My mistake, thanks for clarification.

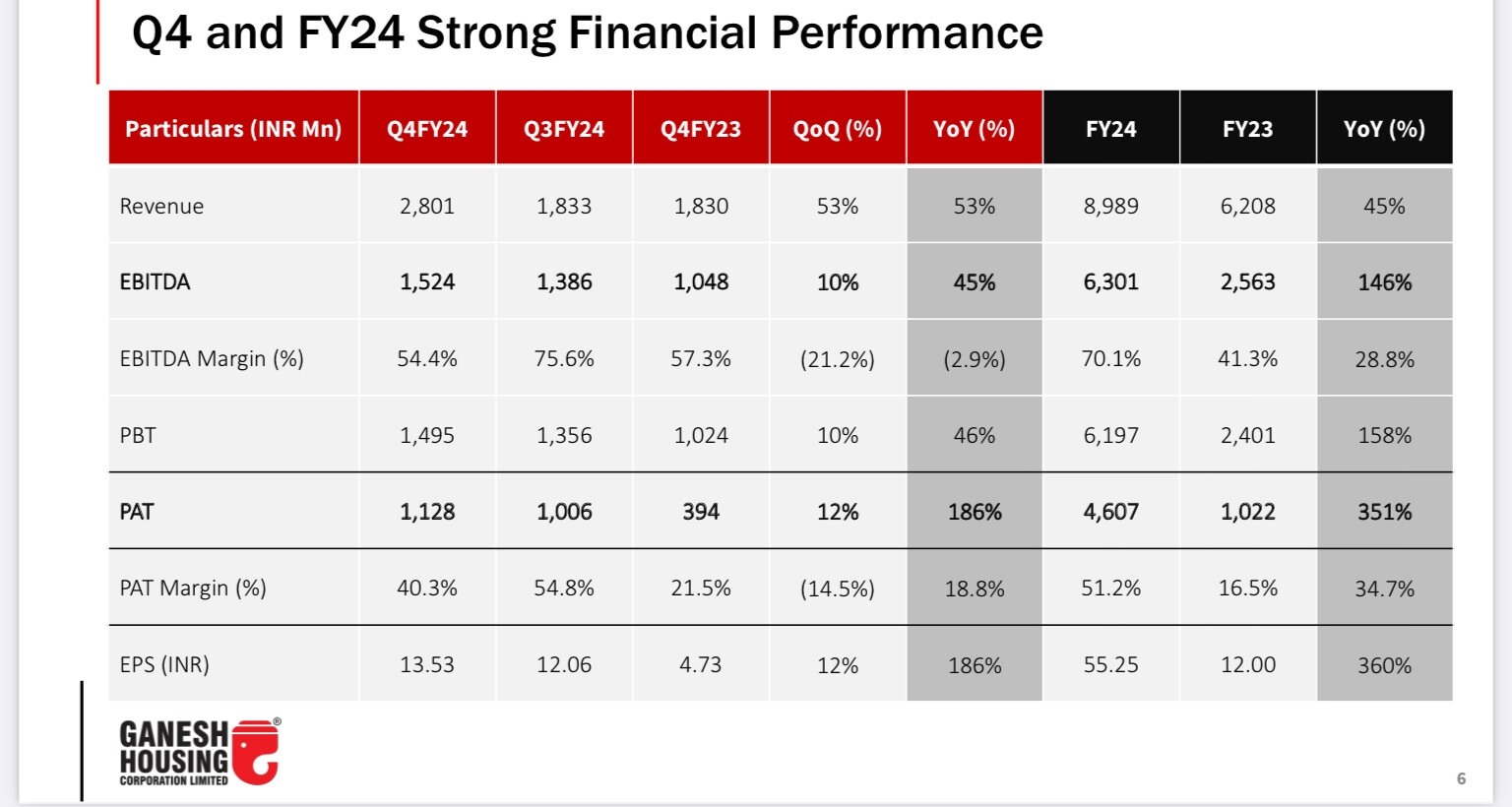

Sir company seems to do very good business good results but why market is not rerating it? Any idea or anything I am missing out? Thanks

