Shekhar addressed this on the concall - he said there was no demand that they have received from the IT dept and that this was a routine check. Nothing to worry about basis the information available at the moment.

2 Likes

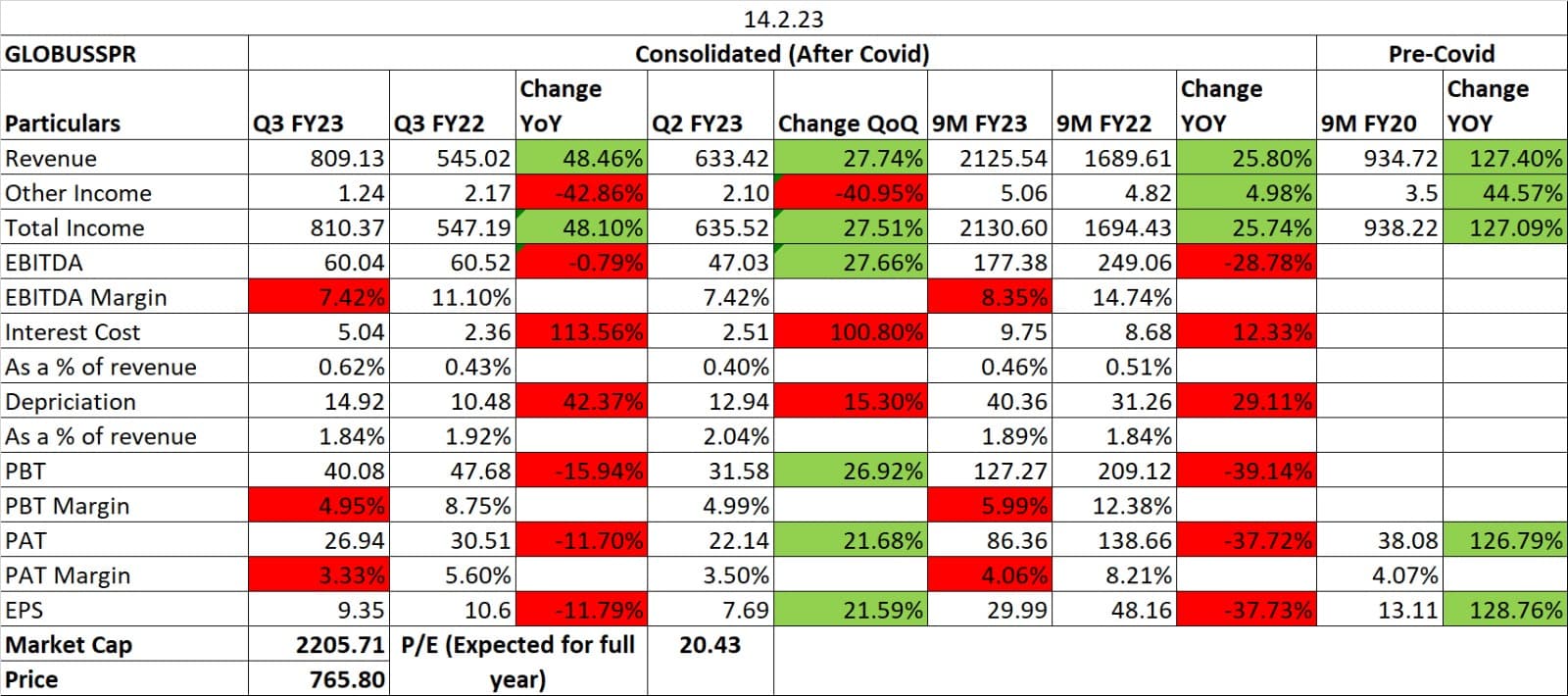

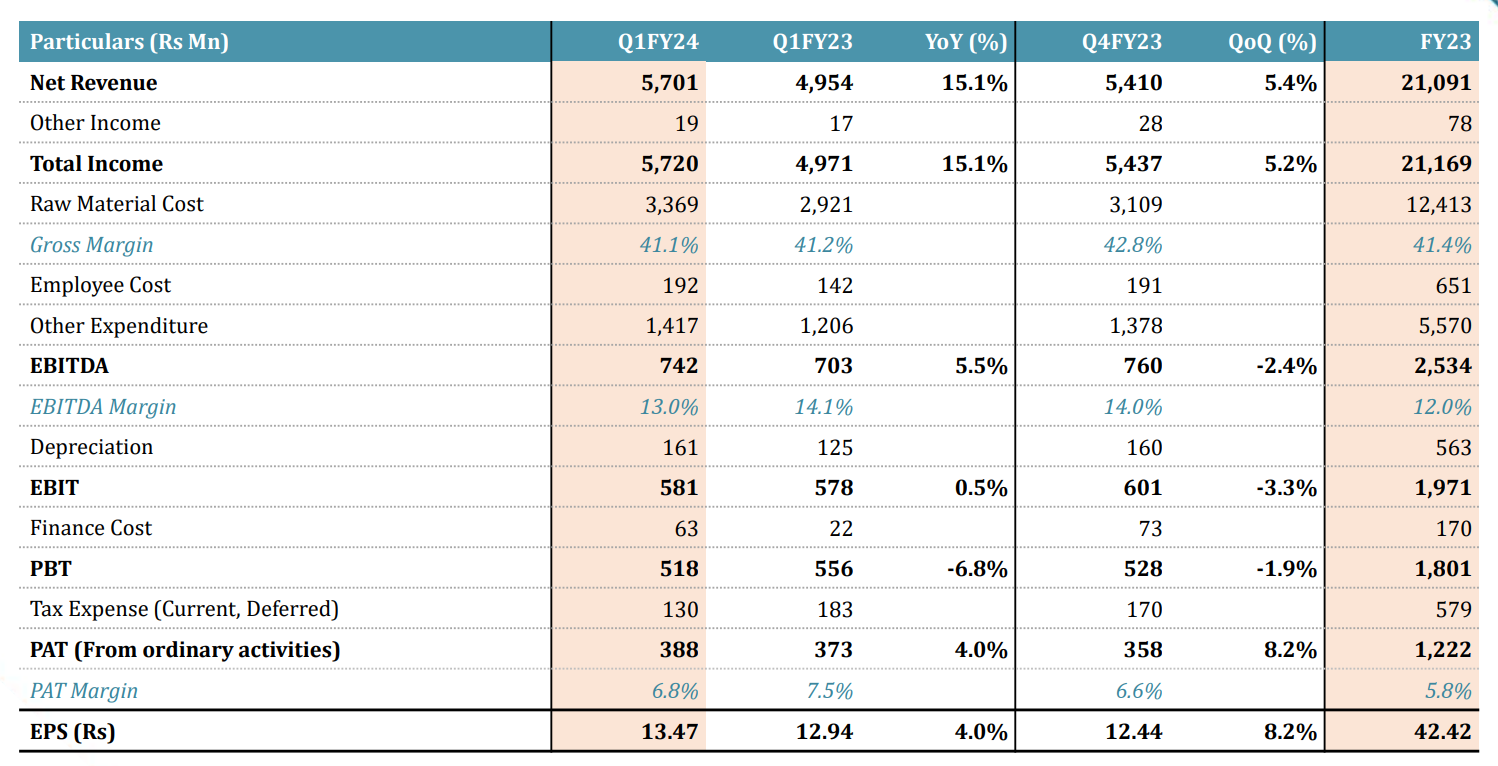

Globus Spirits Q3 FY23 Result Update:

- EBITDA margins excluding IMFL segment are expected to be in 13-15% range. But will remain muted in the short term as grain prices have started to inch upward as well. Recovery in margins will start from Q1FY24.

- Plan to close FY23 with production 2.25 lakh cases.

- Further improvement in realizations is expected with increasing volumes.

- Company is targeting 20% revenue share from IMFL consumer segment.

- They might incure Capex of 35-40 cr in Q4FY23.

2 Likes

One of my key concern is that the consumer business is yet to pick up in West Bengal. WB is a huge market. When company points at a huge access market of 100 million cases in consumer business by 2025 it is yet to make any significant market share or volume gains in West Bengal. They already have their largest capacity there. They mentioned that route to market was making sale of IMIL in particular non feasible. WB state Beverage corporation was in charge of distribution of liquor since 2017. As per newspaper reports Govt is planning to bring in private distributors again. Company seemed positive about the change in RTM in concall but not much enthusiastic.

Company has started incurring significant marketing/ launch costs for prestige and above business. For the 9 months 14 crore was spent on this and expect another 10 crore to be spend in Q4. In the short term this is definitely going to be a drag on the EBITDA margins. Marketing of the brands is particularly difficult due to their limited presence. It needs to be seen how it pans out in the long term.

