Some relevant data on the matter of creating a strong consumer brand.

(Source Economic Times, 11 June 2022)

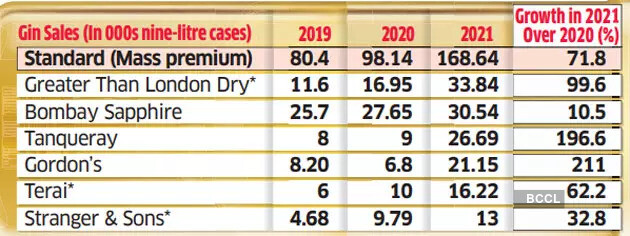

“Terai”, GSL’s niche brand features in this list of fastest growing Gin brands in India. As clear from the data, though still on a very small base, the volumes are growing phenomenally well. It certainly points that the company is doing the right things on the brand creation front.

Gin Industry is growing globally and in India is also showing lots of traction . Diageo has invested in Hapusa/Greater than by buying 20% stake .

All MNC are facing supplies issues with stocks are not available or in short supplies so Indian companies are doing well and lot of growth is still to come with Gin reviving as category vis-a-vis Vodka. Globus should concentrate on this category and expand its portfolio here rather than wasting energies on brown spirits where competition is fierce higher and category is dominated by MNC .

Next year is looking all the more strong.The raw material inflation (coal specifically) hopefully has peaked and the small rate hikes should help with the depressed margins going forward.

