The article gets the capacity and addition numbers wrong but catches the drift on improving consumer business. No mention of the ethanol policy providing downside support to earnings due to guaranteed high capacity utilization as well.

I think the rally uptill now has been a value catch up, and Globus is still cheaper than other alcohol companies. Given that more than 50% of their business of ENA and Ethanol is in demand surplus territory where high continued realizations are likely, I see no reason why valuations won’t catch up with Radico or the likes on a price to sales basis. From there, I think valuation will start mirroring earnings growth.

I had posted a question previously, in case anyone knows the answer, please do share.

Disclosure: Invested in end June as a one year trading bet for valuation catch up.

Full portfolio here Vineet Jain portfolio

I don’t think the valuations will catch up with Radico. Radico is already at a place where globus aspires to be in many years. Radico already has a large share of Indian vodka, premium brandy and whiskey markets. Also it’s a giant in India’s largest liquor market, the UP. Unibev is still in early stages of blending premium liquor while radico has started making single malts. In fact radico has made full transition from manufacturing to consumer business.

I would say globus is a very efficient manufacturer of ENA and the ethanol policy has just been a shot in the arm. Their IMIL/ consumer business is picking up very well. They are able to introduce variants of their IMIL esp ones with higher alcohol content. Earnings may see significant improvement with new capacities coming online. So even without a PE re rating we may see prices going up. If govts are able to curtail sale of illicit liquor, the company will be a key beneficiary in the short term. Entering Jharkand with a green field capacity will add to their IMIL business.

For me key monitorable will be the sale of IMIL( no of cases) on a QoQ basis.

Regarding, ethanol policy there was a intersting thing, an EOI was floated by OMCs solely for procurement of ethanol from deficit states on a long term basis.

SYSTEM ID - 86996 dated 27.08.2021

TENDER REFERNCE NO. – 1000374174

This puts Uttar Pradesh out of the equation where bulk of ethanol capacities are. All of globus’s capacities are in deficit states.

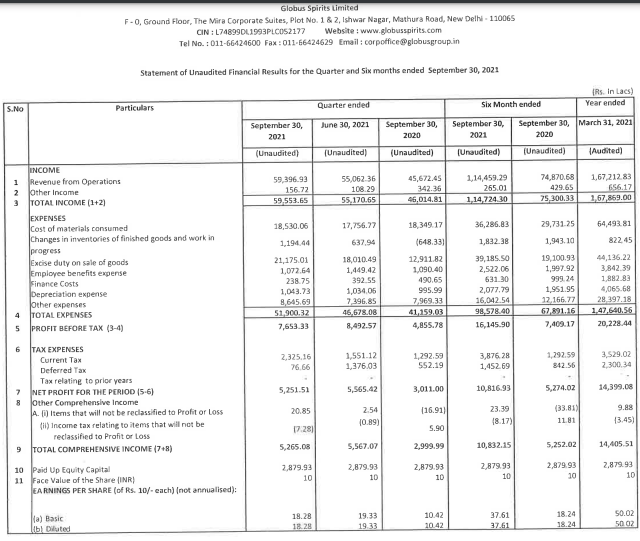

I had the same doubt about the P&L you mentioned

Discl: Invested and biased. One of my largest holdings

Hello Mr. Jose, I am Shounak, a new investor on Valuepickr. I just had a quick question for Globus Spirits: we are observing a lot of capex plans which have a significant portion towards Ethanol blending. Could you please color on how would Globus compete with sugar producers on ethanol blending?

Also, on post capex, is there any gestation time in the liquor industry before the operating leverage kicks-in?

Would suggest to read few last concalls from screener as some questions are very basic. For example,