On the positive side, Rajasthan has announced a price increase for consumer business from Q1 onwards. Rs 26 for value and Rs. 40 for value plus.

As far as raw materials are concerned, Marginal softening in fuel prices and slight increase in broken rice prices.

2 Likes

Very valid point. I myself am concerned about that because West Bengal share has been at 2-2.5% for as far as I can tell without any improvement. Although their IMFL biz is now picking up slowly win other states which seems to be a good sign.

1 Like

Company is not targeting 20% of the rev. From IMFL. They are targeting 20% of consumer biz (which is already dropped from 40% to 34%). So basically they are targetting 7-8% of overall revenue from IMFL part and this is my key concern altogether that even after increasing capacities and increasing access to the new market which they boast very much, their consumer share from overall revenue is declining and no one in the cancall seems to bother about it.

I would very much like to ask about their plans to increase the consumer biz share because then only we’ll know that a brand is actually being built.

The way consumer business is growing in West Bengal is definitely a concern. But you should note that all their plants are running at close to 90 % utilization barring samalkha. As per previous concalls their new plants have a payback period of 2 to 3 years. So when manufacturing alone can give you good ROCE why not expand into new geographies. The share of consumer business has gone down because the revenue from manufacturing segment has increased a lot over the last year. The topline has improved by more than 50 % on a YoY basis. I do agree that greater share of manufacturing means greater cyclicality as we see now. But had they not done the expansion we would have seen a much lower EBITDA.

Secondly, a share of 20 % for IMFL in overall consumer business is something I would love to see. But what needs to be understood is whether this IMFL mean both value plus and prestige segment. Then, how much of these are sales from Rajasthan. Rajasthan is a very established market. They already have a very good share in value plus segment there. In Rajasthan they have everything in place be it marketing, distribution etc. That wont be the same for other states. Its the volume growth of IMFL in other states that I would look for.

Now that the company has started expending cash on launch of prestige liquor, what we need to understand is how difficult it is to build a prestige brand and will company have WB like issues in Jharkand, Orissa or Uttar Pradesh once they expand there?

One thing that I liked about them is they launched a Gin early on. I read somewhere that it was radico’s foray into vodka when no one else was really interested was one of the game changers for them.

6 Likes

Completely agree with you and I happen to admire their operational abilities very much but that makes it a commodity biz so unless and until they improve their consumer biz. Their bottom line would always struggle in one way or another which is very much visible in current quarter. Their topline increased so much but bottomline got depressed. So unless and until their consumer biz commands a bigger share, bottomline will keep on fluctuating and there would be a need to track so many X in the equation. And also you can’t command a higher valuation in a commodity biz. That’s why I’m tracking their them closely and although I’m a a non alcoholic person, request everyone to let know of the quality of the product. Although their instagram looks good for the Terai gin but you never know the ground reality.

I’m invested in this biz assuming it a commodity as of now but hoping that it turns out to be good consumer biz. Till the time something good happens in consumer biz. I’ll value it as commodity play with a little bit less caution because of consumer biz.

8 Likes

Hi, could anyone in the forum please help me as to why the revenues filed by the company differs from the revenue which shows up in screener for Globus spirits?

2 Likes

The company is very cute with their accounting. They include excise duty in the sales to show a higher topline and then show the excise duty as a cost item.

It is like reporting your sales inclusive of GST.

1 Like

All Alco Beverage companies report numbers in a similar manner. Check United Spirits & UBL.

4 Likes

There will be growth in the EPS in the upcoming quarters because of following reasons-