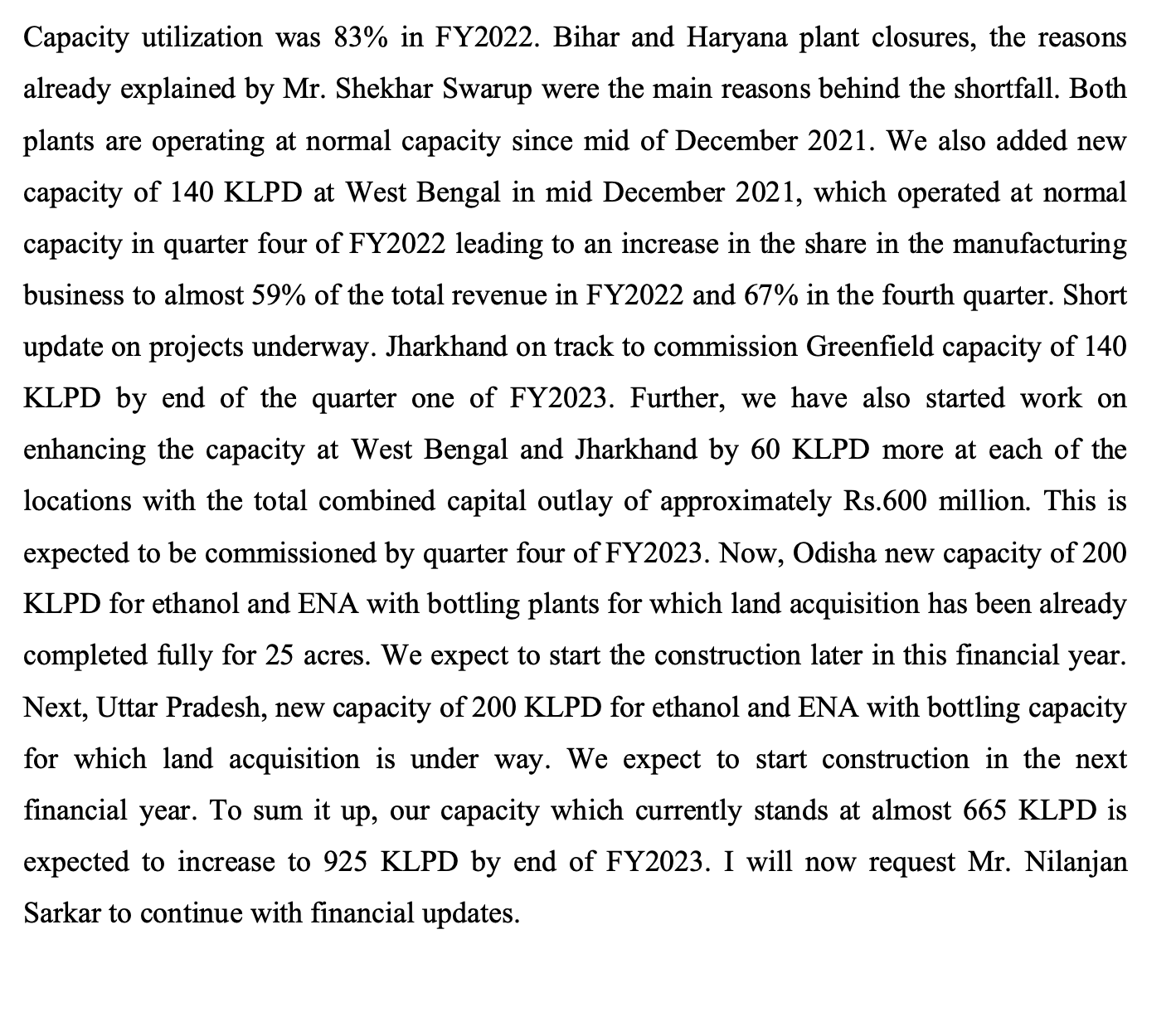

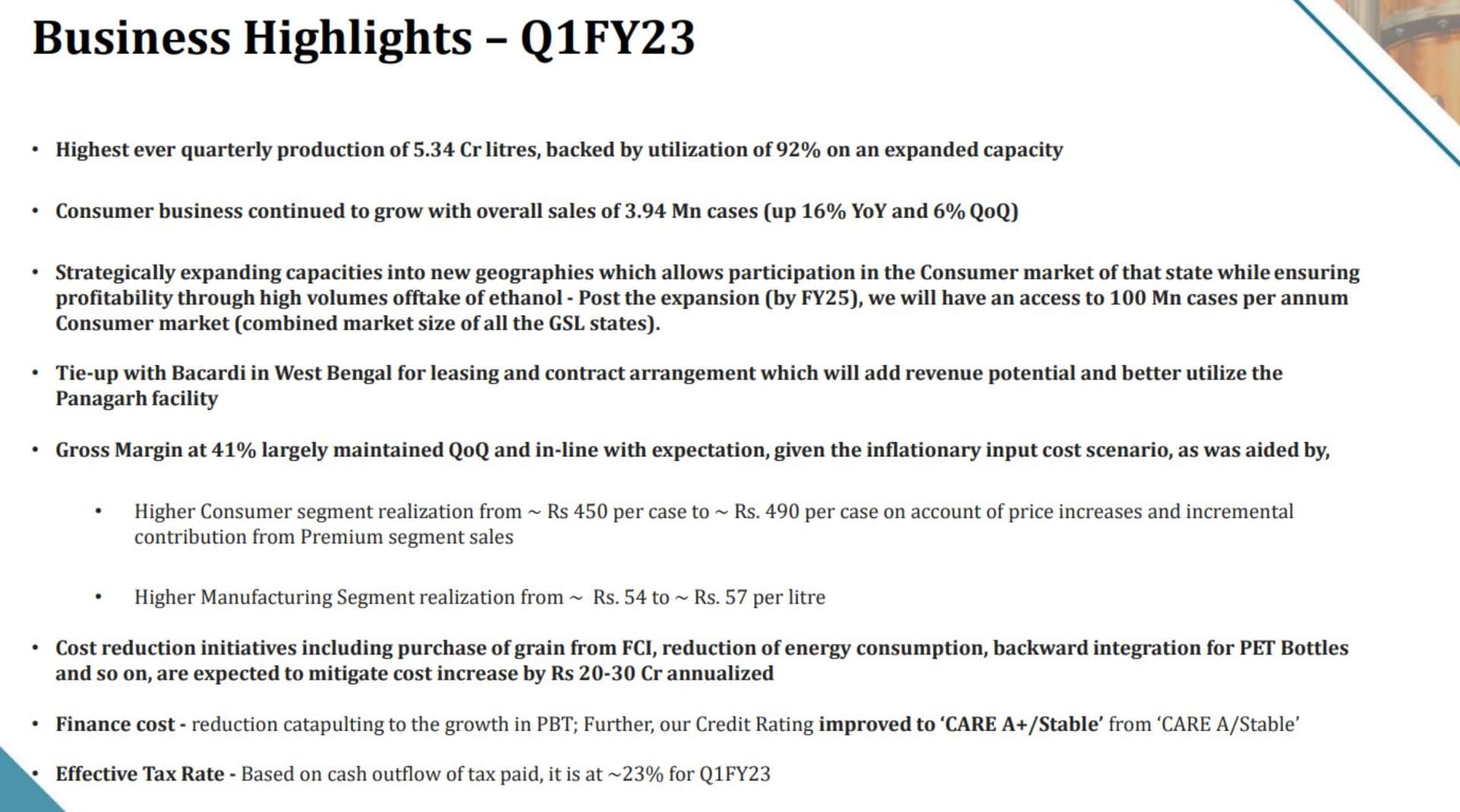

After the new capex the company’s capacity will increase by 33% approx at the end of FY23.

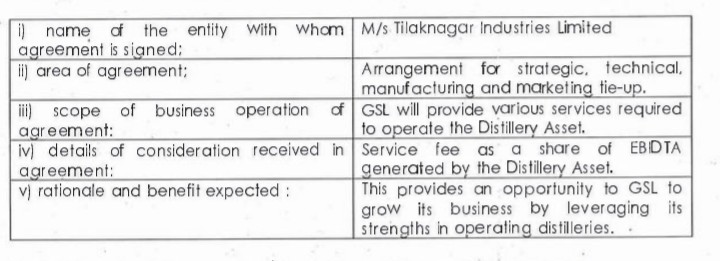

Strategic,technical,manufacturing and marketing tie up with Tilaknagar industries for operating 140KLPD plant in Maharashtra on a EBIDTA sharing basis. No details on the share percentage though…