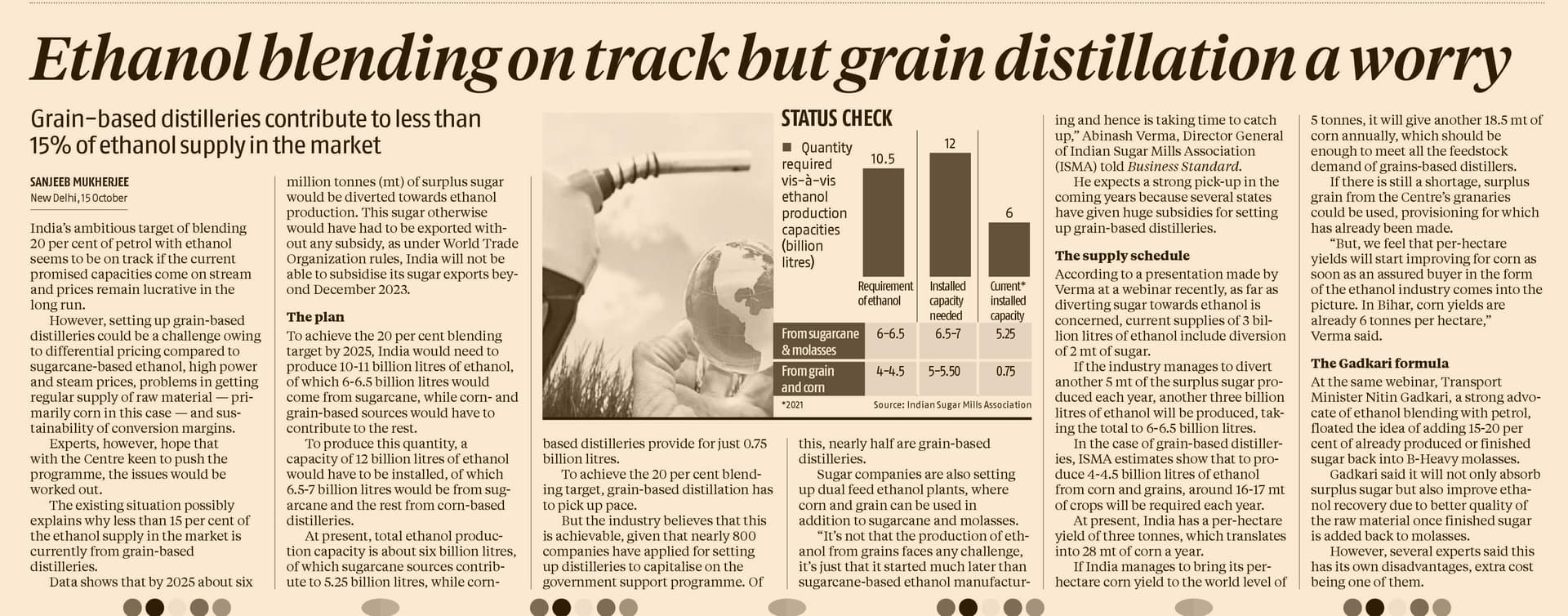

India is currently deficit in ethanol capacity/production vs demand from govt for blending. So there is no question of competing. Now the situation is, if you can produce it, you can sell it to govt (well, almost). The price is fixed by govt. That’s why you see many companies announcing ethanol production capex.

In a typical scenario, when a company puts up a capacity, it will take up few months/quarters to ramp up the production to 100%. But, demand would also be a critical factor to decide how quick company can use 100% capacity. Normally the capacity would be put up keeping next few quarters/years of demand in sight. With time, as more capacity gets utilized the operating leverage will kick in. However, in case of Globus, the scenario would be slightly different. The capacity would get first utilized for IMIL, and the residual capacity would also get utilized for ethanol (since there is dependence on demand ramp up in ethanol, as I explained in previous answer). Again, IMIL has better margins than ENA, which has better margins than ethanol. So you see, if IMIL growth rate keeps up, then margins can keep improving for some more time to come even after 100% capacity is utilized by mix of IMIL & ethanol in initial days. Hope i have answered your question.

There is no direct competition as it is. Latest ethanol blending policy has brought in a lot of interest especially from sugar mills. Most of these new capacities are coming up in UP or other sugar surplus states whereas Globus’s capacities are in ethanol deficit states like Rajasthan, Haryana, WB and Bihar. From what I understand, There’s usually no gestation period for full capacity utilization. Demand decides capacity utilization. Company has some advantages over sugarmills in terms of raw material, location,freight etc. However, prices of ethanol is decided by the raw material used.

Please note that the company’s price has appreciated a lot in the past few months.

Is there going to be amalgamation M/S Unibev Limited with Globus Spirits ? Can some Knowledgeable investor throw some light ? 6206e2ae-143f-4645-9ab7-b84d0170490d.pdf (249.5 KB)

Globus mostly uses broken rice as feedstock and company doesn’t see any margin pressure due to raw materials in the short term. Secondly, govt has allocated 78000 tonnes of rice from FCI for ethanol blending at Rs20 per kg as part of EBP . Company did say that they procured some quantity of rice from FCI to see how this works in one of the concalls in FY '21. So I don’t see any immediate issue with raw materials. It’s true that prices of ethanol is fixed based on the feedstock, but the current price of ethanol produced from damaged/surplus grains seems to be good for efficient manufacturers like globus. Also it will come up for revision in December. I think any delay as cited in the news will be advantage for companies like globus spirits.