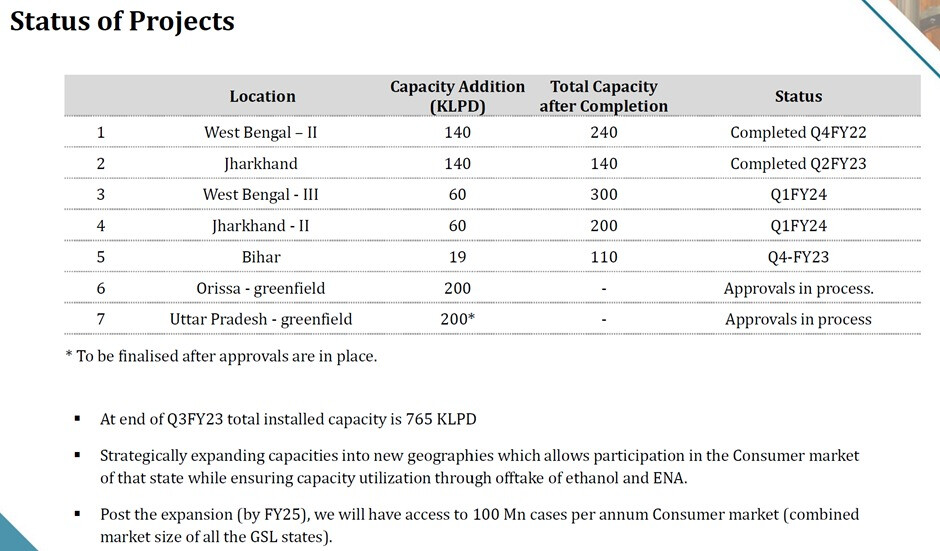

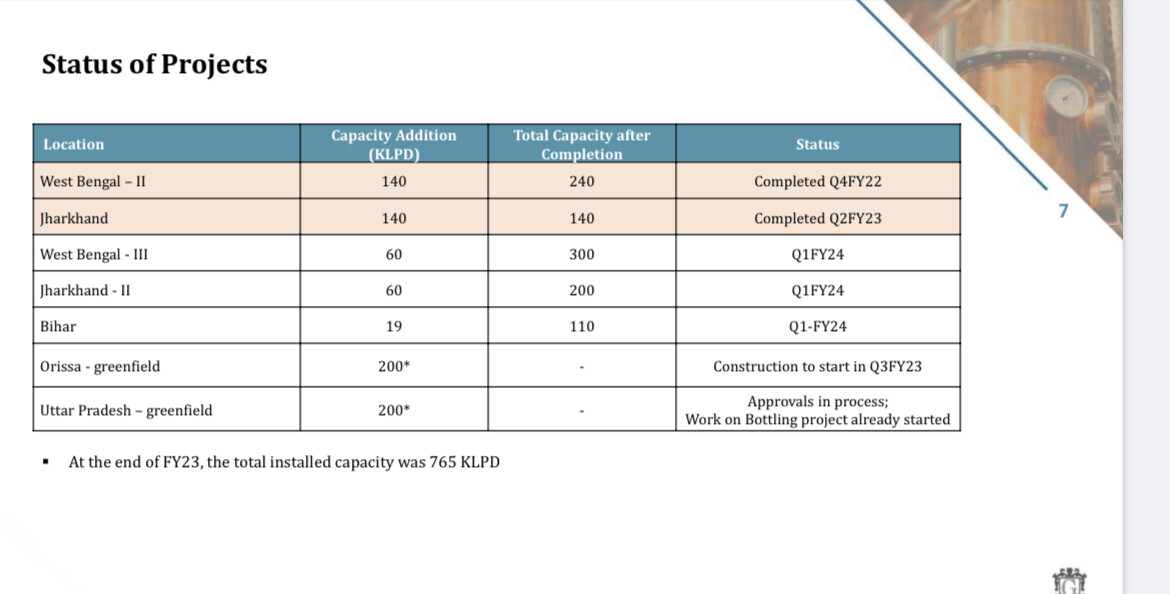

1-Capacity Expansion is Recently Completed for West Bengal Unit2 and is In-Progress for WB Unit3, Jharkhand Unit2, Bihar Plant, Greenfield Capex for UP is already Started.

We will see the major Increase in Topline +Bottomline from Q2FY2024 onwards

2-Secured another price hike of Rs 40 per case for Value Plus and Rs 20 per case for Value segment in Rajasthan, effective 1st Apr’23. This along with ongoing momentum in Premium+ Brands will continue to support consumer segment realisations

3-Full year of operations for 140 KLPD Jharkhand facility and incremental capacity of 60 KLPD each at West Bengal III and Jharkhand II, is likely to benefit Manufacturing Business in FY24

4- Launched Mountain Oak during Q4Fy23 Whisky In WestBengal

5-Snoski Vodka Launched during April.23 in Uttar Pradesh

6-Launch of Products in Punjab During June,23 and Haryana in Q3FY23

7-Addition of New Plant of Bottling Business for the UP in Lakhimpur Khiri in Q3,FY24

8-Once IMFL starts contributing to Profit the margins are high in this segment (15%)

