GHFL reported good earnings yesterday.The concall was good too.Some highlights:

→ Witnessed healthy demand across product range,continue to operate at 100% capacity utilization.Value added films now >80% of revenue.

→ PPF has been tested,orders have started to flow in and product is gaining acceptance across geographies.Expect 40% capacity utilisation in FY22.Broke even at gross level in Q1.

→ NSE listing has been pushed away further.New SEBI rules require that stocks under surveillance category can opt for NSE listing only after a gap of 2 months,post exit from ASM.No clarity from BSE on this as of now but company has done all paperwork and is monitoring the situation closely.

→ Window films demand is higher than company is able to supply.Took price hikes in Q1 and will do more hikes in Q2,some LT contracts getting renewed soon.Trying to get back to 25% EBITDA,no commitments though on the timeline.

→ Subsidiary Garware Chemicals’ product range had become obsolete.Oversupply in the markets,poor end product prices led to shutdown.Company tried to switch to bio-diesel but the condition put by buyer countries was to sell only to Govt…However,the offers were at uncompetitive prices.Usable equipment was shifted to other plants of the company.

→ Lost 2 patents recently(20 years over) Company had developed in-house tech for dyeing the polyester which helps to increase the life of the film.Garware doesn’t sell this outside but one other company supplies to all their competitors.

→ “Processing charges” are on account of an intermediary product that is manufactured by another co. of Mr. Garware.This is a unique tech so GHFL doesn’t want it to be sold outside.GHFL used to buy dyed film in 2014-15,shown under RM cost.All dealings on arm’s length basis.

→ “Some thinking” going on regarding the huge land parcel,nothing concrete as of now.

→ Appointed an exclusive person in US for positioning “Global” as a B2C brand.

→ No public study to compare quality of GHFL’s films with competitors.However,at a “tint-off” event held in Orlando,a randomly chosen GHFL film from a bouquet of other company’s films, GHFL’s product ranked 2nd(out of 96 competitors) Product was judged on ease of application,speed of application and quality.

→ PPF is self-healing & leaves no scratches.Coloured films are banned in India for application on cars.However,film can be applied during manufacturing by the OEM.Coating is done on accident prone areas of the car. US is the biggest market,followed by EU and Middle East.Company has good presence in all these regions.

→ If applied within 1 year of buying the car,PPF helps to retain the look of the car for over 5-7 years.The car looks brand new.This leads to much better resell value.GHFL is offering 10 year warranty.

→ Facing lot of freight/logistic issues on the export side.Otherwise,co. could’ve done even higher revenues in Q1.

→ Already started advertisements for PPF.Undertaking tinter training programs on product usage,etc. and also deploying virtual showrooms for full product range.Currently in touch with over 4,000 tinters.

→ No succession issues.Each daughter taking care of different segments: one oversees production,finance.Other handling R&D+HR.While the third one is managing international marketing.They keep rotating these responsibilities among each other.

→ Other income on account of investment in Garware Technical Fibres,value of stock has gone up meaningfully bumping up the line item.

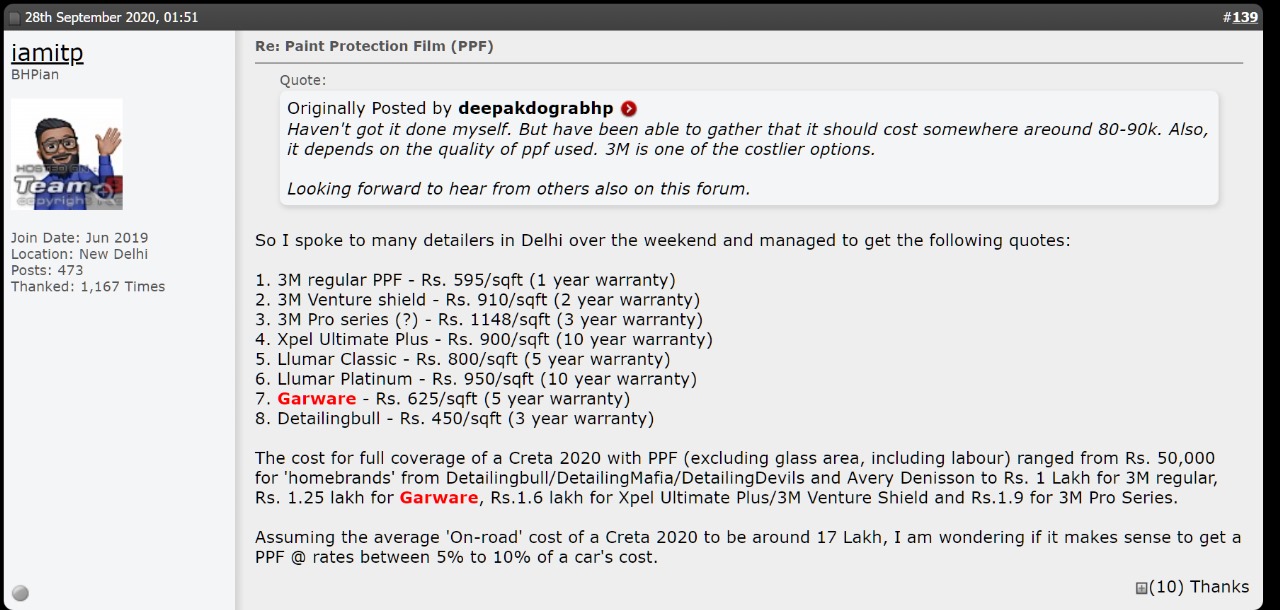

→ 6-7 lk cars/month is the addressable opportunity in India for PPF(any car above Rs. 15 lk selling price) The PPF on a Mercedes would cost Rs. 120k if applied on the complete car.Have 22 dealers currently,developing the market in India.Also see a huge market for architectural films on tinted glass.Film can absorb UV radiation & even radiation from nearby telecom towers.GHFL will seriously look at this market only post new capacities coming on-stream since all existing capacities are being used for other products.

Company seems to be moving well with it’s stated plans while demand for existing products continues to be strong.

Disc.: Invested.Views are biased.