crop.

- Considering in-season raw material storage to manage volatility.

Operational Updates and Expansion:

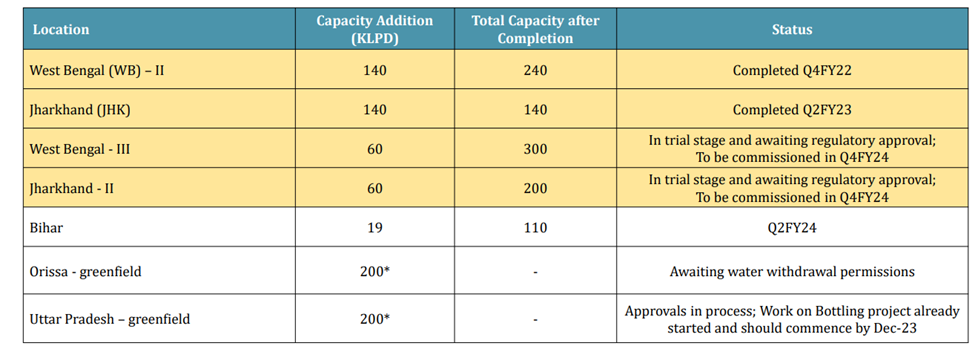

- Awaiting regulatory nod for additional 120 KL capacity.

- Jharkhand and Bengal expansion to reduce production costs by 5%.

- Stable fuel costs maintained with technology upgrades.

Strategic Initiatives and Brand Performance:

- Secured one-third of fuel demand through recent auctions.

- Boiler technology upgrade in Haryana underway.

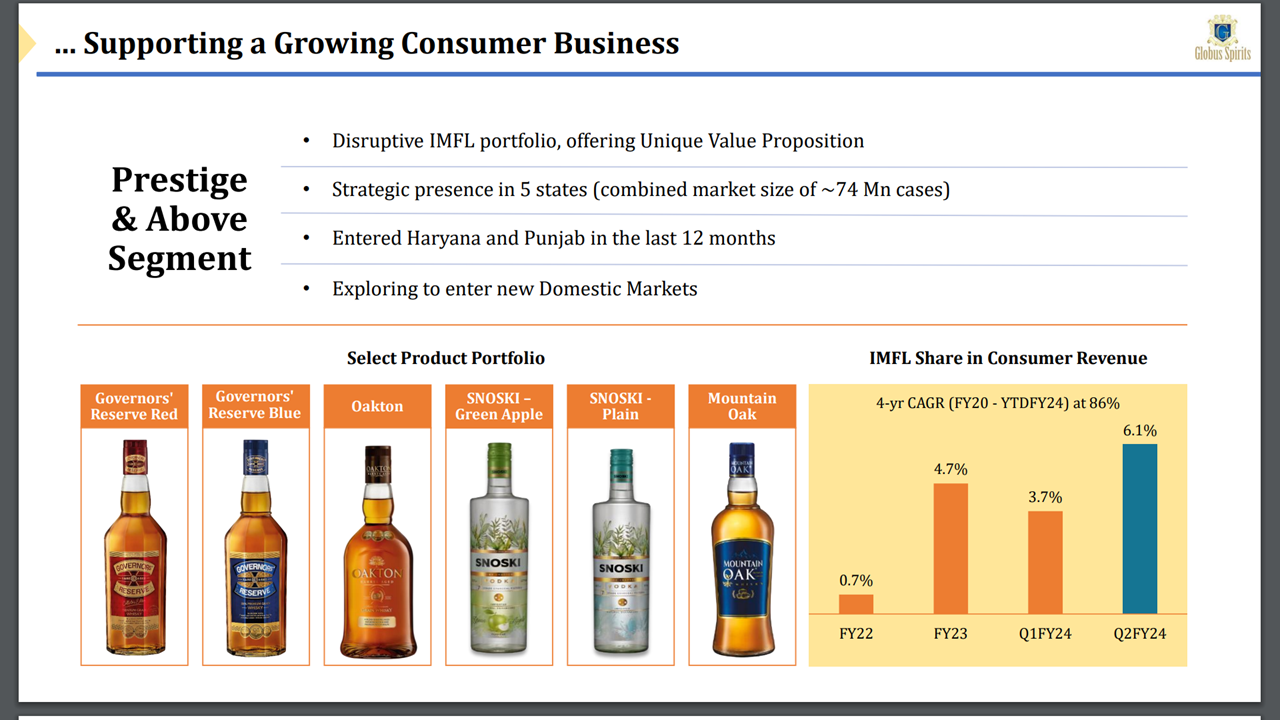

- Prestige brands gaining momentum with innovative offerings.

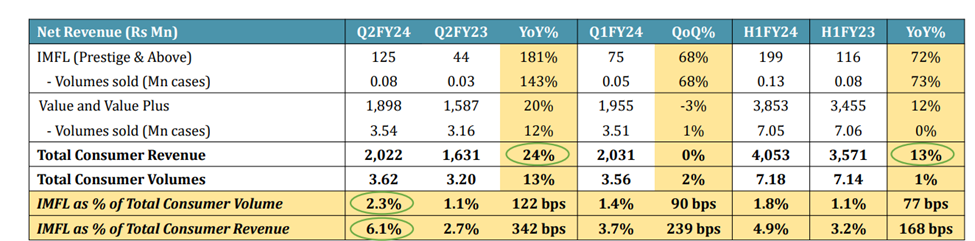

Consumer Segment Summary:

- Premium Segment Surge:

- Q2 volumes: 0.08M cases, up 143% YoY, 68% QoQ.

- Prestige brands contribute 6.1% to total consumer revenues.

- Geographic Reach:

- Presence in UP, West Bengal, Delhi, Haryana, and Punjab.

- Robust routes in Delhi, West Bengal, and Haryana; plans for UP, Punjab, Rajasthan (Q3), and Jharkhand (Q4).

- Revenue Growth:

- Total consumer revenues up 24% YoY in Q2 FY24.

- Mountain Oak Whisky expands nationwide.

- Product Momentum:

- Terai Craft Gin broadens distribution.

- Snoski Vodka expands in Haryana, West Bengal, and Delhi.

- New launches in premium rum (Q1 '25) and super premium malt whiskey (Q4 '24).

- Strategic Branding:

- India Craft Spirit Company consolidates highest price offerings.

- Utilizes four generations of promoter’s alcohol industry history.

- Value and Value Plus Success:

- Volume growth: 12% YoY to 3.54M cases.

- Average realization grows 9% YoY to INR 558 per case.

- Global Green captures 5% market share in whiskey flavor.

- Market Dynamics:

- Rajasthan market share: 35% in Q2 FY24, up from 34% in Q2 FY23.

- Dominates Rajasthan with a 61% market share in the value plus segment.

Financial Highlights from Q2

- IMFL Loss and EBITDA Burn:

- IMFL loss in Q2: INR 6.5 crores.

- Projected annual EBITDA burn: 20-25 crores, with a potential decrease as volumes increase.

- Ethanol Procurement and Pricing:

- OMCs’ ethanol procurement tender underway.

- Current ethanol prices: 64 for rice, 66 for maize.

- Prices for the new year pending, expectations of stability in rice prices and potential action on maize ethanol.

- Impact of FCI Rice Procurement Challenges:

- 18-day disruption led to production halt in Bengal and Jharkhand.

