Garware Hi-Tech Films Ltd (GHFL) has incurred a capex of Rs. 270 crore over the last two years. With the help of this capital

expenditure, GHFL was able to vertically integrate its business, strengthen its dealer network, launch its new product (PPF), and

increase the capacity of its current goods (SCF). Thus, ramping up of capacity provides the company with strong medium-term

growth visibility.

• GHFL has continuously increased the share of value-added products within its sales mix. Value-added products, which accounted for

48% of total sales in FY2017, increased to 80% in FY2023. This led to an improvement in its margin to 18.7% in FY2023 from 9% in

FY2017. As the company is planning to ramp up the capacity of value-added products and add new products, margins will continue

to improve going forward.

• The company has fully vertically integrated chips-to-film manufacturing facilities. These capacities are fungible and capable of

delivering customised products across a range of over 3,000 SKUs. Backward integration also helps the company’s R&D department,

as it leads to greater customization, faster time-to-market, and improved quality.

• Key risks: Sharp surge in oil price could impact margin/earnings. Sluggish demand in the automotive and real estate Industry

Results are out, please go to the below link -

https://www.bseindia.com/xml-data/corpfiling/AttachLive/57cd927c-6e41-4ee9-8e5e-24919d2cc8ab.pdf

Almost no change in topline yoy and degrowth of 5% in bottomline.

You was right @phreakv6 their PPF line is operating at peak capacity backed by orders from US clients.

Also the company is debt free and has 350cr of cash which can utilised for expansion.

Disclosure - Invested and holding.

@phreakv6 Could you please share your views on Garware Results and how things are looking for future. Thanks.

Saw this reel on Garware PPF product quality, just thought of sharing it

XPEL seems to be on a troubled path.

We are short XPEL, Inc. (“XPEL”, “the Company”) for two reasons. First, we believe the Company has grossly understated its reliance on Tesla, which just last week signaled that it would be disintermediating XPEL. The Company responded by claiming in a Form 8-K that Tesla represented just 5% of YTD revenues, yet we believe the true figure is many multiples higher.1

As per Culper research XPEL revenues highly correlates with TESLA new car sales. It also states that Entrotech is going to disrupt PPF market by integrating their technology directly into paints.

In May 2023, XPEL’s long-time supplier entrotech formed a JV with PPG.

The announcement saw little fanfare, yet we believe presents an existential risk to XPEL’s business. In fact, we spoke with a representative of the JV who indicated to us that entrotech and PPG have effectively integrated protection technology directly into OEM paint, hence disintermediating XPEL’s aftermarket solution. Moreover, they indicated to us that the technology is already being rolled out among the “Big 3” automakers with the anticipation that within the next 5 years, the entire aftermarket industry will be disrupted.

research report can be availed at Latest Research

A few snaps from XPEL’s Q3 concall (8th Nov) that maybe of relevance to Garware:

- XPEL CEO addresses the Entrotech-PPG JV and how the product compares with PPF in quite a bit of detail. The competing product is called Aero, a demo video can be seen here - https://www.youtube.com/watch?v=OQ3YDZh_tlw

- XPEL CFO highlights that one of their suppliers has had quality issues as a result of which they had to increase supplies majorly from alternate suppliers during Q2-Q3 CY23 (Apr-Sep). They don’t specify which product line, I assume the supplier was present in both segments. Coincidentally, this timeline coincides roughly with Garware’s spike in PPF exports. Could it be that Garware has been the beneficiary of this mishap at the other supplier’s end? If so, then the question to be answered is, is this PPF run-rate sustainable beyond Dec when XPEL expects inventories to get normalized?

- XPEL is opening an India facility (I assume its an office rather than a factory) with a view to taking a more direct approach to the Indian market. How will this play out vis-a-vis Garware’s own ambitions of dominating the local market? Would there be any collaboration here or pure competition?

It would be nice to get Garware management’s thoughts on these aspects in upcoming management meets or concalls.

Disc: Invested.

GARWARE HITECH FILMS -

Q2 and H1 FY 24 highlights -

Financial outcomes in Q2-

Revenues - 397 vs 395 cr

EBITDA - 65 vs 67 cr ( margins @ 16 vs 17 pc )

PAT - 46 vs 48 cr

SunControl, PaintProtection businesses - did well. Industrial products division witnessed some decline

Value Added sales @ 90 pc of total sales - very positive for long term. Commodity products sales now @ 10 of the total

Consumer Products division - ( includes sun control, paint protection films ) grew by 53 pc !!!

