My first post in the forum.-

The Company : Garware Polyester Limited (GPL) founded in the year 1957, is the pioneer and the largest exporters of polyester films in India. GPL is the only manufacture of sun control window films in India and a trend-setter in Sun Control Film industry with a history of more than 3 decades of technological development. The Company has four manufacturing plants for Polyester Film and manufactures Film of thickness ranging from 10 micron to 350 micron.

The Company possesses Patented Technology for Dyed Polyester Film in India and USA and is the Second Company in the world to possess such Technology. The Company is already backward integrated through the establishment of a Batch Process Polyester Chips plant which ensures a steady stream of supply of chips for the Film Lines. The BOPP line set up by Company in last year was part of the Company’s efforts to ensure forward integration too. Thus Company’s strength is its integrated manufacturing facilities, R&D Center and development of specialty products for various applications.

Products : The Company manufactures Bi-axially oriented polyethylene terephthalate (BOPET) / Polyester Films, Sun Control Films, BOPP Films, Thermal Lamination Films and Specialty Polyester Films of high quality for a variety of end applications. GPL also manufactures the premium grade heat rejection films based on the latest `Nano Technology’ developed in its in-house R&D facility center. The Company has introduced Infrared rejection films which can reduce infrared heat up to 92%. It has also developed the film to reduce the impact of mobile tower radiation.

Domestic Business : Growing Retail sector, increasing preference towards packaged items, liberalization and rising middleclass is expected to increase in consumption of Polyester Films thereby adding to growth of this segment in the domestic market. Increased usage of window films in offices, commercial buildings and malls will continue to add to the growth of the Company’s business in the premium segment of window films. GPL has well recognized brands and integrated manufacturing facilities which are expected to augur well for the company’s future growth.

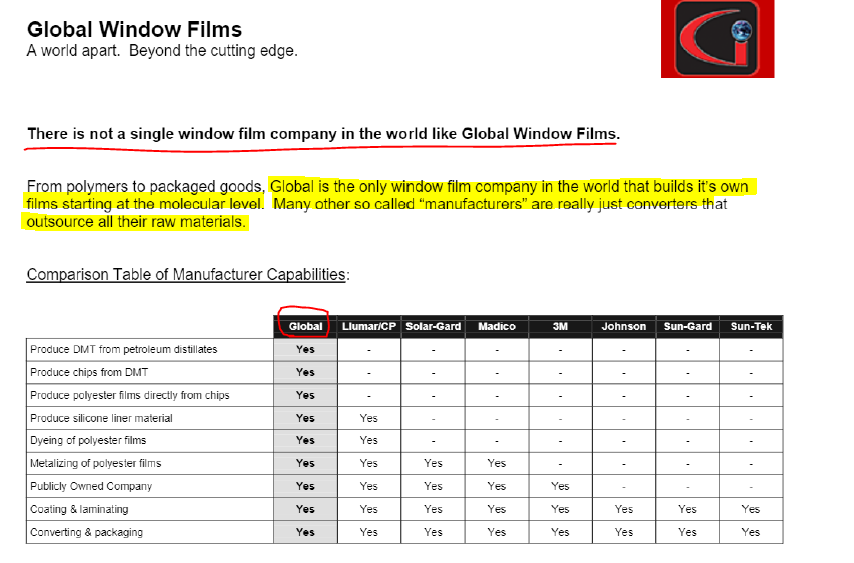

Global Business : Through its subsidiaries situated in USA and UK the company has developed a wide network of dedicated customers in Europe, USA, Far East, Middle East, Brazil, Australia, China, Russia, New Zealand, Eastern Europe, Mexico and Africa. The quality of GPL products is rated amongst the best in the world and the Company pays special attention on customer service and satisfaction due to which the customer base is consistent and increasing. The aim is to expand export base and catapult international operations into a major growth driver. GPF is the marketer of the brand ‘GLOBAL WINDOW FILMS’ which is registered in the US and is one the most popular brands. The subsidiary is catering to Russia, Europe, Asia-Pacific and Africa market film under the brand “Garware Sun Control”.

Future Strategy : The strategy is to focus on the specialty films, launch new products, strengthen network and Services and speed up brand building initiatives. Plans are afoot on a marketing warpath, overhauling the product portfolio and penetrate newer markets, launch aggressive advertisement campaigns. The shrink label application film is very well stabilized in the market. With demand outlook for High Shrink films remaining robust, the Company has plans to shift to the specialty PET shrink Films, where it sees a tremendous opportunity. In thermal film, GPL has developed Gold & Feather feel films. With foray into BOPP, GPL has now become the only company in the segment which will be manufacturing BOPET, Sun control Films, Thermal Lamination and BOPP.

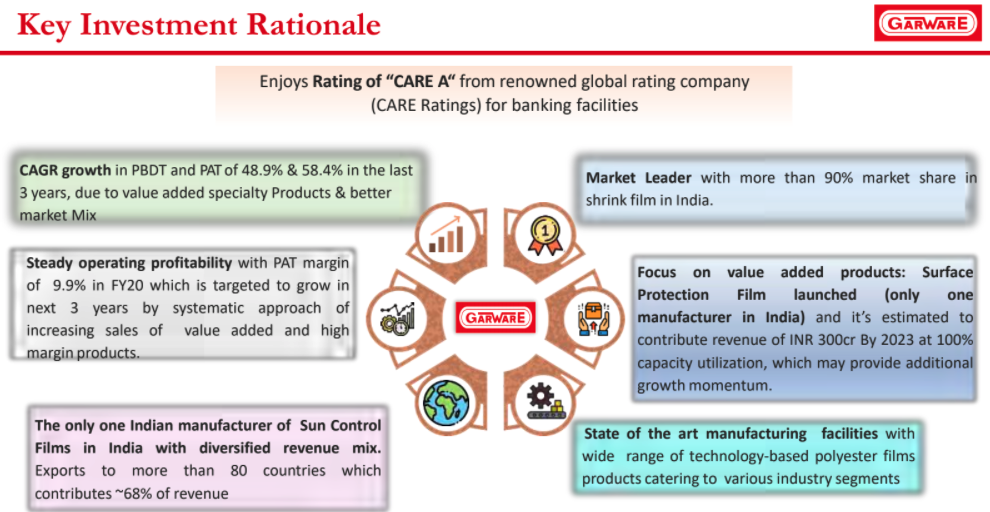

Valuation : GPL, a six decade old company with promoter holding of 61% (Zero Pledge) posted a Consolidated total revenue for FY 17 of 925 Cr & Net Profit of 19.9 Cr on an equity of 23.23 Cr giving an EPS of Rs 8.57 per share. Borrowing stands at 267 Cr (Short Term) and 19.9 Cr (Long Term) Finance cost remained 32 Cr. The company is having 4 Lakh shares of Garware Wall Ropes (At current market price of 850 per share, the value is close to 33 Cr)Freehold Land, Lease hold land and an entire Building in Vile Parle, Mumbai, near Airport, the value of which should be many times of current market cap (300 Cr).

If company can sell even part of its mentioned asset and retire the entire debt than savings on interest alone directly gets added to the bottom line, which can boost the EPS by 15 Rs per share. Debt to Equity Ratio is 0.63, Debtor Days at 19.31. With bottoming out of the Polyfilm Industry in near future and Softening of interest rates, and falling Crude price, the profitability of the company with reducing debt, may improve going forward by 15 to 20% CAGR for the next few years, plus the company is back on dividend paying list after 5 years, that shows confidence of management towards future growth of the company, hence Investor may study this asset rich company for long term investment.