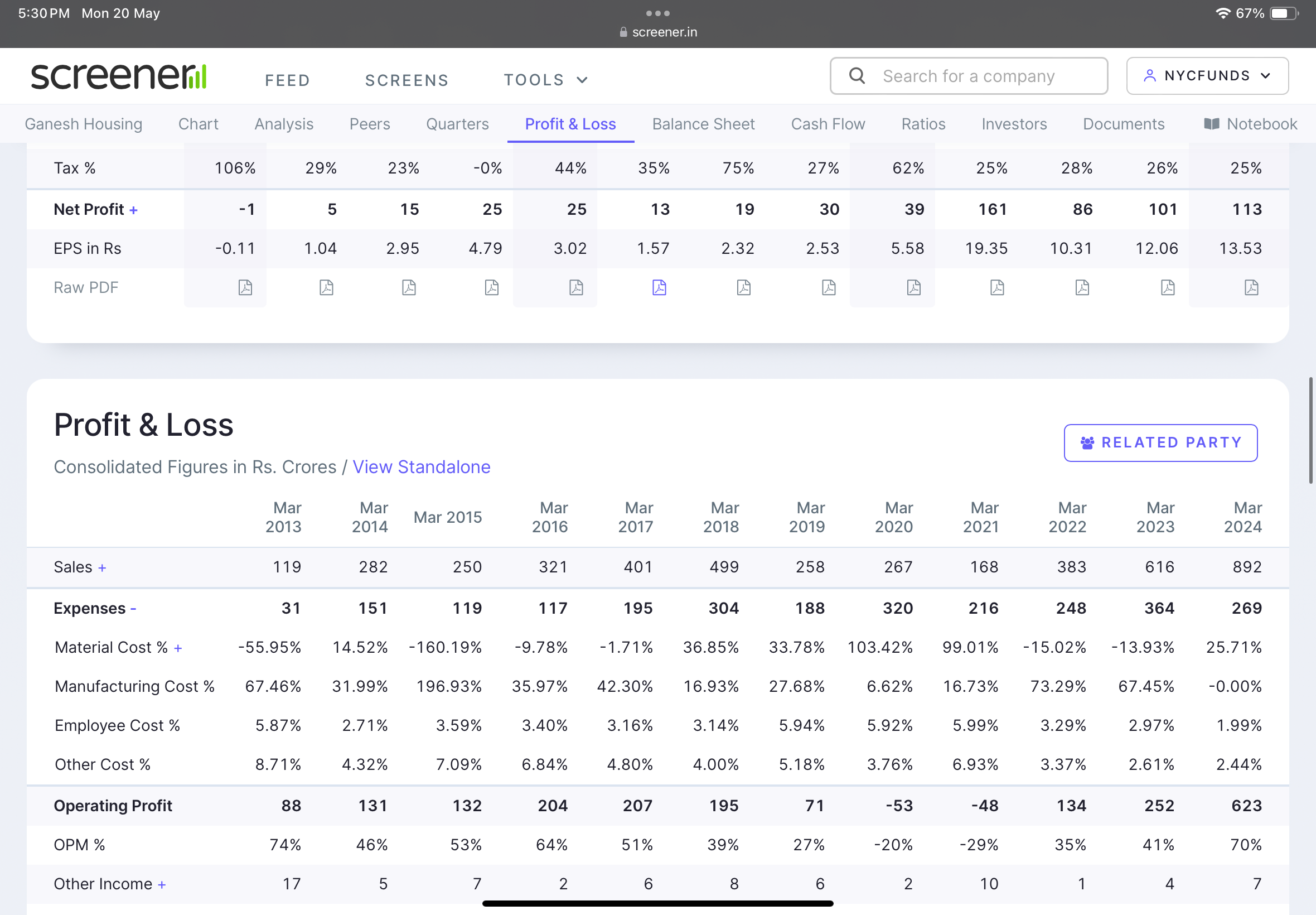

sir, one question if the land value is 18000 crore then should it not be reflected in balance sheet assets ? i see land in assets was only 175 cr in mar 2023 on screener

Company’s accounts reflect original cost of land

1 Like

Business Updates

- The trend of bookings in premium housing usually picks up after the first floor is completed and the sample flat is on show

- Q1FY24 was exceptional in one sense so its not completely comparable to the current quarter’s numbers

- Sequentially there will be a growth in all the quarters going forward

Participants

Nuvama Wealth

Profitmart Securities

Countercyclical Investments

Manya Finance

Arjav Partners

Oneup Financial

Antique Stock Broking

QnA

- Total sales value is Rs 450 crores and the cost is Rs 350 crores for the Malabar Retreat project

- The company has enough cash balance on hand for construction of first phase of the projects and pre sales from projects will be used to construct

- Most of the costs have already been done on land which is historical and now the only cost that remains is construction cost which is done from pre sales and customer advances