- Shift from FCI rice to maize and broken rice impacted profitability.

- Estimated impact: INR 5 to 7 per litre for subsequent supplies.

- Expected 8% decrease in grain costs in H2, impacting from December to March.

- Power and Fuel Costs:

- Power and fuel costs fluctuated between INR 1.8 to INR 2 per GCV.

- Absolute power and fuel spend for Q2: INR 59 crores.

- Net Debt (as of September 30, 2023):

- Net debt, excluding cash and cash equivalents: INR 235 crores.

Business Strategy and Expansion Highlights:

- Product and State Metrics:

- Key products include Governor’s Reserve, Oakton, Mountain Oak, Terai Gin, Snoski, with new launches in premium malt whiskey and rum.

- Strong presence in West Bengal, Delhi, and Haryana; upcoming launches in UP, Punjab, Rajasthan, and Jharkhand.

- IMFL Business Growth:

- Vision to invest in and strengthen the IMFL business.

- Aim to achieve 20% of consumer business share from IMFL.

- Focus on diverse portfolio and innovation alongside established products.

- Innovation and Brand Strategy:

- Ongoing innovation, e.g., launching a new flavor for Snoski.

- Emphasis on transformative products for brand success.

- Core products like Mountain Oak, Oakton, and Governor’s Reserve for market presence.

- Market Dynamics:

- Stronger market presence in West Bengal, Delhi, and Haryana.

- Expansion plans for UP, Punjab, Rajasthan, and Jharkhand in the next six months.

- Consideration for launch in one additional new state.

- IMIL Business Expansion:

- New launches planned in Haryana, Delhi, Rajasthan, and West Bengal.

- Limited expansion in other IMIL states like UP and Punjab.

- Strategic decisions aligned with business priorities.

Highlights:

- Utilization:

- Q3: Expected 80-85%, pending consent for expanded capacity.

- Q4: Full capacity utilization target at 95%.

- Financial Impact:

- FCI disruption, higher grain prices: INR 42 crores impact.

- Anticipated profitability improvement post-Kharif season.

- Revenue Composition:

- Ethanol: 30-35% of overall revenue.

- Stable ENA pricing; Q3, Q4 seasonal uptick expected.

- Raw Material Strategy:

- Maize as key input; ongoing farmer education.

- Short-term: Rice primary for Bengal plant.

- Capacity Expansion:

- Capital work: INR 155 crores; INR 115 crores expected to be capitalized in H2.

- Upgradation ongoing; Bengal, Jharkhand expansions.

- Packaging Costs:

- Marginal impact; glass cost up, offset by reductions in CC box rate, reduction in paper prices and pet resin prices

- Costs in material consumed, not in other expenses.

- Revenue Diversification:

- Active management of ethanol, ENA sales.

- Utilization of leftover ENA capacity through ethanol sales.

- Capex and Depreciation:

- Expected INR 100 crores capitalization; total capex INR 115 crores.

- Constant depreciation in H1.

Ethanol Pricing Outlook:

- Anticipates slow reaction from oil companies to market changes.

- No significant price increase expected in the next few weeks.

- Government’s E20 blending mandate likely to influence price revisions.

Potential Downward Revision:

- In case of sustained low prices, possibility of downward revision.

- Long-term sustained reduction could lead to a downward adjustment.

Timing of Price Revisions:

- Price announced at the end of October for the next year.

- Revisions happen as needed, not limited to specific timings.

Business Margin Impact:

- Majority of margin reduction in manufacturing business.

- Consumer business also impacted, but not the primary contributor.

Price Increases and Consumer Business:

- Consumer business experienced margin reduction due to raw material price increase.

- No price increases in the consumer business contributed to margin challenges.

Sustainable Margins for Blended Business:

- Depends on the growth rate of the consumer business.

- Growth rates in Value, Value Plus, and IMFL show promise.

- Further guidance contingent on raw material price correction in December and Q4.

Future Guidance and Considerations:

- Waiting for new crop and raw material market stabilization.

- Plans to store inventories during the seasonal downturn.

- Longer-term guidance and sustainable margins assessment expected after the raw material price correction.

- Anticipates some price increases in the consumer business around February, March, and April.

FTA Agreement Impact:

- Immediate benefit: Reduction in scotch prices used in blending.

- Increased competitiveness of scotch in the country.

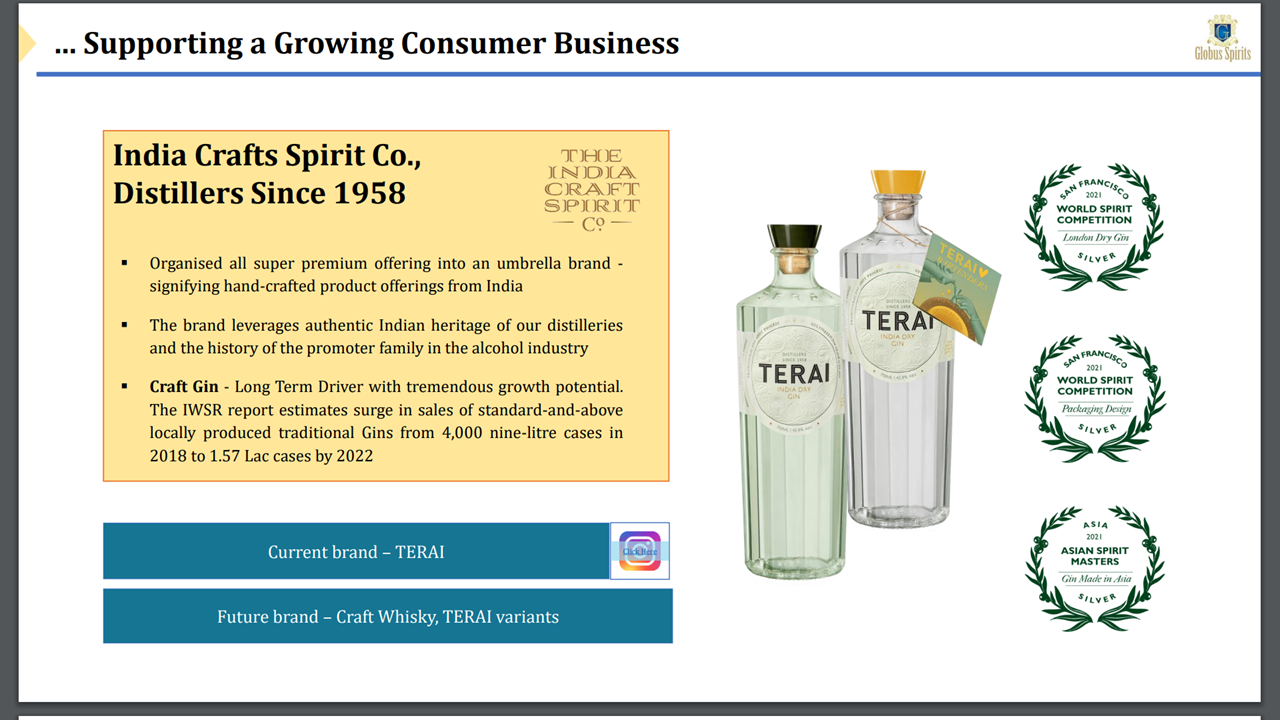

International Market Exploration:

- Immediate focus on TERAI for exports.

- Global interest in Indian spirits industry gaining momentum.