Industrial products division reported a decline of 32 pc in revenues

Paint protection film revenues doubled in Q2 vs Q1 FY 24 !!! This happened due robust demand from US and Indian distributors

Company has tied up with over 500 OEM car retailers for installation of PP films. Aim to tie up with over 900 dealers by next yr

Sun Control films grew by 8 pc vs Q1 FY 24

Expanding into architectural and decorative sun control films - should have a bright future going forward

Industrial Products business (IPD) de-grew sharply in Q2 due strategic focus on Consumer products division (CPD) and headwinds in IPD business. Seeing some recovery in IPD business in Q3

Company’s Gross Debt at - NIL

Cash Balance @ 350 - indicating strong financial position

Company has ramped up its marketing expenses wrt to both SCF and PPF business. This capped the EBITDA margin expansion in Q2. CPD is an invest to grow business with higher margins. That’s why the higher initial spends

Currently, the company is receiving overwhelming response in the CPD division

For SCF,PPF, Shrink films etc - company is the only fully backward integrated player in the world

Have spent additional 8 cr towards pushing the CPD in Q2. Likely to continue this kind of spending in Q3, Q4 and then revise it in FY 25

IPD business demand from North America was subdued in Q2 which led to business decline and a hit on margins. Hence, despite clocking much higher CPD sales, overall margins remained at similar levels as LY

Expecting North American IPD business to see some recovery in Q3

Have got commercial approvals from M&M for PPF coatings on XUV-700. Expecting approval from another 3-4 OEMs going forward. This should lead to more than decent volume uptick in domestic PPF volumes

Company still maintains a sales guidance of Rs 2500 cr for FY 26 - company is confident of achieving the same !!!

For FY 25, Architectural and Paint protection films should be the primary growth drivers

The new SCF lines are fungible and can be used to produce PPF products as well. Can be used in accordance with demand from these two segments. De-Bottlenecking can be resorted to further expand capacities

Company sees structural improvement in Gross Margins 18-20 months down the line

PPF sales in Q2 @ 120 cr ie 30 pc of topline. This percentage should further improve going forward

Sales from SCF @ 36 pc of topline in Q2. Business momentum in SCFs is also strong

In 2-3 yrs, expect 80 pc of business to come from SCF + PPF ( 40 pc each ). Expect remaining 20 pc of business to come from IPD

PPF penetration in Indian Auto Mkt is about 0.5 pc of total Cars. In China, US the penetration is > 10 pc. Company aims to take Indian penetration to around 2 odd pc of the cars

Disc: holding, biased, may add more if performance improves, not SEBI registered

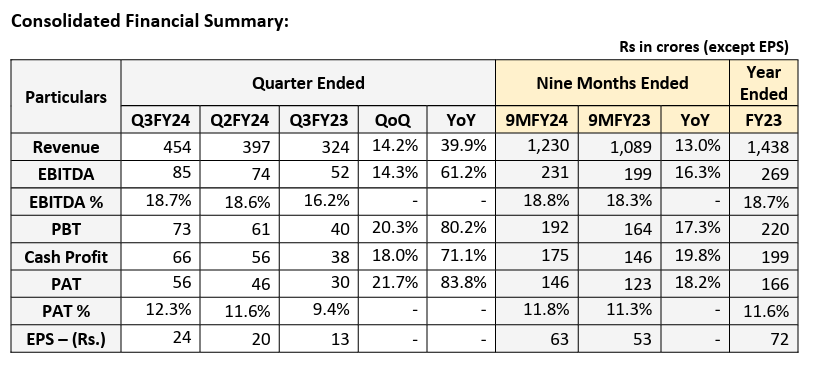

Q3 FY24 -Blockbuster Results

Records Highest ever quarterly revenues and profitability

Q3FY24 consolidated revenue up by 40% YoY at Rs. 454 crores and

PAT up by 84% YoY at Rs 56 crores

Paint Protection Film business continues robust performance, driven by significant demand increase, contributing one-third of revenue

Solar Control Film continues growth trajectory back with global demand recovery

Launched world’s first Rooftop series for the automobile segment

Robust response received in Expo - Automechanika and ACE Tech (Architectural)

Dr S. B. Garware, Chairperson and Managing Director of GHFL

"…Going forward, product innovation remains our cornerstone, coupled with aggressive

sales and marketing strategy, to drive us towards higher value-added products and

profitability.”

Ms Monika Garware, Vice Chairperson and Joint Managing Director of GHFL

" While the industry faced geo-political challenges, including “red sea crisis” and supply chain

issues in the later part of the quarter, our performance remained strong. This resilience is

attributed to strong demand for PPF, solid recovery in SCF across domestic and international

markets, supported by effective shipping and logistics.”