9-Premium and Non-Premium Products both will be launched in UP around Q4,Fy24

10- Capacities are fungible So Globus is getting benifits of the same

Disclaimer- Invested, can be biased, Source- Investor Presentation- Q4FY22

Always open for your opinion ![]()

11 Likes

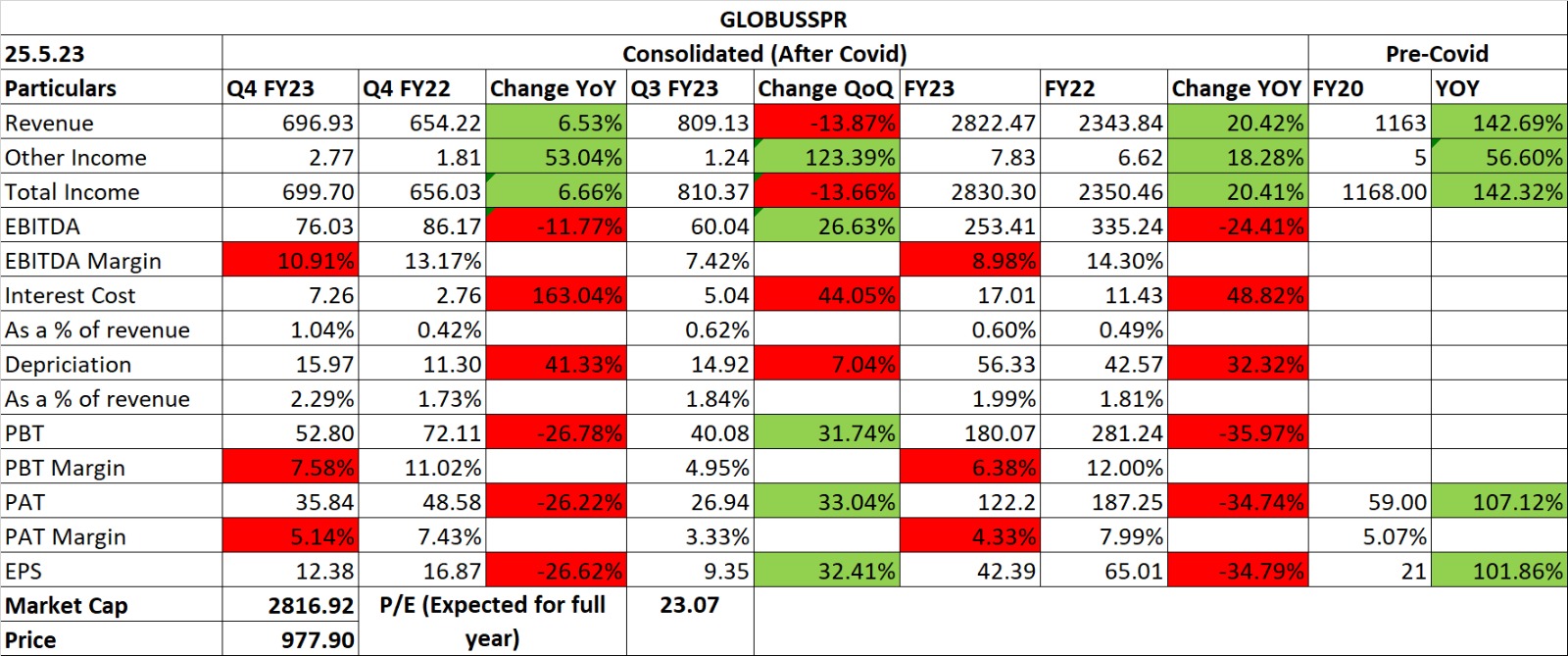

- Utilization levels at 90% in FY23 for ENA production.

- Power & Fuel cost reduced by 27% QOQ.

- Consistent focus on reducing debt. Average cost of debt is 4%.

- ROE/ROCE of 14%/17% respectively.

- Capex: The company has planned additional capacity expansion in West Bengal as well as Jharkhand and is expected to be commissioned by the end of Q1 FY24. These additions would take the total installed capacity to 905 KLPD. Another capacity in Orissa is targeted to start construction by Q3 FY24 and would add 200 KLPD. The capex for this capacity is expected to be ~₹160 crore, out of which ₹120 crore will be funded by debt and the balance through internal accruals. The borrowing cost on the debt would be ~4% as it would receive interest rate subsidies from banks. The project in Uttar Pradesh has begun construction at Lakhimpur Kheri and anticipates to start rolling out its brands by the end of Q3 FY24.