- Aim to establish Indian spirit brands with sustained global presence.

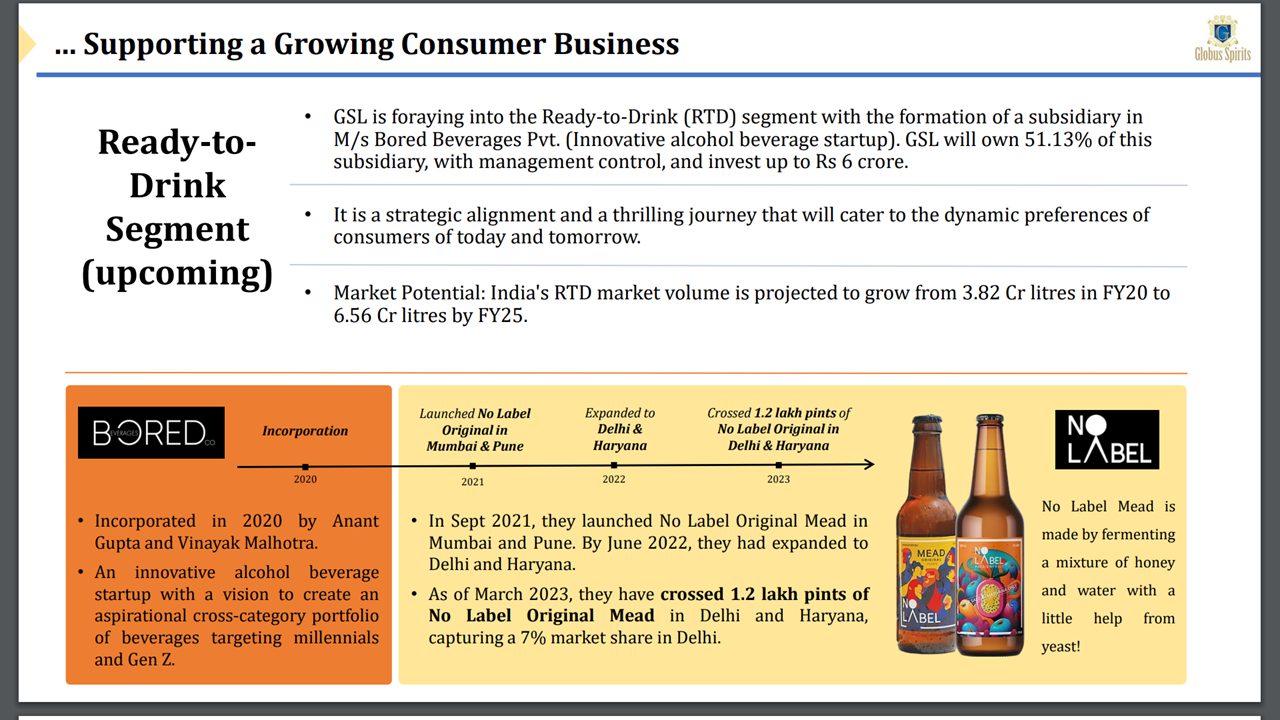

Bored Beverages and Market Expansion:

- Initial focus on Delhi and Haryana.

- Future expansion to align with Globus Spirits’ operations and premiumization strategy.

Possibility of Globus Brands in Mumbai and Pune:

- Bored Beverages currently not operating in Mumbai and Pune.

- IMFL business initiated with Terai Gin; other brands to follow.

- Maharashtra entry prioritized based on strategic value and profitability.

- No specific timeline provided; not a current priority market.

Consumer Business Revenue in Q2: Seasonal Softening

- Q2 typically softer than Q1 due to excise year dynamics.

- Q1 sees inventory replenishment, new players entering the market.

- Q3 tends to be higher with festive seasons in October-December.

- Q4 may show softening as business partners prepare for excise policy renewal.

Franchise Bottling Impact and Outlook:

- Franchise bottling is a small part of revenue.

- Impact observed in Q1; management expected normalcy in Q2.

- Current status indicates persistence of impact.

- Difficulty in predicting future growth as it depends on fortunes of brand partners.