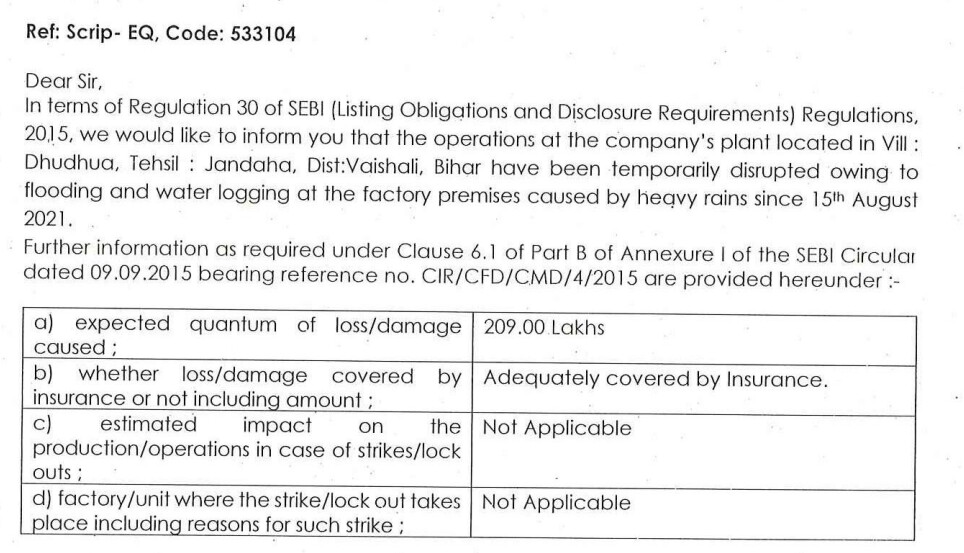

I think the recent correction is in-line with correction in broader markets , particularly w.r.t. the shares that have run up in recent past. Another possible reason is market is expecting muted sequential earnings due to flood in Bihar unit from mid of August ( see corporate announcement on 2nd Sept).

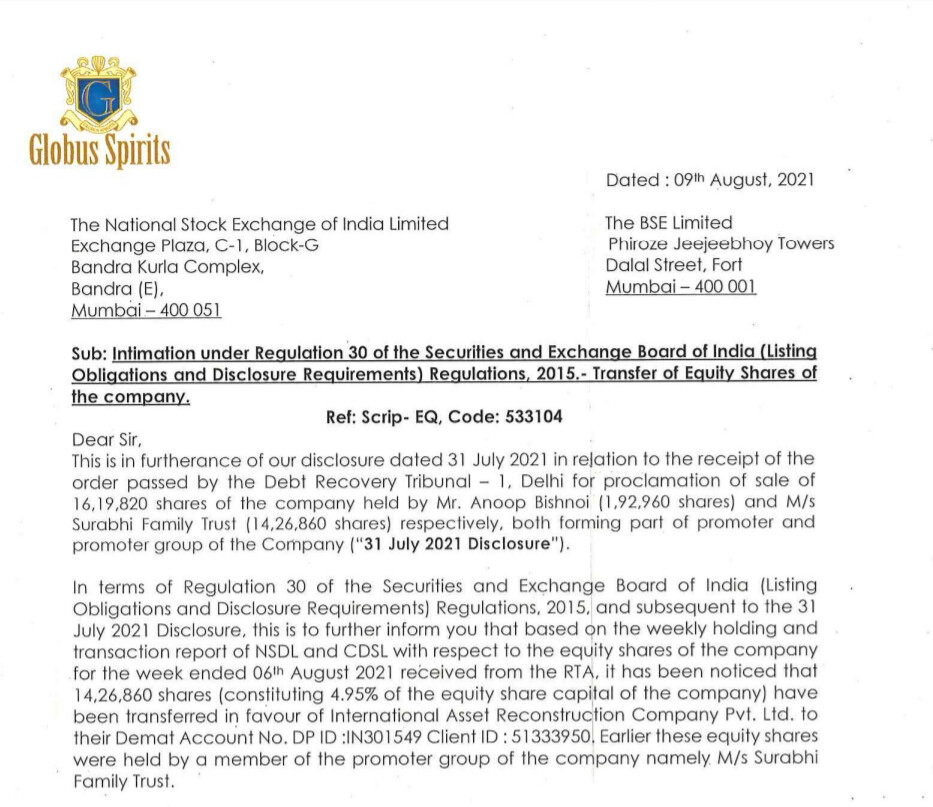

The promoter stake change is only with respect to Bishnoi family’s holdings which were transferred to International Asset Recon Company. Dont think the family has any active role in management of Globus Spirits ( cant be sure though).

The estimated loss amounts to 2 cr which is very small and the same is covered through insurance, also as per them the impact on business is “Not Applicable”, meaning the impact is none or negligible

I think loss should be actual material /equipment damages. But this clearly has resulted in factory closure for some time ( no announcement of reopening till now). Not sure if they will classify loss of production as loss or as factory closure due to strike.

Anyway, let’s see the results , hoping the the effect isn’t much.

I also didnt take the flood too seriously. Last year also there was loss of some days due to flood in Bihar. I was expecting the facility to restart production, but there has not been any disclosure so far regarding recommencement. This could be one of the reasons why they were rethinking about the location for the next expansion. They have still not announced anything regarding capacity expansion at WB. However, I expect margins to further improve in Q2.

Revenue nearly doubled for GM Breweries on a QoQ basis, so I expect IMIL sales to improve for globus ( as lock down caused some reduction in sales in Q1). It cant be a peer to peer comparison as Maharashtra was much more severely affected by covid second wave

Discl: Biased due to investment. Have added in last 7 days. I may have discounted the effect of flood due to my holding.

The date for board meeting has not been announced as yet. I expect the meeting around 8/9 of Nov and an announcement of this by 01 Nov. QE Jun results were declared on 08 Aug .