- Guidance: Share of premium segment in in revenue is targeted towards 20%. Planning to enter Punjab, UP & Jharkhand Markets with Premium segment products. A premium rum is expected to launch by Q2 FY24 and the management envisages to enter into the single malt segment by the end of FY24. It also plans to expand the variants of its flagship product of Craft gin. EBITDA margin of 15% targeted excluding IMFL segment for the next 1-2 quarters. Manufacturing Capacity Utilization in Haryana to be 95% in FY24. The company is not expected to hit 1 million cases in the IMFL segment this fiscal year, but triple-digit growth is expected.

10 Likes

Looks like their capex is completely going into bulk manufacturing and they are not able to grow their IMFL segment even with a smaller base, only 5% growth is just not enough, unless and until they can’t ramp up the pace, I don’t think they deserve the valuation they have.

Disc: Exited today. Will see, what mngmt. will say in the concall.

1 Like

Anybody who has attended the concall?

What is the guidance of the management for future?

takeaways from concall esp. on FCI stoppage …

- margin impact foreseen 1-2% on EBIDTA due to open market sourcing v/s FCI rice

- sourcing from open market to continue until Nov/Dec until new Rice is produced

- Q2 / Q3 will have lower margin compared to Q1

- top line impact approx 40crs in Q2, but can be covered by increased pricing on animal feed / consumer business

1 Like

My notes of August 16, 2023 concall

Ethanol and ENA Business Dynamics

- Variables in Play: The ethanol blending scenario involves several variables: raw material (corn, rice), yield conversion, and offtake prices by OMCs.

- Fungibility Advantage: Flexibility exists to switch between ENA and ethanol production, comprising over 50% of installed capacity.

- FCI Rice Disruption: FCI halted rice supplies for ethanol production, prompting industry reliance on alternative materials like maize and broken rice.

- Price Adjustments: Industry requested price revisions due to unfavorable ethanol pricing based on raw material costs. Prices for maize and broken rice ethanol increased by INR 6 and nearly INR 5, respectively.

- Margin Impacts: Margins on ethanol differ across states and materials, sometimes lower than ENA. Reorganization of sales mix between maize ethanol, broken rice ethanol, and ENA is needed.

- Plant Operations: Jharkhand operates on ENA due to high grain rates, while West Bengal combines broken rice and maize for production.

- Q2 Impact: Closures in West Bengal and Jharkhand temporarily affect revenue and margin in Q2.

- Q3 Expectations: Q3 will see new crop availability, easing supply constraints and supporting margins.

Consumer Business Strategy and IMIL Penetration: State Approach and Expansion

- State-Specific Approach: IMIL presence varies across states, with some having IMFL-like segments, while others categorize it as IMIL or country liquor.

- Integrated Model: Globus pursues a comprehensive approach, including ENA production, bottling, and distribution within states featuring economy segments. This strategy ensures stability and sustainable margins compared to buying ENA and just bottling.

- Current Operational Scope: The strategy is actively implemented in Rajasthan, Haryana, and West Bengal. Future expansion plans encompass Jharkhand and Uttar Pradesh.

- Targeted Expansion: No immediate plans for Value and Value Plus expansion beyond these states, but future opportunities will be considered.

- Market Maturity: Rajasthan and Delhi stand as mature markets with well-established distribution networks. Haryana and West Bengal are identified as growth-oriented markets.

- Odisha Plant: While Globus has a plant in Odisha, there are no plans for entering the Value and Value Plus consumer market in the state.

Gross Margin Impact and Raw Material Costs

- Gross Margin Computation: Gross margin calculation factors in costs of raw material consumed and packing material consumed.

- Raw Material Costs: A significant factor in the decline of gross margins is the rise in costs of raw materials consumed.

- Raw Material Impact: While FCI supplied rice remained stable, the prices of other purchased broken rice increased in Q1 compared to Q4.

IMIL Volume Loss and Haryana Strategy

- Volume Situation: Year-on-year, IMIL volumes were down due to a decline in Haryana.

- Reason for Decline: Haryana experienced volume loss due to margin pressures. An investment pullback strategy was adopted to prioritize sustainable margins over immediate volume growth.

- Haryana Volume Impact: A significant portion of the volume loss (0.4 million cases) was attributed to Haryana.

