Business prospect wise nothing has changed for worse since I first bought 10 months ago .I also bought some more today .Please check yesterdays investor presentation(available in screener easily) for the news from horses mouth . This quarters results were along the expected lines but Mr. Market was very depressive today .

2 Likes

While I think you are right and results were kind of expected I feel the main issue is the management comments. In Q3 concall which was held in February the management said that the 17% EBITDA was one off due to plant shutdowns, having to procure raw materials from market, increase in ethanol proce which had yet to kick in and more. The management on asking multiple times mentioned that margins of Q4 last year was what they were aiming at in this year also. Therefore seeing margins come in at 18% is a disappointment and atleast for me reduces my trust on the management.

1 Like

Fair enough but power cost and foodgrains price increase could not have been forecasted back in Feb. While its true that the management is more optimistic than realistic sometimes but from a long term perspective they are doing what they have said and I do not see any deliberate misleading.Also considering Radico has even lower OPM%,double the PE and the expansions of globus ,in normal scenario its cheap.

Disclosure: largest portfolio position

2 Likes

There is a genuine reason for no PE expansion similar to radico or even tilak nagar industries.

They both deal in well established consumer liquer brands. Thats why they have similar PE expansion.The consumer side of globus is still small with no major brands in place as of yet. Expecting PE expansion similar to radico is not right in the current scenario. I think the market is treating globus as a commodity liquer, bottling and ethanol play for now. In the concall of united breweries they have mentioned that future price of their inputs will only increase for the coming 6 months or so .

Considering those factors market is pricing in a few quarters of major commodity price headwinds .

Company is doing all the right things. If they are able to gain ground in making a sticky brand , PE will expand.

7 Likes

I am not expecting Radico PE for globus right now .But the idea is that they will get there with time .ENA prices are revised once a year in December and thats fixed .So it does not affect Globus’s selling price for the same till Dec atleast . What United spirits is talking about is the imported ENA price that is not under gov regulation afaik we dont produce enough in our country .Kerala based companies are cutting down production for this reason.

3 Likes

yes that would be right expectation, I believe ![]()

1 Like

Ethanol Prices are revised once a year on 1st December. As far ENA is concerned i think it is more a factor of demand & supply.

Liquor and ethanol both have regulatory risk, how do you price that?

The risks are same for all the players in the industry .As of now ,until the time ENA prices are determined by the gov, the risk of making loss by selling ENA is very small.Thats because, I think it was only in late 2018 that ADD was applied on imported ENA to make the domestic industry viable. Reversion of this is the single biggest risk .

However,with the much higher demand of Ethanol brought about by the petrol mixing requirement ensures that if ENA becomes unviable ,company can simply sell ethanol as all the newer factories are fungible .

4 Likes

You monitor what the government is doing with their policy in the field .For now the policy towards both ethanol and liquor are favorable .The govt has realized that having a healthy push to liquor in the retail helps with their tax collection immensely . This is actually a trend which is very hard to reverse. Specially in the tier 1 metropolis

4 Likes

Agreed even in Davos. I heard Piyush Goyal Ji mentioning about EBP. But concern is that policy change is sudden and hardly gives time to react.

I have a position at lower levels.

Just worried about adverse govt action.

I’m trying to understand how to hedge against this risk.

1 Like

In your opinion

Does the current management has the bandwidth to expand into premium alcohol segment

Next FY onwards company will have substantial cash flow available with them(assuming no more capex in ethanol segment)

It does have the bandwidth but building a brand does not happen over a year in my opinion.Building a brand is a 3 to 5 year project mostly and right now the management is focused on expanding and gaining market share in various parts of the country over brand building and premiumization as a goal .To me this is a capex play a company growing topline at 20-25% at ROCE of 30% plus in a consumer segment .Given the management has a track record of successfully achieving these targets previously and having 40% of their revenue from consumer alcohol I believe the company should have a PE of 20 at least . Let me know if this analysis seems sound. Disclaimer invested .

6 Likes

They have spelled out their intent to do so .But being based in a WB village,I have no direct or indirect exposure to their products myself and hence I have no opinion on their chances of success.

As I see it ,the exapansion and FCF is good enough to justify holding on to it and wait for the consumer section to get better with time .

5 Likes

The value and value plus segment is mostly decent in rajasthan , but still not like a household name I believe. There is a difference in having a somewhat decent local brand and market share and having a pan india known brand and market share . So it would take them around 3-5 years to properly be available in major parts of india and simultaneously premiumize their products and strengthen their brand .It is a Promising candidate for sure thats why invested but not there yet so i do believe unreasonable to demand 40 or 50 PE with current business level .I believe a fast grower with good ROCE proven management track record , pro government policy for the coming years .If inflation keeps biting into their net profits these ratios may worsen and that is why the stock fell . Market factoring in uncertain margin pressures(which the management had no guidance on concall, because they had no way to predict coal prices) will continue and if you take that their OPM is below 20% for this FY 23 their ratios will start to look less attractive .Though i believe this is a very pessimistic stance the market is taking hopefully coal prices should cool off as the production is ramped up, india begin a major producer of coal . Government has already started to take measures to cool these input prices .

5 Likes

Getting a foothold in consumer side of liquor business is a tough call as consumer liquor market is highly fragmented and liquor MNC i.e Pernod & Diageo are having a dominating presence . Few smaller companies have gained some shares in selective states and regions due to owning retail and some states e.g Oasis distilleries in Punjab with brand like All seasons. Rock & Storm brands like Barrent , Dennis etc . Some companies are surviving as they can push their brands in government controlled markets i.e TN , Telangana , Kerala.

Liquor MNC has deep pockets and they get excise policies revised too favor them & Markets are shifting towards imported premium brands .

Best way forward for GSL is increase their presence in value segment where consumers can upgrade from country liquor and in niche categories like Gin Terai as brand is getting good traction .GSL needs to play on its strength of being one of the best quality ENA producers.

Consumer business has a long gestation and investments .

7 Likes

I am also based out of a WB village. I have seen their value product getting sold in Liquor shops. A vendor usually keeps only 1 brand and I am not sure how that brand is selected. The consumers dont even ask the name of the brand, the just say give me Bangla. I dont know what factor drives a vendor to sell one vs the other and I hope the govt has no role to play in it.

6 Likes

@AmithGowda and others can you make sense out of the latest related party transactions made by Globus?

I am quite confused about the last entry in particular…holding of office/place of profit…what does this really mean?

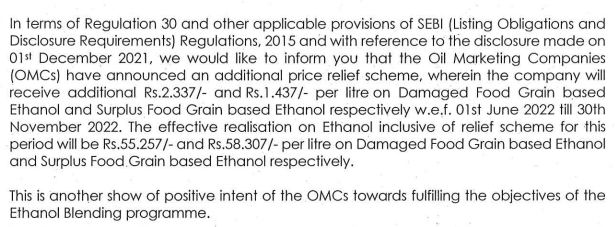

Price hike for ethanol is here.

3 Likes

screenshot of announcement

2 Likes