If you could describe briefly your rational behind pickup these scripts then other superior boarders could share their thoughts.Which will make sense to all.

I have been investing in Mutual funds for last 12 years and lately I have started investing in direct equity since 2013. I try to buy and hold stocks. I try to follow global and domestic news/developments and research stocks which is likely to benefit.

My mutual fund holdings experience has taught me not to panic during bad times and eventually it pays to hold long term. I hope to do the same with my stock holdings as well.

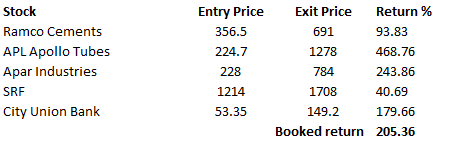

Most of the stocks appear to be overvalued. I haven’t tracked all of them. The following appear to be on the commodity business and are likely to have subdued growth w.r.t the sector and will exit them and move into larger company that is likely to move at the same growth rate (and thus better returns):

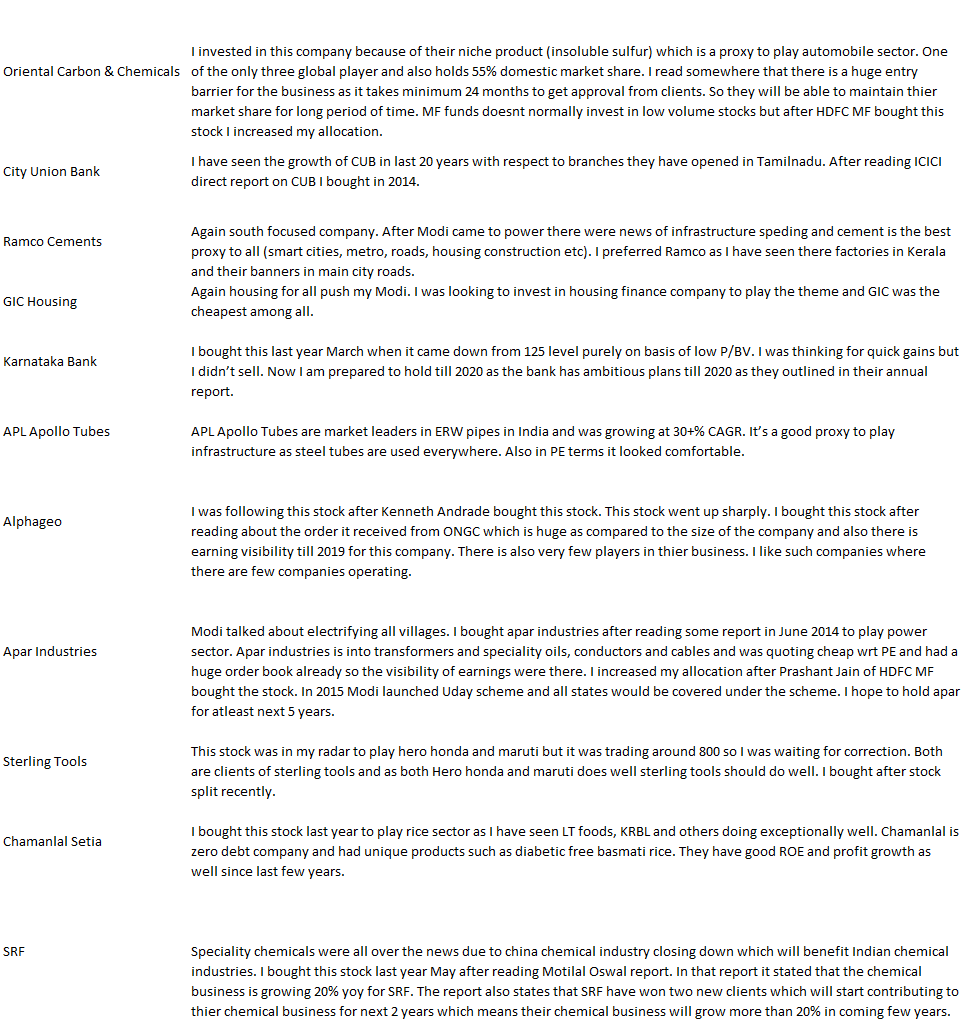

Citi Union Bank: subjected to all-round competition, having lost the perceived edge.

GIC Housing: Housing may grow after a short lull, but it is really a commoditized space - even otherwise this company lacked the aggressiveness and evaluation expertise of a DHFC or HDFC.

Apollo tubes - at the mercy of buyers and raw material prices.

All the above stocks have seen better time, though you will see a short term spike in GIC housing - I would use that opportunity to offload.

City Union Bank - They are doing good within the small/mid bank universe. If you see the results of CUB of last few years they have done quite well. I hope they will continue to do well in the MSME loan growth and govt giving tax benefit of 5% to sub 50 cr industries will help CUB increase the loan growth. Other small bank which looks quite good is federal bank but it has been in limelight and everyone is talking about it lately.