- Reinvestment Strategy: The company has initiated reinvestment in Haryana due to a more favorable environment. Gradual growth is expected as the strategy unfolds.

- Future Outlook: The reinvestment strategy is anticipated to yield results in the upcoming quarters, with meaningful numbers expected next year.

RML vs. IMIL Trends in Rajasthan

- Past Policy Change: A policy change affected the medium segment or Value Plus segment, resulting in de-growth followed by anticipated growth.

- Current Observation: In Q1 and Q2, growth is observed in Rajasthan within this segment after a decline last year.

Maize and Broken Rice Impact on Margins

- Volatility and Flexibility: Shifting to maize and broken rice introduces more volatility compared to stable FCI rice prices. The flexibility to mix raw materials, however, helps mitigate some of the volatility.

- Margin Evolution: Q2 margins will be impacted due to shocks and the transition to maize and broken rice. While maize and broken rice aren’t as profitable as FCI rice, Q3 and Q4 are expected to see margins move closer to Q4-Q1 levels as new rice and maize crops become available.

- Annual Margin Expectation: Margin projection for the entire year is challenging for the next 3 to 4 months (August to November), with an estimated 1% to 2% drop. However, from November onwards, margins are anticipated to approach Q4-Q1 levels, but exact numbers are difficult to specify for the short term.

Consumer Business Performance and Growth Expectations

- Y-o-Y Volume Performance: Y-o-Y volumes for IMFL have fallen short of expectations in Q1, particularly for prestige and above IMFL, which grew by 5%.

- Pipeline Effect: It’s important to note the “pipeline effect.” When new brands were introduced last year, there was an initial surge in sales due to inventory buildup before the official launch. This phenomenon affected year-on-year comparisons. The current year reflects the replenishment phase following the initial introduction.

- Supply Challenges: Some supply issues at the quarter’s beginning temporarily impacted delivery but were promptly resolved.

- Future Trajectory: The company remains confident in its growth trajectory. Challenges are being overcome, and as the year progresses, a more robust performance is anticipated.

- Full-Year Expectation: The aspiration for the full year is to double IMFL business, reflecting the evolving nature of the business, expansion into new geographies, and portfolio growth.

Value and Value Plus Growth Expectations

- Growth Outlook: Anticipate slightly higher growth, around 5% to 7%, for Value and Value Plus segments this year.

- Quarterly Variation: Expect stronger growth in these segments on a quarter-on-quarter basis. Last year’s investment slowdown in Haryana impacted year-on-year growth until Q2, but growth is expected to rebound from Q3 onwards.

De-commoditizing the Business through Consumer Growth

- Key Focus: The strategy to de-commoditize the business revolves around strengthening the consumer-facing segments, which have higher margin potential.

- Consumer Business Growth: The goal is to gradually increase the revenue share from the consumer business, moving from the current position to around 50% initially.

- Long-Term Target: The aim is to achieve a healthy balance between the consumer and manufacturing segments, potentially reaching around 60% to 65% revenue share for the consumer business.

- Timeline Uncertainty: The exact timeline for achieving these targets is uncertain due to various factors, including the growth trajectory of the manufacturing business. It’s a medium to long-term objective that’s being closely monitored.

Prestige and Above IMFL Strategy

- Geographical Selection: The selection of geographical areas for the prestige and above IMFL segment is based on factors like favorable margins, route-to-market viability, and the potential to establish a competitive presence.

- Strategic Focus: The goal is to leverage the initial small base for higher growth rates compared to the larger IMIL business. The prestige and above IMFL segment offers higher margins and appeals to an evolving consumer base.

- Gradual Expansion: The company’s approach involves expanding gradually from state to state, building route-to-market capabilities and key account activities along the way.

- Growth Trajectory: The aspiration is to achieve a substantial increase in market share, with a medium-term target of reaching around 20% from current 4% for the prestige and above IMFL segment. This growth is driven by the evolving consumer preferences and the strategic expansion into select states.

16 Likes

on Sept 6

5 Likes

I brought Globus Spirits at Rs 840, is it still good to hold for long term(5 years).I felt company is fundamentally strong. Please suggest.

2 Likes

the company seems good and well diversified avenues, they are also trying to pivot to IMFL brands. The key concern is dependence on FCI Rice (and open market in absence of that). As soon as Rice ban occured, it destabilized their margins. I was holding it, sold upon FCI Rice ban news, as I reckon it will continue for until next summer.

3 Likes