GSL is improving IMFL sales in WB,Haryana and Delhi. They are trying to get the shelf space in UP and Jharkhand.They have Governor’s reserve,Mountain Oak and Oakton under Whisky segment.Please provide the review of the products and availability in these states if anyone have access.

Mountain Oak is doing well in UP . Delhi is govt market so its primarily push sales .Products are good but branded business is long runaway and needs investment to gain market shares and needs to compete with deep pocketed multinationals .

5 Likes

Why this stock has become a falling knife?

Could be a couple of things of the below:

- Last two quarters the OPM has halved.

- Compared to peers it’s Gross Profit Margin is not so great.

- Lastly - this could be a red-herring for Q4 results not in line with expectations.

Also looks like hence forth companies with good fundamentals will do well, rest will be brought down to their previous levels before the mad rush started in mid-cap, small-cap…

Discl - not invested.

@strike44 or @Sreekanthreddy9 Do you know how much of the bulk alcohol capacity is used internally for the consumer business?

They have mentioned in Mn Cases for consumer business in PPT.

Company is concentrating on IMFL. They have recruited several experienced people for IMFL segment in the last 3 years. Mountain Oak is getting good attention in WB

No Label is also good, can scale this up just like bira but not sure if management can do that or not.

Whats the source of info?

36a972da-cabf-49c2-8974-9e4772f6b98c.pdf (acesphere.com)

This is the invesment in Bored beveages, they have acquired 51% stake.

No Label Mead | Bored Bev

This is the website of No Label. We can buy these beverages at Gurugram and Delhi.

If OPM is halfed,Mean reversion will take place-It is at the lowest ever margins for now ![]()

2 Likes

Now that’s an optimistic view ![]() . Interestingly their cost of raw materials is going up, when compared to the peers ( Piccadilly Agro ) the cost is almost double … probably need to understand, why they are not able to source the raw material at industry rates as done by it’s peers.

. Interestingly their cost of raw materials is going up, when compared to the peers ( Piccadilly Agro ) the cost is almost double … probably need to understand, why they are not able to source the raw material at industry rates as done by it’s peers.

Note: Above info is purely from numbers reported, I have not done any deep dive into the business model analysis.

How is Piccadily Agro comparable to globus ? Raw material for Piccadily is barley as they produce malts and it’s broken rice /maize/ bajra/ sorghum etc.for globus since they produce Ethanol .

1 Like

Probably you are right, still the question bags the answer - why the material cost is rising for Globus…

Is there a way to track Maize and broken rice commodity prices in Eastern india?

2 Likes

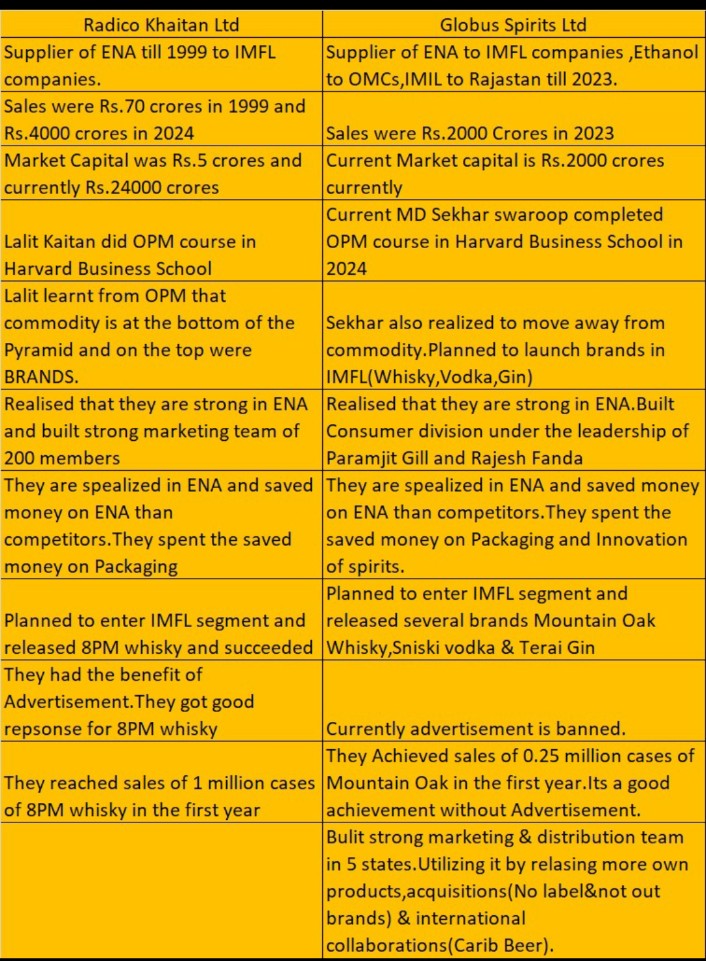

Documented my thoughts on Globus Spirits here: Globus Spirits - Stock Analysis - Google Docs

4 Likes