GIC housing - You are right they lacked aggressiveness but lately they have started working on it. They have increased their branches from 33 to around 60+ in last few years. I hope those new branches will start yielding results and add to their profits. Its a boring stock and not fancied like can fin homes or DHFL but I think in coming years all the housing finance companies to do well and GIC will also benefit from housing for all push from Govt. GIC is also consistent with their growth in last few years.

APL Apollo Tube - They have a strong order book and are market leaders in their segments. Yes their profits depends on raw material prices but they are also the beneficiary of Infrastructure play as Govt spending has increased in this year budget. Also, I have been holding this stocks from lower levels so I am comfortable to hold this stock for few more years.

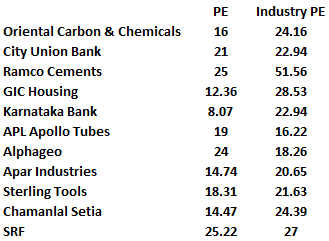

If I compare the PE with the industry PE of all the stocks I think there is still room left in most of them. Though I know PE is not the only criteria for judging the stock valuation can be misleading as well. But just to put some numbers to compare.

Thanks George! That’s terrific and helpful - obviously you would have done

more homework on this, to hold unfavored ones. I had such success with a

few - a few were GM Breweries, RPG, Tata Elxsi - offloaded them when they

became too expensive, though it surprises me to see Elxsi in hot

recommendations even at this price. I do not see that over-heating in your

portfolio and therefore may not carry risk of erosion.

Have started tracking alphageo only recently, no idea about other stocks. Alphageo has come out with excellent results yesterday. This was the first quarter since they got their large orders from ONGC as no seismic survey is carried out during monsoon. This result (quarterly sales equal to last year annual sales with good profits) is a confirmation of the capability of the company to execute such large orders which are 15-20 times their average annual sales for the last many years. Company is in business for more than 25 years, prudent management, survived through good/bad cycles, debt free status and week status of competitors bodes well for the company.

Most people are thinking it as an one-off order and question the sustainability over long term and what will happen after execution of this order.

Management commentary in the annual report provides some glimpse of future possibilities.

Still some orders for the NSP (National seismic programme) are balance,.

After completion of this survey and based on the data , there is a possibility that a more intensive seismic survey will be carried out by explorers"s/ Gont. who actually acquire blocks for further survey, development and production.

Based on prospectivity, opportunity opens up for acquisition of 3-D data.

Company is diversifying in other geographies viz. Myanmar, middle east etc.

Size, cash flow and track record will start working in its favour and company will have competitive advantage over other players.

In my opinion, It is a focused business with excellent future growth and profitabilty potential.

Thumps up for this stock.

Upfront apologies, I don’t want to hijack this thread to drift towards Alphageo specific discussion, still can’t hold from my two cents on alphageo.

Though I am invested in Alphageo from lower levels. However, even with that I don’t have visibility beyond 2018. All that optimistic thinking about getting 3D orders from OLAP bid winner for extensive survey, vertual monopoly, mote etc has a BIG ‘IF’ attached, that is…continued policy tailwind.

With the benefit of historical reference, government changes quickly and the policies even faster. All of the sectors floting/rising JUST ON policy tailwind may not command that great a valuation. Look at 15 years of top line/bottom line chart for Alphgeo and this very fact screams aloud.

Disclosure:

Invested

Underlying hypothesis : can hold till 18 and beyond subject to policy continuity

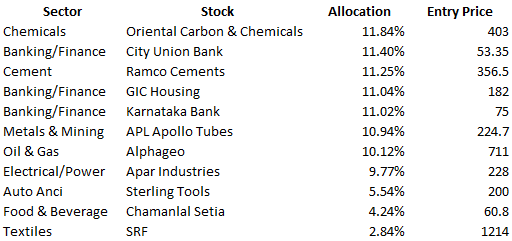

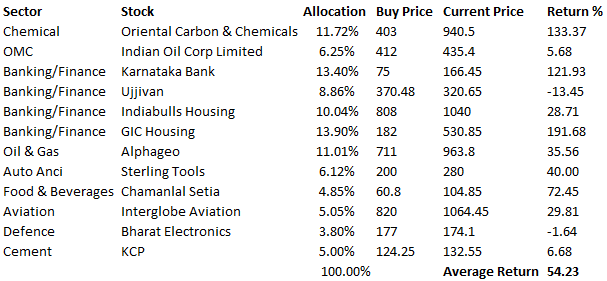

I am happy with the return from my portfolio and would like to bring the portfolio down to 10 stocks. I was contemplating which stock to exit but couldn’t able to figure out which one to exit.

Currently I am actively tracking Amara raja batteries, HPCL, Ahluwlia Contracts, UFO moviez, sterlite technologies and trident.