9 Likes

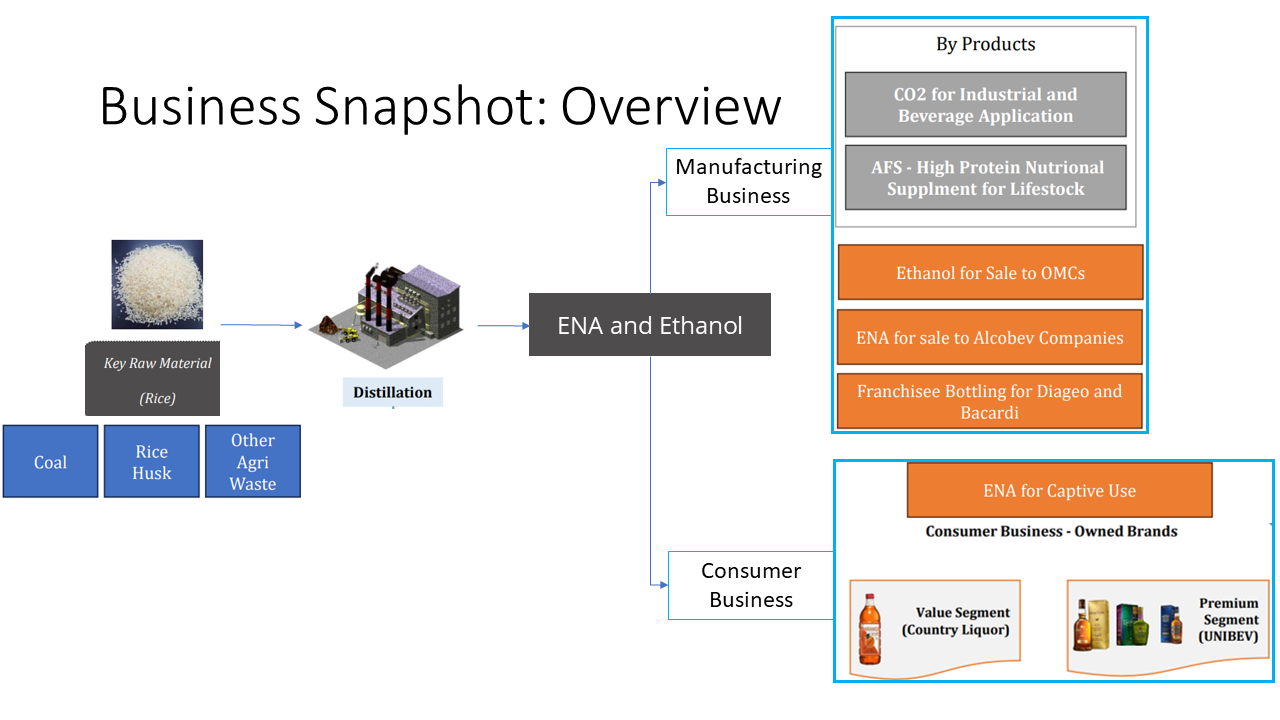

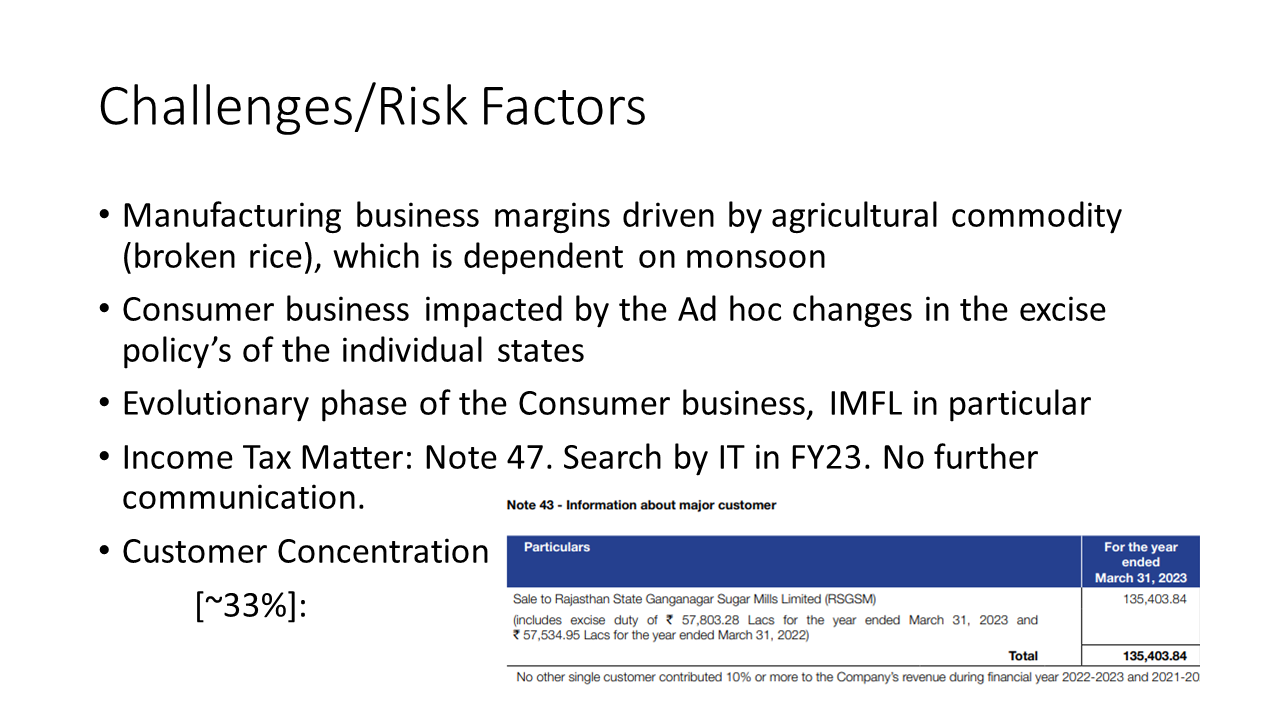

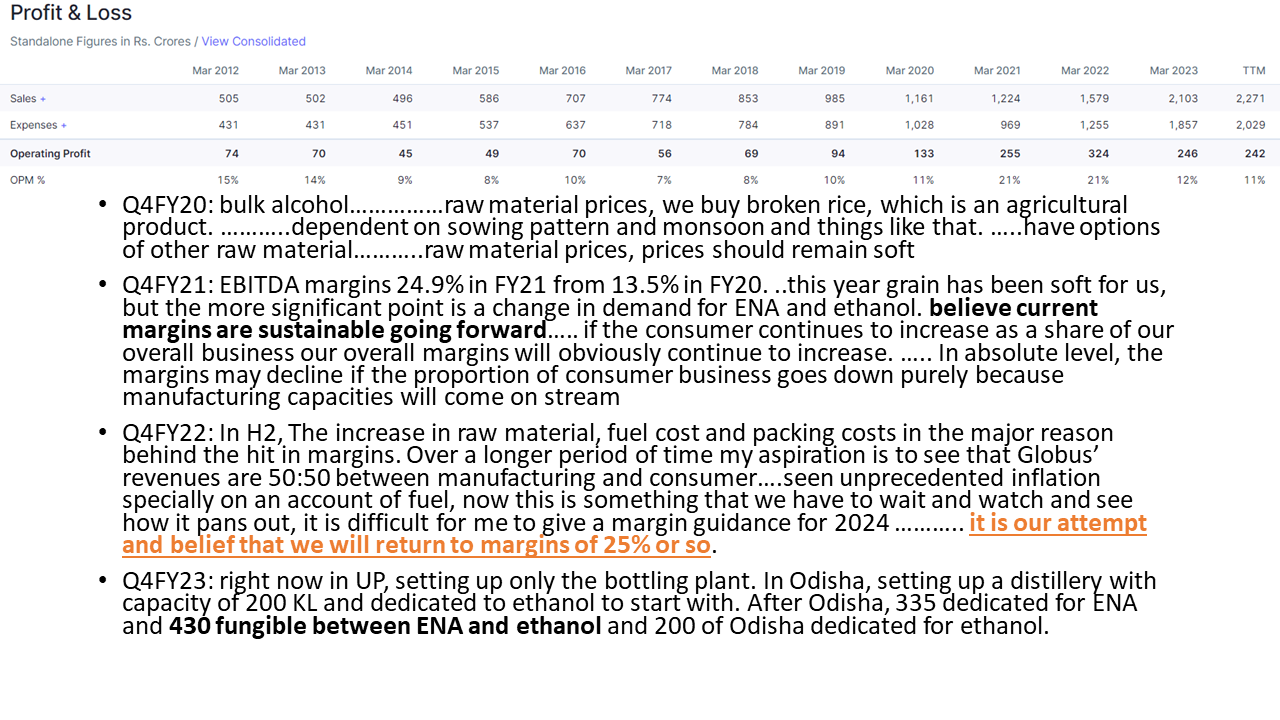

The company had a very tough time in the past 8 to 9 quarters. As far as input costs are concerned, I don’t think the situation could get any worse than it is. The only silver lining could be that there were no issues in offtake by OMCs. Broken rice prices started moving up first followed by the power prices. After the coal prices came down there was some respite in power prices. But then broken rice prices started going through the roof. Then, the company was able to procure rice from FCI at a fixed price but with Govt stopping supply of rice Globus had to buy rice and maize from the market.

Even in such adverse market conditions, Globus was able to increase its quarterly sales from 382 cr in Sept’21 to 567 cr in Sept’23. However, the margins fell from 23 % to 7 %.

One of the major reasons for the fall in margins is raw material prices. Also, the increased contribution from the bulk segment is another factor. With newer capacities coming in the contribution from the bulk segment has significantly increased. Also, the company started investing in marketing for their prestige and IMFL division.

Demand for ethanol remained strong with prices revised multiple times by the OMCs.

