About Geojit

A LEADING RETAIL FINANCIAL SERVICES PROVIDER

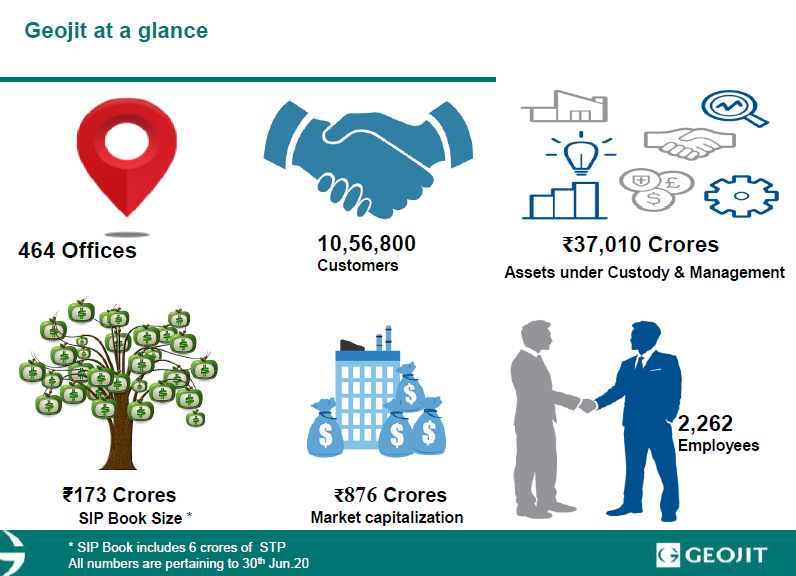

Geojit is a leading investment services company in India with a growing presence in the Middle East. The company rides on its rich experience in the capital market to offer its clients a wide portfolio of savings and investment solutions. The gamut of value-added products and services offered ranges from Equities and Derivatives to Mutual Funds, Life & General Insurance and third party Fixed Deposits. The needs of around 10,56,800 clients are met via multichannel services - a countrywide network of over 460 offices, phone service, dedicated Customer Care Centre and the Internet.

Geojit has membership in, and is listed on, the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE). In 2007, global banking major BNP Paribas joined the company’s other shareholders - Mr. C. J. George, Founder and Managing Director, Kerala State Industrial Development Corporation (KSIDC) and Mr. Rakesh Jhunjhunwala – when it bought a stake and became the single largest shareholder.

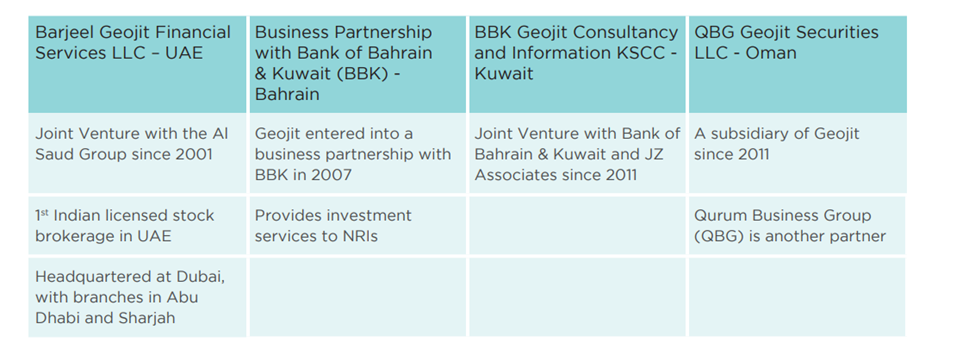

The company also has a strategic presence in the Middle East region in the form of joint ventures and partnerships. Barjeel Geojit Financial Services LLC, its joint venture with the Al Saud Group, is headquartered in Dubai, in the United Arab Emirates, and has branches in Abu Dhabi, Al Ain, and Sharjah. Aloula Geojit Capital Company, the joint venture with the Al Johar Group in Saudi Arabia is headquartered in Riyadh with a branch in Dammam. BBK Geojit Securities KSC, located in Kuwait, is a joint venture with Bank of Bahrain, Kuwait and JZA. QBG Geojit Securities LLC in Oman LLC is the joint venture with QBG and National Securities Company and is based in Oman. In addition, the company has a business partnership with Bank of Bahrain and Kuwait in Bahrain.

