Ganesh Housing Corporation Limited (GHCL) is one of the leading real estate developers in Ahmedabad founded by Late Govindbhai Patel.The Company is an established brand in Ahmedabad with an enviable track record of delivering over 22 million sq. ft.(msf) of residential, commercial and retail real estate projects.

For more info Check, http://www.ganeshhousing.com/

Numbers-The Latest

Marketcap: 595 Cr Approx CMP on Day 25Mar2018: 121

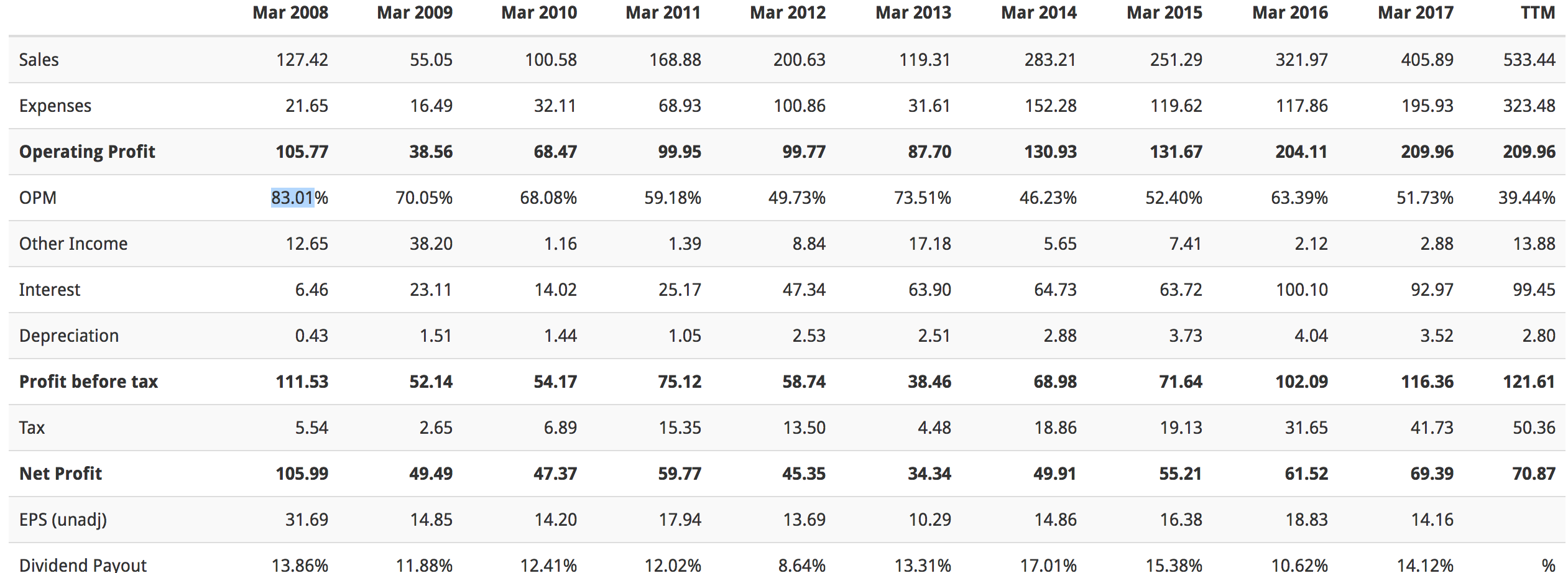

Revenue: 9MFY18 346 Cr Apx BV :150 Apx

Net Profit: 9MFY18 39 Cr Apx. FV 10

POSITIVES

1)Company enviable track record of delivering over 22 million sq. ft.(msf) of residential, commercial and retail real estate projects Since 1991.

2)RERA, REIT’s, GST, Demonetisation are the four big bang Changes made by Government which will help to prosper the organised players like GHCL.

3)Company Operates only in Ahemedabad which is emerging as one of the fastest growing cities in India with rapid infrastructural investment, development

of GIFT city and presence of major manufacturing industries and the entrepreneurial nature of the population.

4)GHCL to Benefit from Govt’s PMAY “Housing for All by 2022” and Infrastucture status to Affordable Housing as real estate market will be boosted like never before.

5)Company has Never Missed a Dividend Payout Since 2005 which shows the promotors attitude towards minority Shareholders even being a smallcap company.

INTERESTING INFO

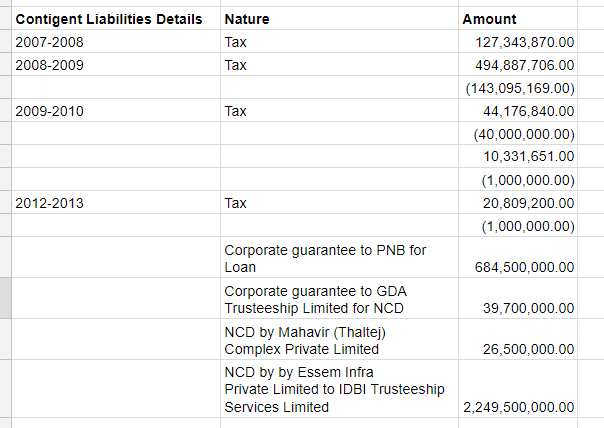

1)Piramal Real Estate Fund has invested Rs 225 crore in the form of debt in year 2015 giving confidence to investors of GHCL as disbursals are made by Piramal REIT only after high level of due deligence.

2)GHCL has one of the largest developable land bank in Ahemedabad, with more than 50 million sq.ft. of space, a Revenue Visiblity for Next 10 Yrs.

3)The Company has 4 on-going projects having a developable area of nearly 2.55 msf. It has procured one of the largest land parcel at very low-cost, across key locations (Sanand, Thaltej, Shilaj, S. G. Road, Chharodi) in the city of Ahmedabad having a total development potential of 22.47 msf.

NEGATIVES – POSSIBLE RISKS

1)Company is concentrated only in Ahmedabad Market so it faces Concentration and Political Risk if any in Future.

2)Any Drastic Global Slowdown in GDP Growth would affect the Sector as a Whole.

3)Any Policy Changes Regarding to Real Estate

MY TAKE

With Housing shortage in India of 62.5 million ,rapid urbanisation, govt’s focus towards housing for all by 2022 company like GHCL will benefit immensely.

GHCL operating in entrepreneural city of Gujarat which is one of the fastest growing Markets in India will prosper as the company will transform itself from a small cap company to a midsize company.

GHCL With 595 Cr Marketcap, High Operating Margins, Low PE, Lowest P/BV, High Curent Ratio, Lowest Debt to Equity than its listed peers clearly defines undervalueness of the stock.

Just on a conservative note if are able to repeat the past by just completing projects of 10-15 MSF out of 50 MSF in Next 5 Years company has a Cumulative Revenue Visiblity of 7000-10000Cr, Enabling Profit Potential 1300 Cr over Next 5 Years.

Stock is a Perfect Example of Growth at Reasonable Price. Investors in GHCL will have a great opportunity to participate in big 5 Year run benefiting from housing for all theme.