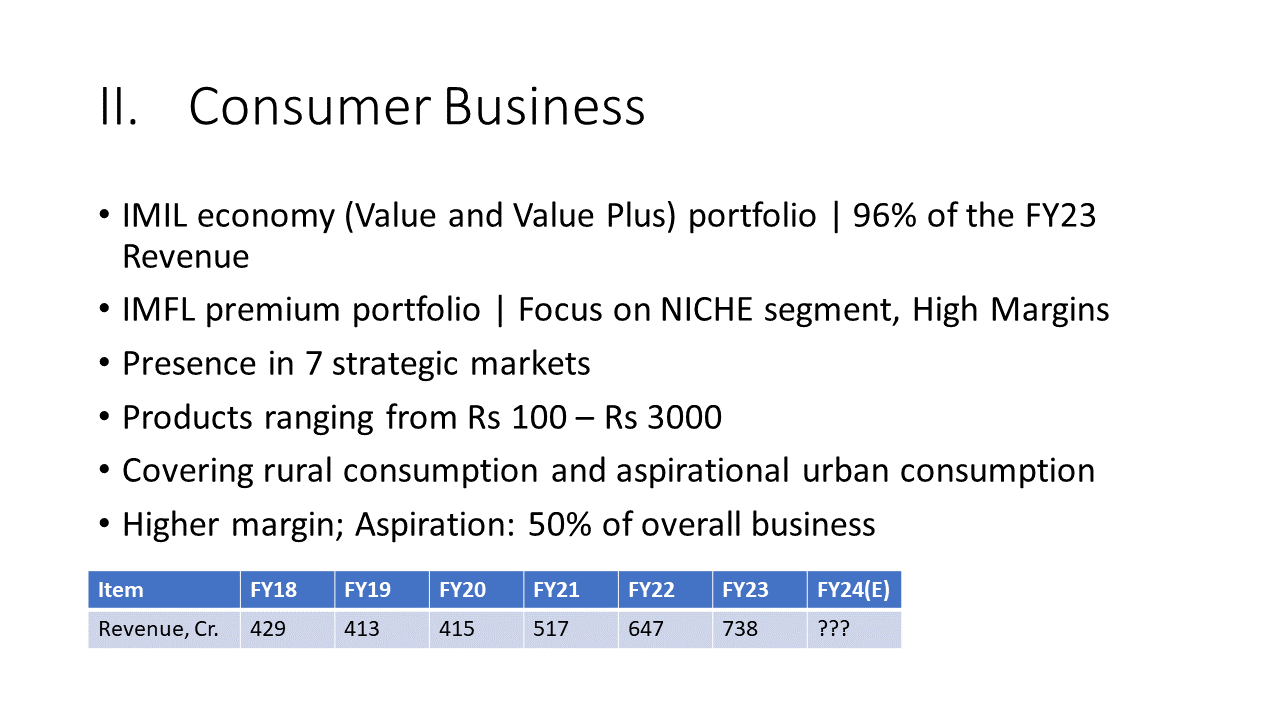

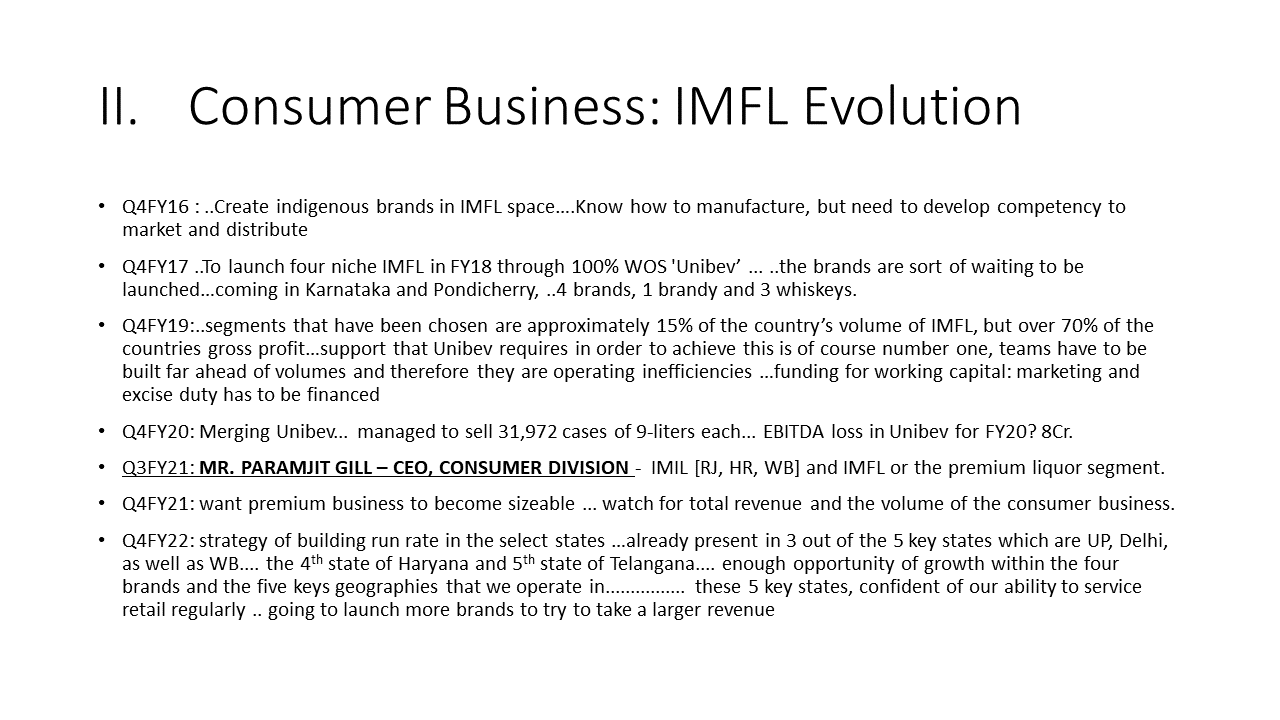

The company sees the IMFL segment to be the growth driver for the company.

Company’s presence

The company has an IMIL presence in Rajasthan, Haryana, West Bengal, and Delhi. Globus dominates the Rajasthan market as far as value and value-plus segments are considered. They were able to further strengthen their market share which is now 35 % of the value segment and 61 % in the value plus segment. The company has plans to foray into one new state in IMIL. However, they have not disclosed which state it is. Doesn’t have plans to move into the IMIL business in Jharkhand and Orissa. Must be UP.

The company has not been able to gain any major market share in West Bengal. The company has blamed the route to market for this.