Falling crude prices help OMCs in growth. As per numerous reports crude oil is not likely to go up in a hurry. Recently they have completed capex of paradeep refinery which will help them increase their margin and market share. Recently all the OMCs have started daily price change that will help them forward any price hike or down to consumers. According to motilal oswal report IOC is expected to generate free cash flows over FY17-19 without any major expenses. So hoping that dividend distribution should be good and its also the cheapest amongst the peers. Plus its a consumption story. People buying cars (maruti sales increasing qoq) and bikes (eicher sales increasing qoq) will consume petrol/diesel. I have bought IOC because I have seen their petrol pumps crowded most of the time, it doesn’t matter to consumers if the petrol price is up or down as its a basic necessity nowadays. In metros and tier 1 & tier 2 cities nobody uses cycle anymore.

All the members in the valuepickr forum have great experience and insight in analysing stocks deep down and dig deep into every aspect of the company. Those analysis really help individuals like me who have very limited knowledge.

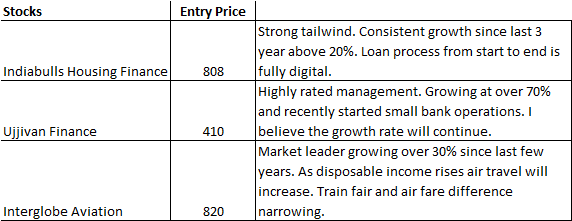

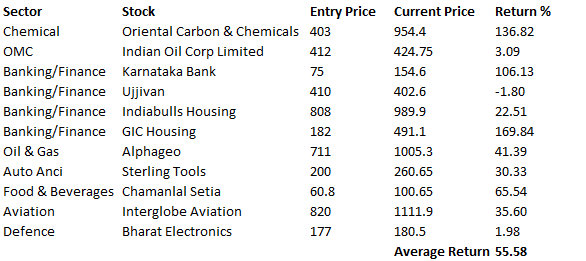

I have added a small cap stock KCP Limited to my portfolio. Also increased my holding in Ujjivan as it came down heavily due to bad results. I still believe Small Banking Licence will be game changer for Ujjivan with Mr. Ghosh at helm. Management has plans to convert Ujjivan into a full scale commercial bank in next 5 years and I am betting on that.

Rational behind adding KCP is its a cement company situated in the border of AP and Telangana. Telangana has acquired 33,000 acres of land for developing their new capital Amaravati. Govt will be spending huge on infrastructure to build the capital city world class. As per reports, the master plan is designed by Singapore Govt and Amaravati will hope to 13.5 million people by 2050. The new capital touches three national highways and seven growth corridors as per report. Cement is a proxy play to housing, construction, roads, waterways, railways, etc. They have done capex recently which will help them in their volume growth.

Apart from Cement they are into sugar, engineering unit, Ethanol Distilleries, hospitality and building materials. They also have huge land bank in Chennai.

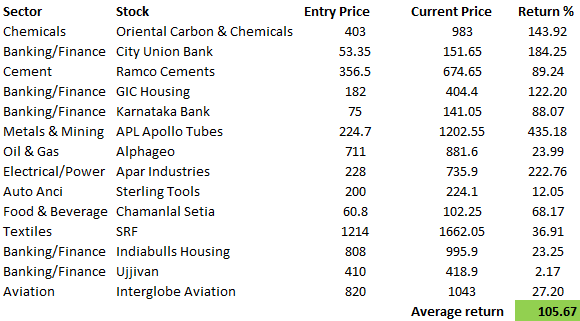

Current Portfolio

Your input/suggestions will be highly appreciated.

Please note that I am not a SEBI registered analyst. Please do due diligence before taking investment decisions.

Hi I am looking at KCP since some time now - I think valuations are cheap here so we are getting a good deal but my valuations are based on numbers and balance sheet but the thing to be noted is while all the cement companies had a good run up since last couple of years - this has not moved the same way and market knows more than we anticipate.Overall i would sum it up as less downside but uncertainty on growth and upside.Would start a thread on KCP soon. Please provide additional info if you have.Other wise portfolio looks robust. good going.

@nikhilv I dont think its Growth issue thats keeping the stock prices down, They have an Hotel which is loss making and the sugar business in Vietnam didnt perform well despite almost all sugar companies in India had a very good run. The results of the sugar division only gets announced once in a year and that is a fear which market has. Cement business is performing well and demand in AP and Telengana is good. Also the engineering division is loss making. Hotel, sugar and engineering has to perform well for them. In cement business they are doing pretty good and new capacities will come in by next year.

Agreed - but my point is its difficult to get into something just because it is cheap - i can wait but growth should be there but it is a very subjective thing… - also i just heard the comments from management and according to them the hotel business should do well going forward as average occupancy has increased.I have very less visibility to their sugar business and engineering - but isn’t the sugar business separately listed - kcp sugars ?? Though it is again a question that when all sugar companies are doing relatively well their side has not. @Hocuspocus32 - Do you have any report on how is the management - general view looks good - 75 year old company , paying dividend consistently ? Request to share more details.I would go through the AR too and share more.