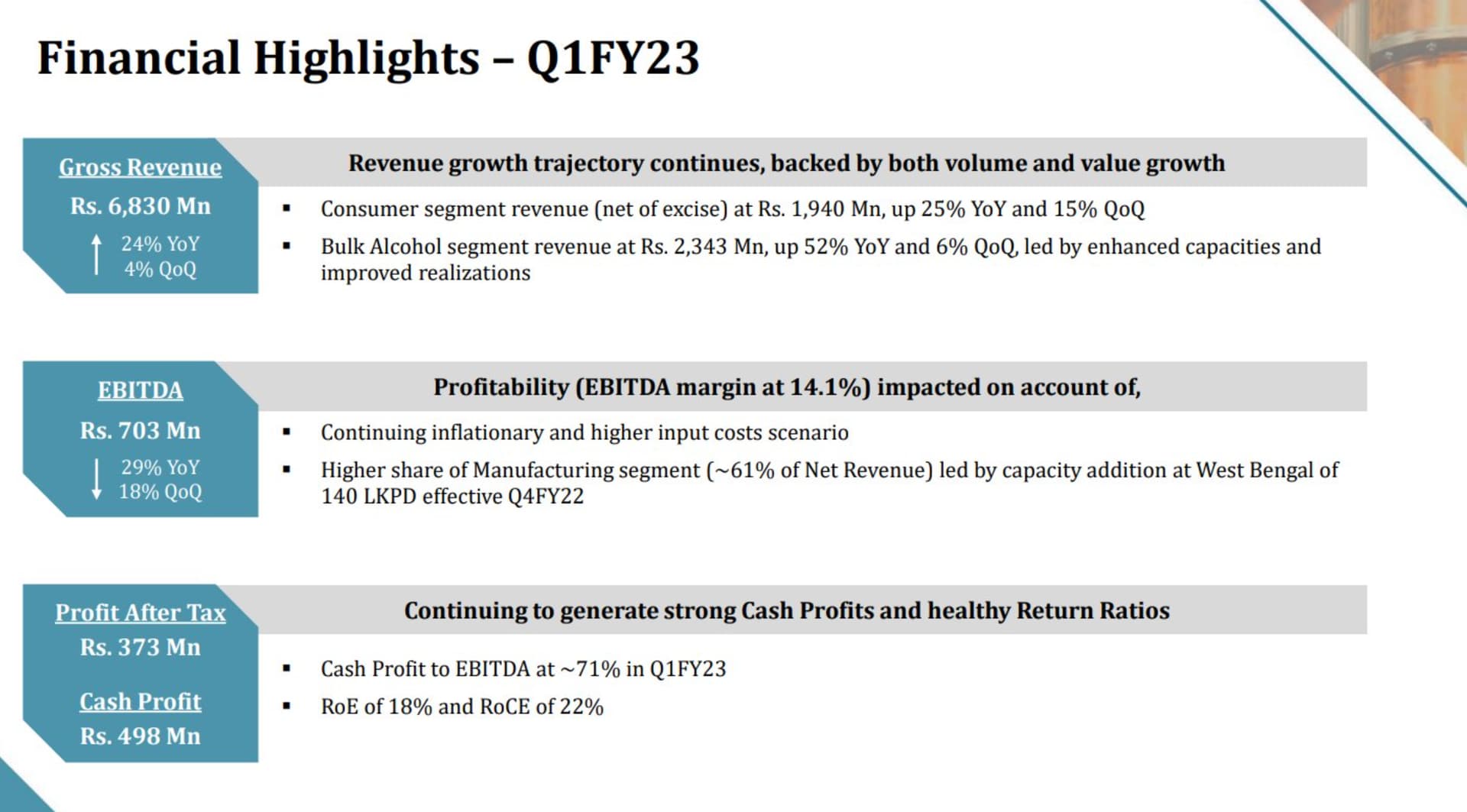

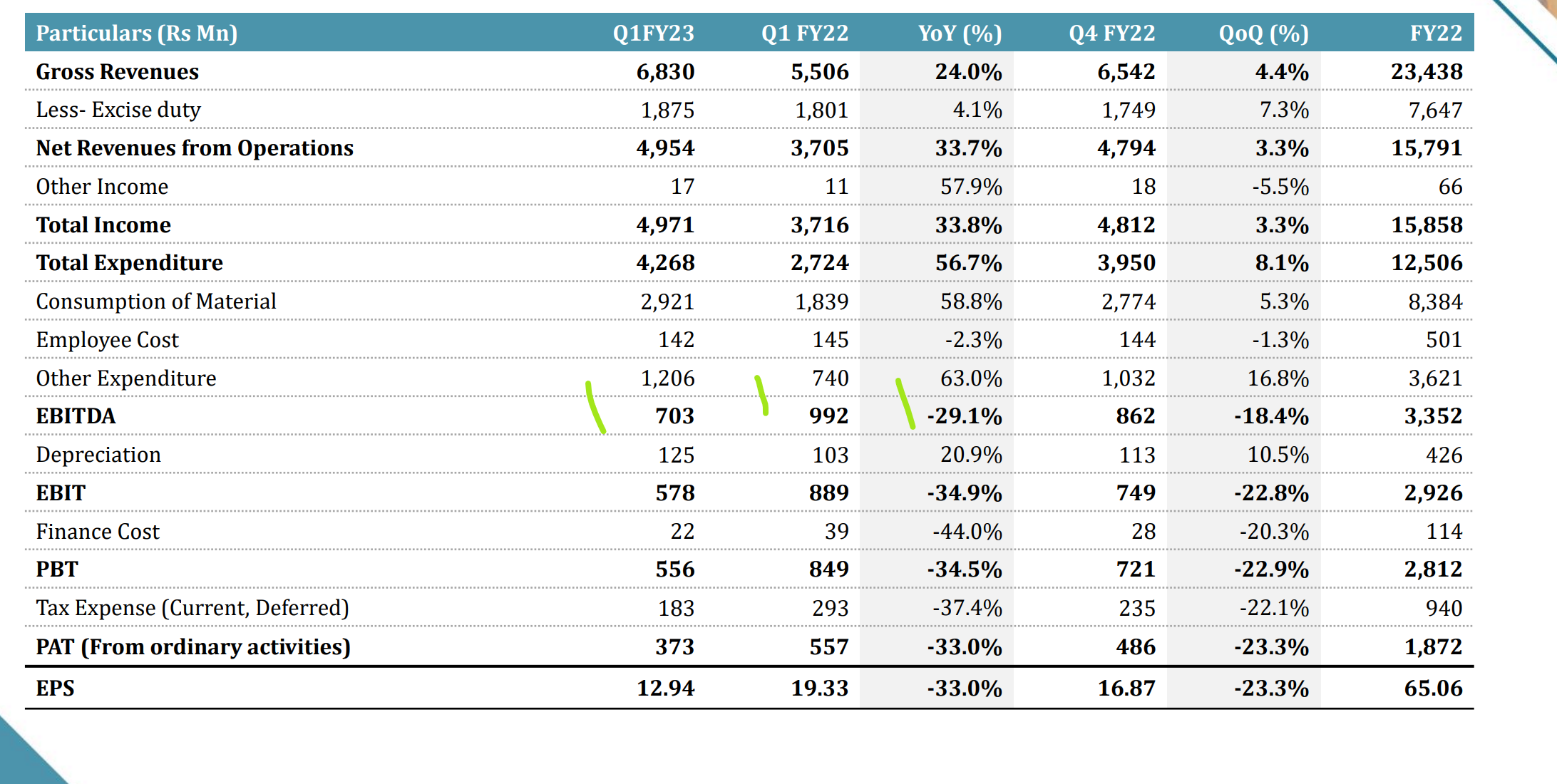

In my opinion results are very bad. They have not been able to maintain margins for last 3 quarters and each wuarter has been worse than the previous one. Current margins of 14% is extremely bad compared to the margins of 24% which the management said they will be able to maintain easily. This concall Mr swarupdropped the guidance of 24% completely and said they will try to target 18-20% in normal course if business and that too only after 2 quarters. Very difficult to trust the management this way.

Basically, Globus has no control over realizations in both the bulkena/ethanol nor consumer segment. Their input costs including fuel, grains and plastics are also commodity prices beyond their control. Globus is basically a commodity chemical company. How can mgmt “guide” on margins? They can’t… Margins will be exhibiting cyclical behavior with not much predictability. If you see OPM over the years, 14 is about average. 24 is clearly way above the mean and is in no way sustainable. Thus a commodity “chemical” manufacturer like Globus will be a cyclical stock

and will exhibit huge volatility.

The best feature of Globus, however, is its growth rate. There is no negative there! They are keeping on growing… State after state… growth runway is large given ethanol blending… Value, value plus and desi premium are a play on rising rural income… Each new state makes it easier for them to add the next state.

As the growth story is intact, I actually added up. Will add up some more if further drops after Q2 provided growth continues. Note that for a bulk chemical entity, the bigger it becomes the better it becomes and will ride over OPM cyclicality which will never truly go away.

@Ravi_Hegde I agree the narrative of Globus being a commodity chemical company

Having said that, this year is quite unprecedented scenario. Worldwide, we see the inflation across the Globe which it not see in past 50-60 years. Specific to Globus’s raw material, Coal prices have spiked almost three time. To my knowledge, such as steep price increase have not happened in past 10-20 yrs. Cement manufacturers(even the cheapest producers like Sanghi) did also suffer in past 5-6 months. We can hope for this unusual times will normalize, and the investments made in growth yields results. But as you said, we are at the mercy of commodity (fuel, grains, packaging) prices cooling. From conference call, one aspect I personally must appreciate that they are looking for cheaper alternatives of sourcing the raw material by way of sourcing it via coal linkages with Coal India’s subsidiaries. The market is not in company’s control but the intent indicates the management’s willingness and capability to work around.

On the flip side, some of the management members appeared to be overboard on the call. One of the member providing 100% assurance on Govt’s behalf to increase Ethanol pricing given the cost pressures.