PROS

- Presence of BNP Paribas a french banking giant, Mr.Rakesh jhunjhunwala .

- Highest ever 9 months profits.

*Rs.792 cr of cash and equivalents. - more than 5% dividend yield.

- Company is almost debt free.

- Company is expected to give good quarter

- Company has been maintaining a healthy dividend payout of 87.43%

- Debtor days have improved from 131.50 to 92.44 days.

CONS

- The company has delivered a poor sales growth of 0.06% over past five years.

- Company has a low return on equity of 11.44% for last 3 years.

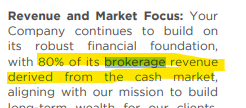

- Brokerage business is cyclic.

Profit & Loss

Consolidated Figures in Rs. Crores / View Standalone

PRODUCT SEGMENTS

| Mar 2009 | Mar 2010 | Mar 2011 | Mar 2012 | Mar 2013 | Mar 2014 | Mar 2015 | Mar 2016 | Mar 2017 | Mar 2018 | Mar 2019 | Mar 2020 | TTM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales + | 188 | 298 | 275 | 250 | 254 | 230 | 321 | 269 | 301 | 363 | 308 | 306 | 386 |

| Expenses + | 167 | 211 | 213 | 191 | 179 | 163 | 196 | 196 | 200 | 238 | 221 | 205 | 217 |

| Operating Profit | 21 | 88 | 62 | 59 | 75 | 67 | 125 | 73 | 102 | 125 | 87 | 101 | 169 |

| OPM % | 11% | 29% | 22% | 24% | 29% | 29% | 39% | 27% | 34% | 34% | 28% | 33% | 44% |

| Other Income | 44 | 5 | 6 | 7 | 51 | -109 | 5 | 3 | 4 | 5 | -6 | -4 | 1 |

| Interest | 1 | 1 | 2 | 4 | 3 | 2 | 1 | 1 | 1 | 1 | 2 | 3 | 3 |

| Depreciation | 12 | 14 | 16 | 14 | 13 | 11 | 10 | 13 | 14 | 14 | 21 | 25 | 24 |

| Profit before tax | 51 | 77 | 50 | 48 | 110 | -55 | 120 | 62 | 91 | 115 | 58 | 70 | 142 |

| Tax % | 20% | 37% | 37% | 51% | 20% | -40% | 31% | 29% | 33% | 33% | 48% | 27% | |

| Net Profit | 40 | 46 | 29 | 19 | 82 | -73 | 77 | 38 | 56 | 73 | 23 | 47 | 106 |

| EPS in Rs | 1.79 | 2.05 | 1.27 | 0.85 | 3.58 | -3.21 | 3.34 | 1.60 | 2.38 | 3.08 | 0.97 | 1.97 | 4.43 |

| Dividend Payout % | 28% | 37% | 59% | 88% | 28% | -3% | 52% | 62% | 53% | 65% | 103% | 76% |

Compounded Sales Growth

10 Years: 0%

5 Years: -1%

3 Years: 0%

TTM: 29%

Compounded Profit Growth

10 Years: 1%

5 Years: -8%

3 Years: -4%

TTM: 193%

Stock Price CAGR

10 Years: 8%

5 Years: 11%

3 Years: -19%

1 Year: 115%

Return on Equity

10 Years: 9%

5 Years: 9%

3 Years: 9%

Last Year: 10%

Its my first Topic post in the group so please correct me if i am wrong any where…

Disc. :- Invested with 9% of my PF.