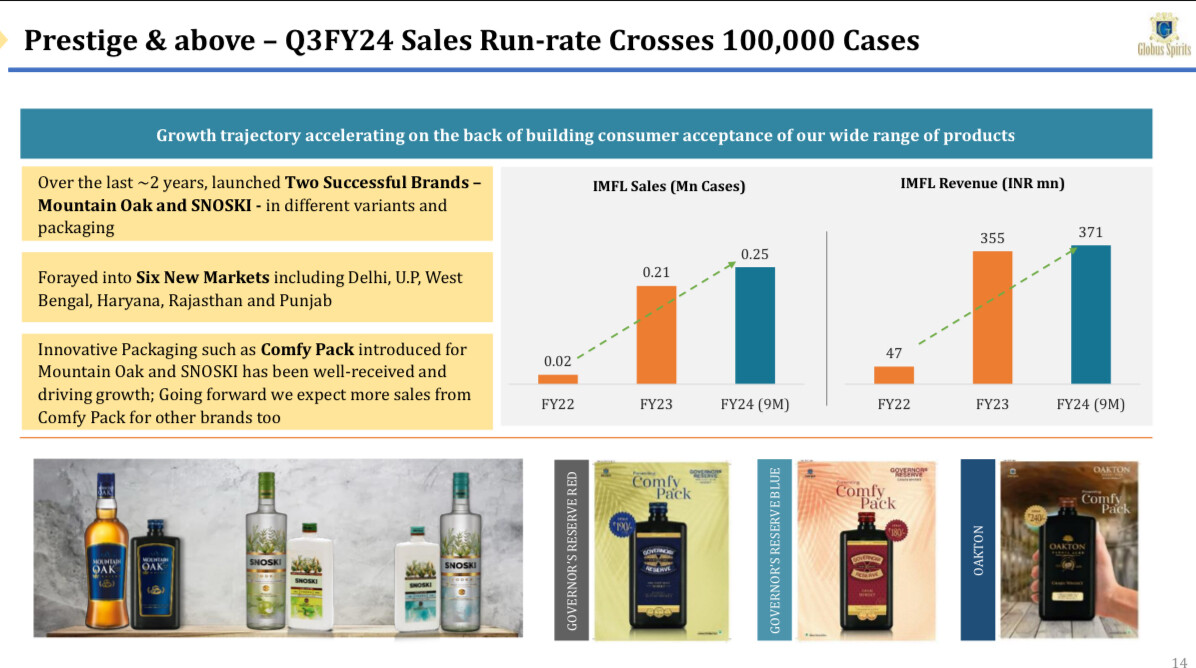

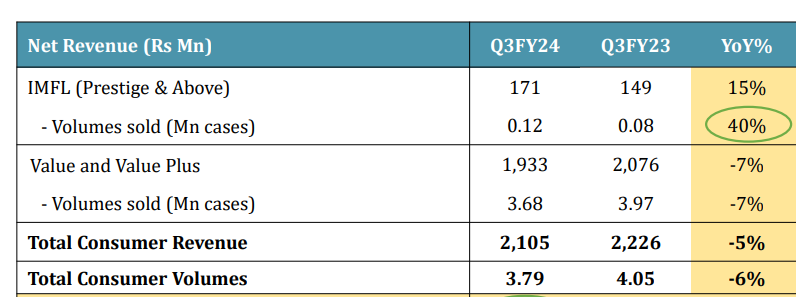

IMFL revenue is currently 6.1 % of the consumer revenue

They have a presence in Delhi, West Bengal, Haryana, Uttar Pradesh, and Punjab. They entered Uttar Pradesh and Punjab in the last year. Have plans to enter Rajasthan in Q3 and Jharkhand in Q4. I am very positive about the company’s foray into Rajasthan. The company has a very good presence in the state for a very long time. However, the company has mentioned that the distribution and marketing required for IMFL and the value segment are very different.

As per the management, it may take 3 years for the IMFL business to stabilize in a state. Marketing of a brand is not going to be easy.

Debt and other metrics

Debt has increased significantly over the last year with the company increasing its capacity aggressively.

Debt increased significantly to 291 crores in March’ 23 from 180 crores in March’22, which further increased to 352 crores in Sept’23. However, the company mentioned that they reduced the debt by 37 crores in last quarter. It seems that debt repayment is something the company will focus on going forward. The good thing is the cost of debt is close to 4 % which is keeping the interest costs at the levels we see now.

Trade receivables and inventories have also made a huge quantum jump, which could be due to higher contributions from ethanol sales. The effect of this is offset partially by the increase in trade payables. Going forward inventory days may go up as the company informed that they may start stocking up raw materials in the season from next year onwards. The working capital and conversion cycle may get extended due to this.