Business Updates:

Paint Protection Film (PPF)

The PPF business achieved a substantial 35% sequential revenue growth in Q3FY24 compared

to Q2FY24, due to strong demand primarily from USA, Middle East and India. Recent launch

of Ceramic Coating, complementing our PPF product line, aims to further enhance growth

prospects. The business delivered a significant 36% contribution to total revenue in Q3FY24.

The PPF plant is running at optimal capacity with intermediate processes supported by other

lines.

Solar Control Film (SCF)

SCF business accounts for around one-third of the company’s total revenue and has achieved

a 10% sequential revenue growth in Q3FY24 compared to Q2FY24, due to improved global

macroeconomic environment and surge in automobile sales. This growth momentum is

expected to continue with strategic diversification into the architectural film segment. The

architectural films products have made a successful debut at the recent ACE Tech expo,

garnering considerable interest from key stakeholders.

The company foresees accelerated growth in the untapped domestic market. The recent

unveiling of Rooftop series products at the Automechanika Expo underscores the company’s

dedication to meeting specific domestic market demands. Furthermore, the exhibition of PPF

products at the expo garnered significant interest from OEMs, retailers, and car enthusiasts,

reinforcing the company’s focus on domestic market potential.

IPD Business

The IPD business experienced a decline in Q3FY24 compared to Q3FY23 due to industry

headwinds. The capacity utilization of IPD plants stood at 72% in this quarter as compared

82% in Q3FY23. Despite this, the Company’s strategic emphasis on expanding its specialty

segments and improving capacity utilization underscores its commitment to strengthening

market presence and increase future profitability for the IPD business.

Revenue Growth

GHFL delivered a robust performance in Q3FY24, achieving its highest-ever revenue and

profitability. Consolidated revenues surged 40% to Rs. 454 crores and consolidated PAT

increased by an impressive 84% to Rs. 56 crores, compared to the corresponding quarter last

year, demonstrating the company’s strong financial momentum. The key growth driver in

Q3FY24 was the CPD segment, encompassing PPF and SCF businesses, which witnessed a

remarkable 80% YoY revenue growth. This remarkable performance was partially offset by a

9% YoY decline in the IPD segment. Notably, 82% of GHFL’s revenue comes from exports,

primarily driven by North America and Asian markets. Additionally, the company’s focus on

value-add films contributes approximately 91% of its total revenue, positioning it for superior

growth in the industry.

Margin

GHFL reported outstanding EBITDA growth in Q3FY24, demonstrating continued financial

strength. EBITDA surged 61.2% YoY to Rs. 85 crores, with the margin expanding to 18.7%

compared to 16.2% in the corresponding quarter last year. This improvement was primarily

driven by higher volumes in the PPF and SCF film segments. However, margin pressure on IPD

products and strategic investments in marketing and sales initiatives partially tempered the

EBITDA gains. While an aggressive marketing strategy has led to strong sales performance, it

has also resulted in temporary margin pressures. The company is confident that these

investments are expected to pave the way for sustainable growth and market leadership in

the long term.

GHFL IS cheap at fy 25 pe of 15 n 90 percent value added play n exports a B2C play UNDER OWN BRAND WORLDWIDE. GOOD RND TEAM MOSTLY FROM UDCT leading to innovative products like ppf,suncontrol n architectural films.its new MD deepak joshi is an intelligent fanatic executing beautifully a visionary in right age bracket of 40s. just buy on all dips.

marquee investors like ashish kacholia invested and guiding the next gen Monika garware who seems very keen to increase mkt cap like her cousin Vayu Garware of garware tech fibre n has appointed repute ENY as IR. gOOD CONCALLS N PLANT VSISTS BEING ARRANGED FOR VARIOUS PMS N AIFS. discl invested n biased

Garware Hi Tech Films -

Q4 and FY 24 highlights -

Q4 outcomes -

Revenues - 446 vs 349 cr, up 28 pc

EBITDA - 89 vs 70 cr, up 27 pc ( margins @ 20.1 vs 20.2 pc )

PAT - 57 vs 43 cr, up 34 pc

FY 24 outcomes -

Revenues - 1677 vs 1438 cr, up 16 pc

EBITDA - 321 vs 269 cr, up 19 pc ( margins @ 19.1 vs 18.7 pc )

PAT - 203 vs 166 cr, up 22 pc

EBITDA growth in FY 24 and Q4 driven primarily by increased sales of Sun Protection Films ( SPFs ) and Paint Protection Films ( PPFs) driven by extensive marketing and sales initiatives. SPFs, PPFs are higher margin segments for the company. However, the industrial products division ( IPD ) was muted in FY 24

