@nikhilv

First of all KCP Sugar is different company.

KCP Ltd has a Sugar company as its subsidary in Vietnam and they report the numbers only once in a year.

Cement Sales was good last year had reported sales of 850cr against 770cr thats a 10% growth.

Profits was 113cr against 110cr. Realization per bag was good during the year too. So cement business is doing good, and 70%plus revenue in cement was contributed by AP & Telangana, the building of new city Amaravathi will really benefit KCP Ltd.

Sugar as I said didnt perform well it reported numbers 410 cr against 460cr and profit also was at 66cr against 78 cr .The performance was subdued because cane availability was lower.

Engineering segment reported higher revenues 30cr against 13cr and Loss was reduced to 2cr from 6 cr

Hotel revebue was at 4cr and loss at 2.5cr

As you can see from the revenue stream its the Cement and sugar thats contributing to the sales figures and Hotel and engineering is very low compared to them. Growth will definitely be coming from cement and if i have not mistaken in an interview in cnbc they have informed that they wont be adding any other business again which dosent have an relation to the core business like they did in case of Hotel.

Management seems to be genuine and I wasnt able to find anything bad about them( I did google searches mainly)

I dont have any report to share on this, all these datas are from there AR

Now if you see value at Rs100/- you should start investing in it as your view is long term . and if the prices goes down and Investor should always be happy as it gives you more buying opportunities. We cant enter at the lowest point and cant exit at the highest point, so first build conviction on the idea and once its build then buy it and give it time to perform.

@Hocuspocus32 - thanks for the details - I have done a very basic scan only and hence this mistake.their annual sales is at approx 1300 crore and market cap also same which in this kind of market is a good enough reason to have a look at the company.yearly scan says that their profit peaked out in 2012 and since then it has made low profits - which is gaining now since last year - DO you know why net profit dipped from 106 cr to 65 cr in 2013 and 34 cr in 2014. again many thanks for information.

@nikhilv debt is currently at 420cr i guess and it will go up because of the capacity expansion coming in and i guess it will go as high as 650cr then only it will start to come down.

and regarding the dip in 2013 I think it was due to the slow down in cement demand in AP& Telengana (partition was happening as two states) due to the political issues as well as weak demand , which could have lead to lower capacity utilization .

No idea about Chennai land valuations

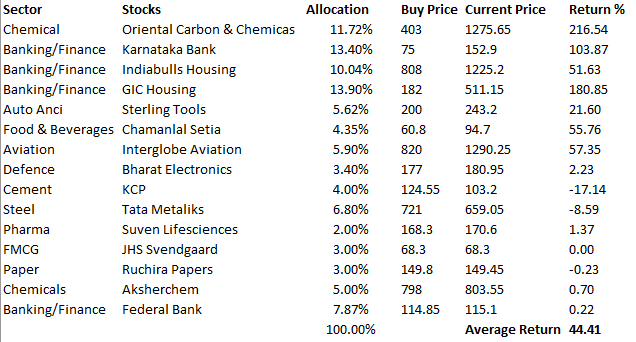

New one added to portfolio - Tata Metaliks @721 - DI pipe portfolio is doing very well and is likely to grow at 20%+. Kolte Patil @181.50 - Maharashtra Govt has approved affordable housing and send for approval to central govt. Pune and Pimpri chinchwad area has most number of affordable housing approved by state govt and Kotle Patil is a Pune based renowned builder with good brand name. Kolte Patil has also got redevelopment orders in Mumbai area.

Please note that I am not a SEBI registered analyst. Please do due diligence before taking investment decisions.

I have been tracking kcp industries and ncl since last few months…I have noticed cement companies in south specially andhra region have corrected cement prices in this qtr by 8 to 10%…The demand is going to pick up for sure but what will be the impact of the price cut on their bottom line? Have you calculated?

Sharing below one of the interviews of kcp management…

I am planning to add kcp to my portfolio but still not convinced…

Disc - still not invested

I have added Manapuram@102.5 to my portfolio today.

Below mentioned stocks which I added recently are recommendations of advisory service where I have subscription - I found their rational reasonable hence taken position.

Suven Lifesciences

Ruchira Papers

Manappuram

Please note that I am not a SEBI registered analyst. Please do due diligence before taking investment decisions.

Well with due respect I have high regards for Mr Malik for his capability of analysing the minute loopholes in a company with such surgical precision. Such analysis is good to know what the company and management had done in the past but it doesn’t always stay same for the future. The future may be good or get worse one doesn’t know and neither any such analysis can ever predict. For many such analysis might hold good to know as it gives them a sense of security that their money is invested in safe company with zero negatives in the past.

I am happy with investing in a company where even 60-70% positives is fine. It has worked for me in the past and I am happy to continue as long as it works for me. When something doesn’t work I learn.

I have stopped following his blog and post long back as his analysis was rejecting most of my stocks.

@Georgej I have just shared it since you added the stock into portfolio, its just a different perspective , I am not recommending to follow the blog and take any decision based on that , Its just that when we read we would get a better understanding of the stock that we own, Its true that all analysis is of the past data but it could well throw some light on our own conviction as well. Happy Investing

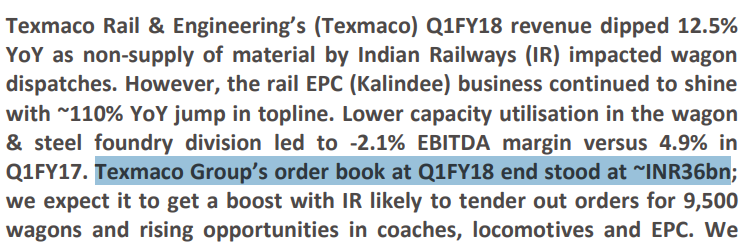

I have added Texmaco rail and Engineering@93.15 to my portfolio. It has recently acquired Kalindee rail and has a strong order book of INR36BN. Its a play on Indian Railways capex.

As per edelweiss report on capex recovery railways will see 3x more capital expenditure than other sectors. Texrail is well placed to get good pie of the order from IR.

Below are the few of the reports related to IR and texrail which says more interesting facts about the companies recent collaboration with international partnerships.

The below link will shed some light on Managements capability to crack a deal with international companies and how successfully.

I have taken token position in this company to track further developments. Future is not known and needs to be seen how it pans out for this company. They have not been doing well for last few quarters and needs to be followed thoroughly.

Any input/suggestion/red flags are invited.

Please note that I am not a SEBI registered analyst. Please do due diligence before taking investment decisions.

Market is bleeding and all the stocks which we wanted to enter came down but still mind says we can get it at lower levels. I always wanted to enter Canfin homes but it went up too fast. Today I entered the below stocks.

Can fin homes @2800

CG Power @69

Added more to my existing stocks -

Tata Metaliks

Federal Bank

Manappuram

Please note that I am not a SEBI registered analyst. Please do due diligence before taking investment decisions.

Added below stocks to my portfolio very recently: Orient refractories - Fundamentally good company. Good return ratios. Brownfield expansion ongoing. 20%+ yearly growth maintained since last 5 years. Mayur Uniquoters - GST play. Caters to automobile, footwear, home furnishing industries. Recently management said that Mercedes has visited their plant and they hope to sign the deal soon.

Trimmed positions in OCCL, KTK bank, Indiabulls Housing, GIC housing. Taken out money to buy other stocks.

Please note that I am not a SEBI registered analyst. Please do due diligence before taking investment decisions.