During the conference call, management stated that the margins for Q2 will be even worse than Q1, They expect margins to get better from Q3. (Subject to terms and condition i.e. commodity prices )

In terms of growth however, growth story is indeed intact as @Ravi_Hegde has mentioned!

The key concern for the past few months have been constantly increasing raw material cost. The company has been exhibiting cyclical characterstics with operating margins falling from as high as 26 % in June’21 to 14 % in June’22. Many has raised concerns about company’s ability to maintain margins at what they guided for in previous quarters. But as @manoopatil has mentioned we are seeing a rare inflationary trend that I don’t think the management could have foreseen it.

As per Q1 concall fuel cost are up around 30 % QoQ, packing cost by 12 % and grain cost by 6 %.

As per BCL industries concall broken rices prices were around 18-19 which has moved further to Rs.21-22 in Q2.

As there are no price revision up for any items in Q2 other than for ENA which is market to market, the Q2 margins will be worser than Q1 as the company indicated in the concall. About 45 % of raw material requirement is met from FCI purchases at fixed price of Rs.20 per kg where there is a higher realisation on ethanol.( Rs.3 incremental benefit as per concall).

India has banned export of broken rice as of September 9.This may provide some respite to the increasing broken rice prices which may stabilise by Q3.

The fuel costs and packing prices are still unpredictable. Company has started production at its Jharkhand Unit which is expected to further increase revenue.

Any improvement in margin can be expected only in Q3 when the ethanol prices will come up for revision, with the industry in very low ROCE the govt may be forced to increase prices so that ethanol blending program goes as planned. Any value segment price revision will come only after 31 March23.

With manufacturing now contributing to 61 % of revenue, revision of ethanol prices will be significant and Q4 may provide us with more idea of how margins will play out. Also another thing to watch will be how Bihar facility will function during monsoon. The facility was flooded in last 2 years when the facility was closed for some days. They mentioned that they have done some flood control activity at Bihar.

Company has sold 3.94 mn cases vs 3.73 cases QoQ in value segment

The company has done remarkably well in increasing sales from 382 crores in sept 21 ( considered sept as there was an abnormal decrease in Dec 21 due to closure of Bihar and Haryana facility)to 495 crores in March 22 which is further expected to go up in current quarter with Jharkand facility commencing operations

The rice prices are not down much.The input prices of coal in particular is coming down but gradually ,the management had said Q2 will see the worst impact of these price hikes. That’s the reason why the stock prices are down.The capacity has come online.From november the prices of ethanol will increased by government too.The coming quarters will be much better if the input prices keep coming down. Market is taking into account the margin pressure and going down accordingly .

Any reaction in the results for globus? I felt the results were much worse than expected. Even after new capacity came in stream I don’t understand how sales declined QoQ.

The value plus contraction in Haryana and Rajasthan is what’s most disappointing. Missed the concall, will have to wait for the transcript to understand if it is a structural issue. In bulk I’m pretty sure the worst of margin pressures is behind us.

The manufacturing side panned out as discussed in Q1. It does appear possibly bottoming out?

But, there is always the geopolitical risk which may impact power expenses. This margin contraction is seen in other ENA companies too.

Negative surprise in consumer is not clear. Huge downswing of 35% in value plus rajasthan is not anticipated. Looking for clarity in this regard from concall transcripts. Perhaps, others can enlighten me.

Very concerned about this.

Thanks for the link. The article does not mention upward revisions for grain based. But, neither does it mention that grain based has not been revise - perhaps omission on part of journalist? Fuel costs are inflated for all ENA manufacturers, so it would be unfair if not re ised. Perhaps, some knowledgeable person on forum could illuminate?

DISCLOSURE - Invested and underwater. I had hoped to average down after Q2. But decided to wait a bit longer, Perhaps after Q3 concall.

I am a bit of a DUNCE actually, so no revo, DO your DD.

Has anyone tried their product in Premium Segment? Would like to get some reviews on that part as well because if the quality is good (which I hope it is), then that is one tick for their Premium segment to be picked up.