**Company’s business segments - **

Consumer products division ( CPD ) -

Auto - Sun Control Films

Architectural - Sun Control Films

Paint Protection Films

Safety films

All these are value added products

CPD - constitutes 65 pc of company’s business

Industrial Products division ( IPD ) -

Value added products -

Shrink Films ( contributes 10 pc of company sales )

Electrical / Electronic Insulators

Release liners

Insulators + release lines contribute to 14 pc of company’s sales

Commodity products ( within IPD segment ) -

Thermal lamination

Plain Films

Packaging Films

These commodity products contributed to 11 pc of company’s sales

Launched titanium PPF with lifetime warranty

Launched new architectural films - DecoVista and Spectra

Expanding their PPF network / Garware Application Studios ( GAS ) to tier 2 cities ( total count now @ 120 + ). Now present in Lucknow, Belgaum, Goa etc. Aim to take the GAS + PPF distributor numbers to 200 in next 2 yrs

Company’s PPF is currently available in 650 dealerships. Aim to take this beyond 900 in next 2 yrs

Completed some new projects in FY 24 - Central Bank of Brazil, Biggest mall in Mohali, renowned developed in Pune for their residential projects ( for their SPFs )

89 pc of FY24’s revenue came from value added products ie - SPF + PPF + Shrink Films vs 80 pc in FY 23 ( rest comes from commodity films )

Company’s SCF manufacturing is completely backward integrated ( only company in the world to achieve this ). Company’s brands for these films are among top 3 brands in US+EU.

Also, Company is the sole producer of premium PPFs in India

Higher sales of premium/luxury cars in India is a huge tailwind for company’s PPF business. Current adoption rates in India are around 1 pc vs >10 pc for US, China

Company putting up a new PPF line with capacity of 3 lakh sq ft / yr. This is likely to go commercial by Q2 FY 26. Seeing strong demand in PPF segment. Total capex requirements for this should be around 150-160 cr

SPF sales in Q4 @ 185 cr vs last few Qtr’s avg of 150 cr or so. SPF sales momentum should continue as the overstocking related issues are now behind in US + EU mkts

PPF sales in Q4 @ 110 cr. For FY 24, PPF sales @ 450. Company is in advanced discussions with various customers in developed Mkts to sell company’s PPFs. Should see good breakthroughs going fwd

In the domestic mkt, company sees most of the growth to be driven by SPFs in Architectural segment. PPF segment should also continue to do well

Aim to hit 2600 cr of revenues in FY 26. Company believes, its on track to achieve the same

Company is seeing very good response from various automotive dealers from tier 2 cities

( like Lucknow, Kanpur, Raipur etc ) to take up franchise of GAS ( Garware application studios ). On an avg, GAS studios are doing PPF work on 15-20 cars per month per studio

@ penetration levels of 1.5 pc, company already has a ready addressable mkt of 60,000 new cars per yr for its PPF products ( in India ). With increased car sales and increasing penetration of people opting for PPF, this addressable mkt should keep increasing every year for a long time to come. For high end cars, PPF work costs upto 1-2 lakh per car

Company also does PPF work directly with Automotive OEMs

Domestic : Export sales breakup @ 20 : 80

40 - 50 pc of PPF + SPF exports by the company are under Garware’s own brands, rest are contract manufactured for other players

Garware has trained over 700 applicators across India for application of their PPF. These films are quite expensive and their application is an extremely specialised kind of Job

Company’s liquidity position is extremely comfortable. May even go in for inorganic opportunities to utilise the cash on books

Will continue to spend aggressively towards marketing and promotional events / ads - to grow the domestic business

Disc: holding, biased, not SEBI registered

The commodity spreads in the packaging films sector have started to improve materially in the last 3 months.

There’s a potential for even Garware’s commodity business to do well in FY25.

@Ahmed_Madha How we can track this numbers? Is there any website showing these numbers?

I see lots of commodity company started seeing improvement from last 1 month with respect to share prices.

Disclosure: Tracking this sector with investment in Jindal Poly and interested in this counter from long time but price keep running ![]()

Happy Investing,

Karthik

we can get the BOPP & BOPET prices from Jindal website. Not sure how to get the Polypropylene prices on weekly basis in Indian rupees. - Can someone help .

You can get the price list from https://www.plastemart.com

Hi. I am not able to find it on Jindal website. Please if you can be kind enough to paste the link to the page on Jindal website.

it does not give daily prices and historic prices on daily basis.

CFO Resigned

Polymer price list is given once every 15 days normally. Unless there is a requirement to increase in between, there are no changes until a fortnight.