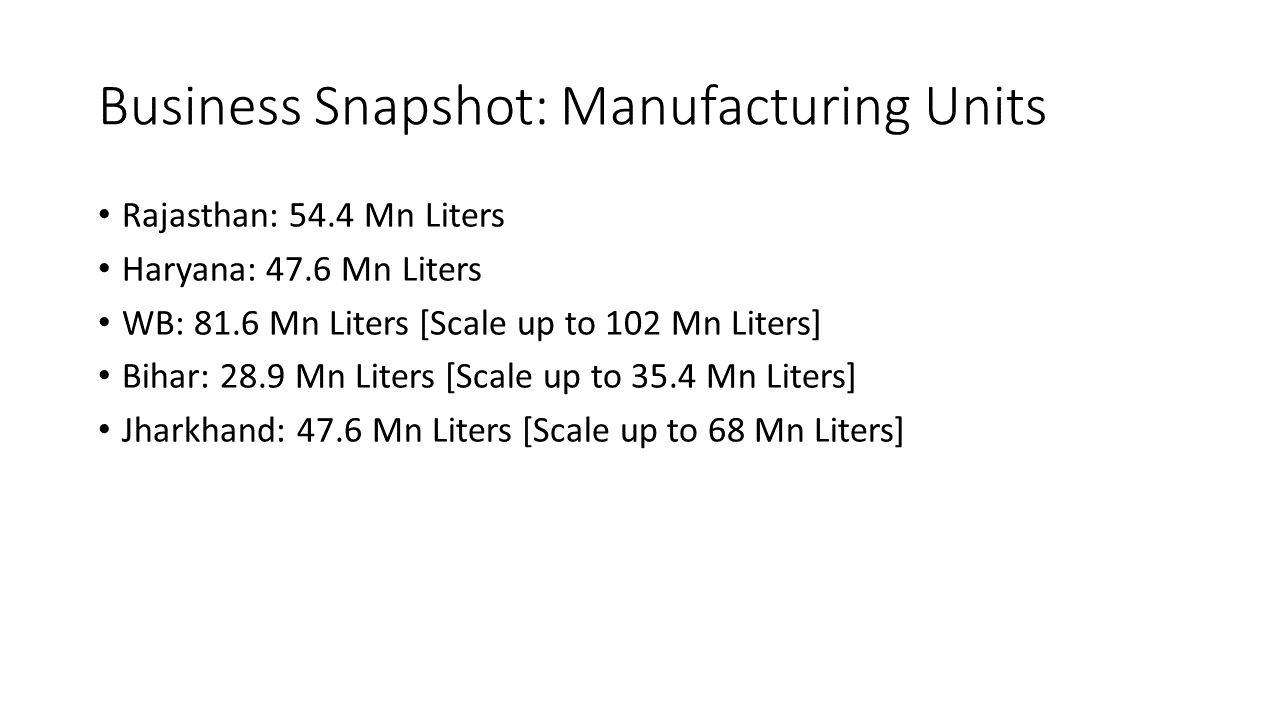

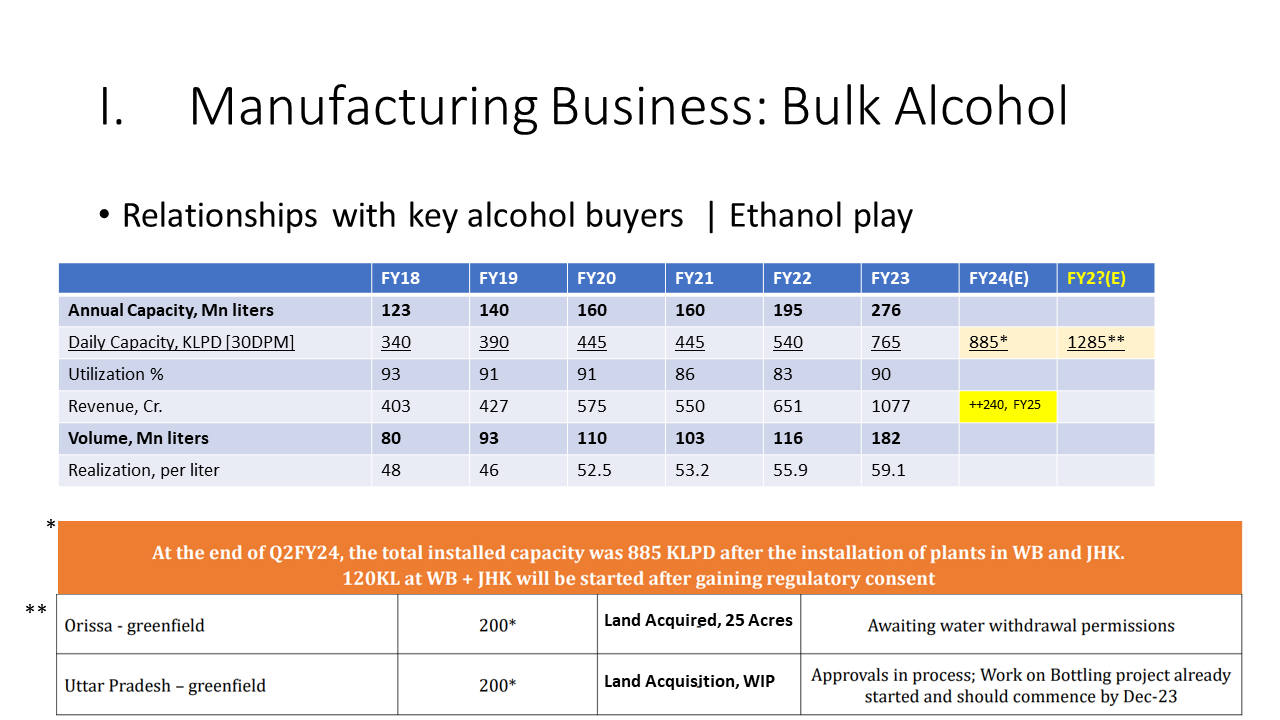

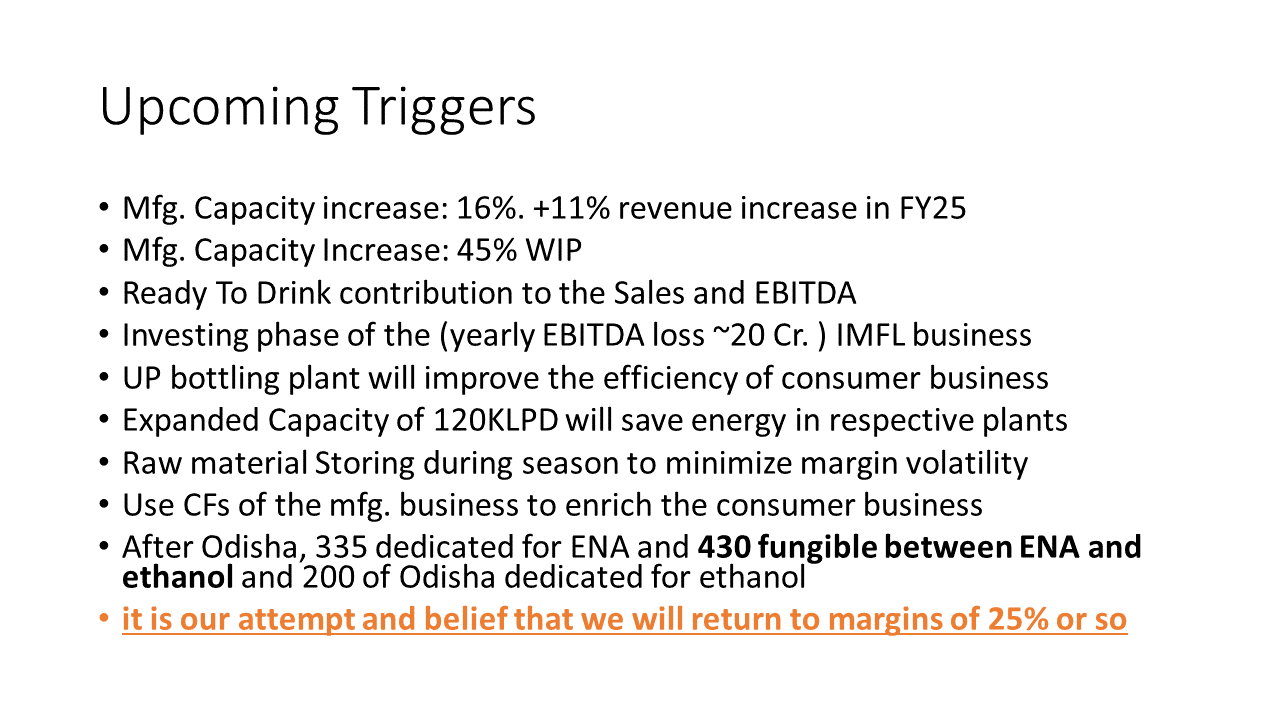

Capacity Expansion

An additional capacity of 120 KLPD will be onstream in Q424. The bottling plant is expected to commence in Dec-23. The bottling plant seemed to be of strategic importance in bringing down the costs of consumer business.

The company expects margins to start increasing from Q424. With the Kharif crop season, the availability of rice may increase bringing some respite to prices. However, as per forecasts, the rice crop is expected to be lesser than last year even though the area under paddy cultivation is slightly higher than what it was last year.

10 Likes

Sharing the note on GSL that I prepared to understand the business:

Vauation w.r.t Own Past Multiples:

Vauation w.r.t Peers:

Disclaimers:

- No position

- Not a SEBI Registered professional

- Do your due diligence since it’s your money at stake

- Shared for learning purpose and not a recommendation

- Sources: Result Presentations | Annual Reports | Conference Calls | Company Website | Screener.in

17 Likes

Thanks for this excellent analysis and sharing it with fellow investors. While the sales growth and operating profit are more or less comparable across all the players (except Radio), any reason why the market is not giving a favorable PE for Globus on par with other players?

In my opinion, others are valued too highly as they have a horse that can count up to 10 even though growth or ROE or both are poor - Well entrenched brands in Premium/Luxury Category. For instance:

- United Spirits Ltd: Manufactures, sells, and distributes a wide portfolio of premium brands | comprehensive brand portfolio | brands that sell more than a million cases each year

- United Breweries Ltd: Products under the flagship brands Kingfisher and Heineken

- Radico Khaitan Ltd: One of the largest and oldest manufacturer of IMFL(Indian Made Foreign Liquor). Company has a wide range of branded portfolio across IMFL categories. Seven millionaire brands.

On the other hand, GSL is still a mass alcohol manufacturer (commodity chemical company - Input cost driven by commodity cycle and Finished good pricing dictated by market forces; Sales and Profitability boosted from ethanol blending) who has just started to learn the ABCs of IMFL trade and will take lot of time and effort to graduate and join the big 3. In FY23, Total Revenue: 2103Cr.

- Manufacturing Revenue: 1357Cr. [~65% of Total Revenue | Capacity will further increase in Steps +120 KLPD to come onstream from Q4FY23 and another 400 KLPD (Odisha+UP) in near future]

- Consumer Revenue:

- IMIL: 709Cr. [~34% of Total Revenue]

- IMFL: 37Cr. [5% of consumer revenue, 1.7% of Total Revenue after 6+ Yrs. of effort| Still Loss Making at EBITDA level | product, brand, marketing, and distribution are evolving]

Pole positioning of big 3 hints at the valuation that GSL can command if the IMFL initiative succeeds. One shall monitor the footprints of the IMFL initiative closely as that will elevate the overall margins and market’s perception (E2E integrated player, stable margins in high double digit).

11 Likes

GLOBUSSPR Acquisition of Shares by Motilal Oswal Mutual Fund: Increased stake from 4.88% to 5.06% in Globusspr.

2 Likes

What are the EBITDA margins of the Manufacturing and Consumer Business individually?

1 Like

Sales is continuously increasing,market share in premium part is again increasing but margins are down because of rice problem…but I think margins have made bottom.This quarter results would be better and stock price will start blasting.

1 Like

Another point to note is that the management is not the most trustworthy when it comes to giving guidance. I have been following the company for a while now and if you go back to concalls of some 2 years ago the margin guidance has reduced from 26% to 19% to now 13-14%. As a matter of fact during the Q1 con call (the ban on purchas from FCI had already been announced by then) the management had said that the impact will only be 2-3% at most but then we got the shocker when results came out and the margins were 7%. So it’s very difficult to believe them. Would.love views of other members in this

6 Likes

Point taken but don’t you feel they should have some idea. Q1 con call happened 1.5 months into Q2 so getting the margins off by such a huge amount is quite a lapse in my opinion. Specially when selling prices are fixed.

1 Like

Is there a way to track broken rice prices in the states where globus operates?

How about coal, should we look at Global coal prices or is there a price index for indian coal

A simple way to buy those stocks are to watch out margin and buy whn margins are at 5 to 10 year low. This gives margin of safety and allows u to play the up cycle

3 Likes

Globus Spirits Good Q3

Sales uptick seen in Prestige and above segment which can improve their margins going ahead, can be a play to the premiumisation theme

Net Profit Up 65% At 44.5 Cr Vs 27 Cr (YoY), surge mainly due to tax refund after shifting to new tax regime

Revenue Up 16% At 687 Cr Vs 592 Cr (YoY)

Great sales growth!! Steady growth in sales for the past many quarters. Capacity utilization back at 90%. I was eager to know what triggered the growth in sales.

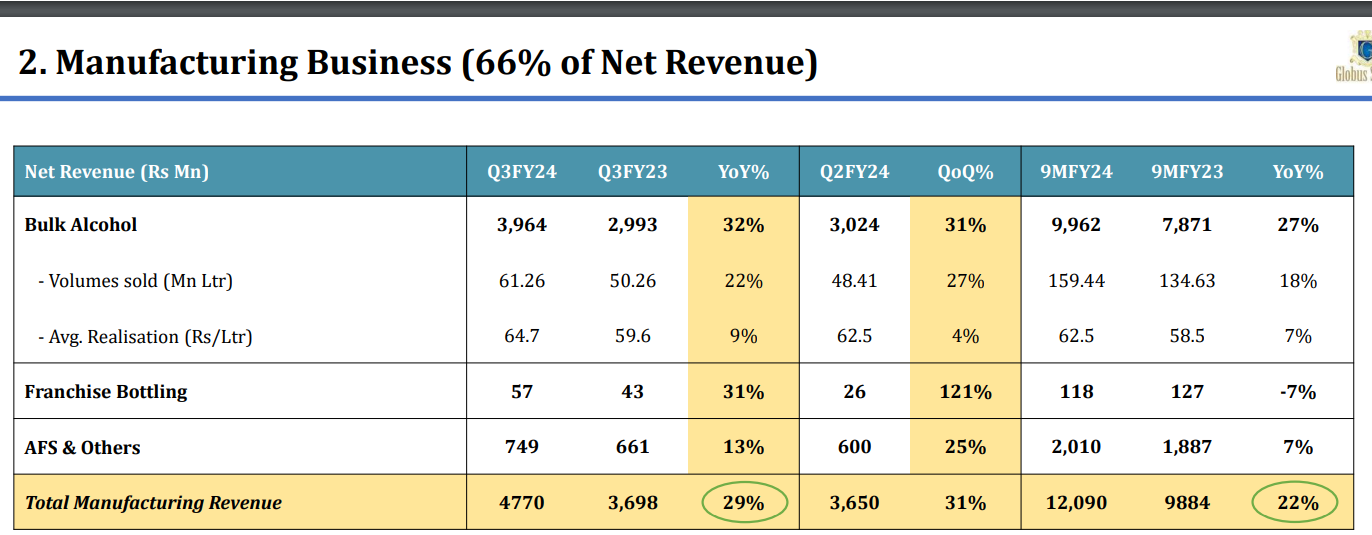

Bulk segment performed with significant growth in bulk alcohol, franchisee bottling and by products on a QoQ basis.

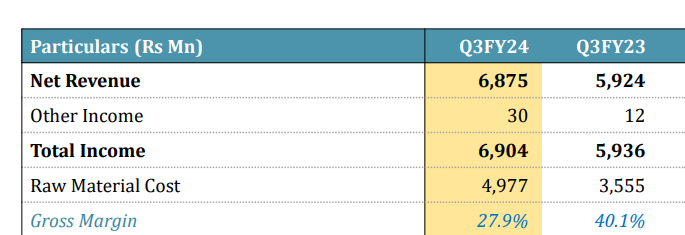

Margin compression was expected as management guided in the last concall. Gross margin dipped further

Consumer sales down down YoY

Prestige still a very small part of the sales. Still at a nascent stage. Still a long way to go.

Have new capacities coming onstream next quarter which can further aid sales growth

Margins could be cyclically at the lowest levels.

3 Likes

Why broken rice is important for alcohol companies:

Understand costing aspects:

Case 1: Revenue / Lt of Bulk alcohol: Rs 64.00

Animal feed & other products: Rs 10-12.00

Total Revenue: Rs 74 -76.00

RM cost: Broken Rice 2.2kg X 26/-: Rs 56-57.00

Gross Margin on Case 1: Rs 18-19.00

In %: ~ 24%

Case 2:

RM cost: Broken Rice 2.2kg X 20/-: Rs 44.00

On the same line, Revenue will also come down by Rs 6.00/- to 58.00/-

Now Total revenue: Rs 68-69.00

Gross Margin on this case: Rs 24-25.00

In %: ~ 35%

Hope you can understand both case scenario. Now come to full costing mechanism

Power Cost: Rs 9-10.00 per ltr

Net Margin: Case 1: Rs 9-10.00 and Case 2: Rs 13-14.00

So Net Net Rs 5-6.00 is impact on EBITDA margin, which is 7-9%.

5 Likes

For the first time, since I’m looking at it, they’ve taken a good decision of not expanding capacity of ethanol. I think this should bring more focus on Consumer biz. Need to watch out as it is not easy to build a consumer brand.

Disc. Not invested at all and not planning to anytime soon.

2 Likes

| Report Date | Mar-21 | Mar-22 | Mar-23 | 9M FY24 | 3 year CAGR % |

|---|---|---|---|---|---|

| Manufacturing revenue | 709.98 | 900.13 | 1356.38 | 1209.00 | 38.22% |

| Consumer Revenue | 514.12 | 679.04 | 746.40 | 615.80 | 20.49% |

| IMIL | 508.12 | 674.34 | 709.00 | 578.70 | 18.12% |

| IMFL | 6 | 4.7 | 37.4 | 37.1 | 149.67% |

| IMIL Volume in Lakhs | 146.30 | 142.3 | 159.44 | 4.39% | |

| IMFL Volume in Lakhs | 0.2 | 2.1 | 2.5 | 253.55% |