- In FY27 The Malabar Retreat project will get completed and that has a revenue potential of Rs 450 crores

- In the next 7-10 years the company will use all the land bank that it has on its books and value of land on books on a baseline can be estimated at Rs 20000 crore on a conservative basis

- Currently in no hurry for JV deals and can do this in future if an opportunity comes across but not for now

- The selling price in Malabar Retreat is around Rs 5500/sqfoot and the idea is to do at a lower amount initially and with new bookings done every quarter the price will keep inching up

- Post implementation of RERA and GST the real estate industry is now fully converted to organized. Even the smaller unorganized developers have converted themselves to the organized space

- There are multiple good developers in Gujarat which are doing very good in respective areas and around 15 odd developers in Ahmedabad have a good market share in the city

- Each good developer has their own niche which they have developed over the years and they have their own area of excellence in terms of land bank in respective areas

- No large developer in Ahmedabad will have more than 10% market share

- As of now no concrete plans to go out of Ahmedabad but there is a continuous evaluation of opportunities outside of Ahmedabad as well

- The cash balance was Rs 230 crores as on FY24 of which Rs 60 crores is still remaining. Looking at the way projects are planned the construction cost is already in the books and also being funded by advances and collections from customers

- There will be no additional equity or debt raised from the market to fund any of the projects

6 Likes

The financials looks attractive is a company in such a capital intensive business earning 70% OPM and is almost debt free? IS there something unique about their business model or is the books bogus ?

What method are they using to realise contract revenue?

1 Like

Large part of the sales in recent quarters is land which was bought at low prices historically. Hence the higher margins. Once the revenue shifts to developed sales, optically the margins will drop.

3 Likes

I have the same Question, However these lands are acquired very long ago and might not be revalued in balance sheet. the market value of this land must be much higher than 175Cr , but 18000Cr ?

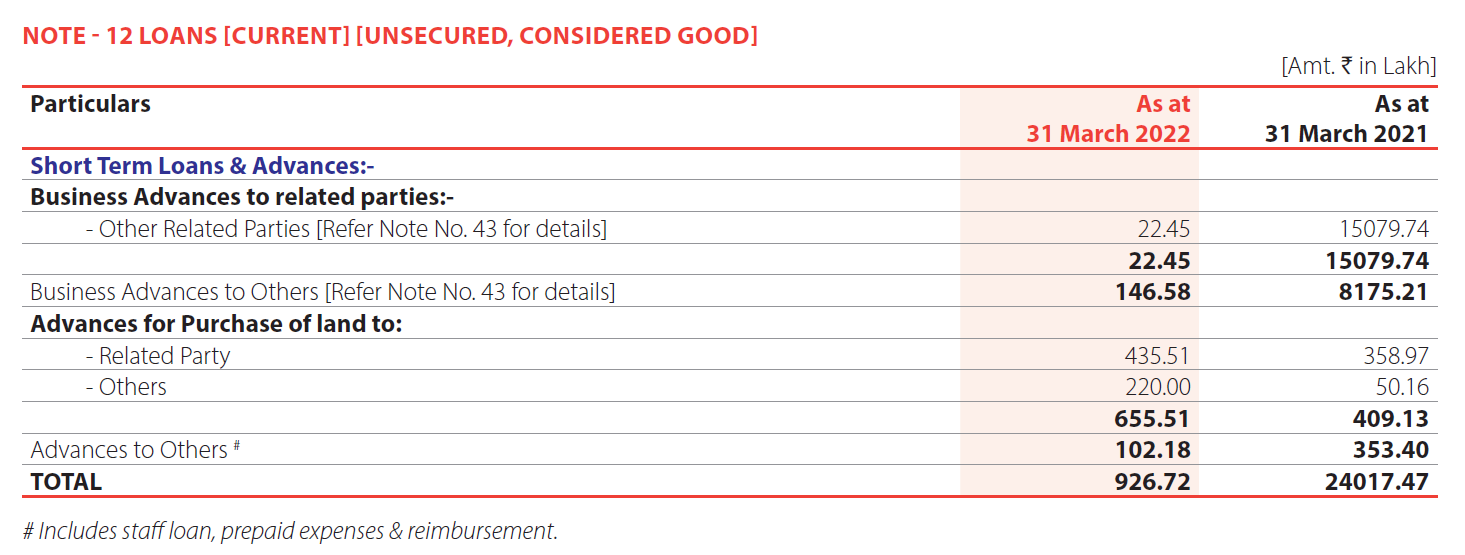

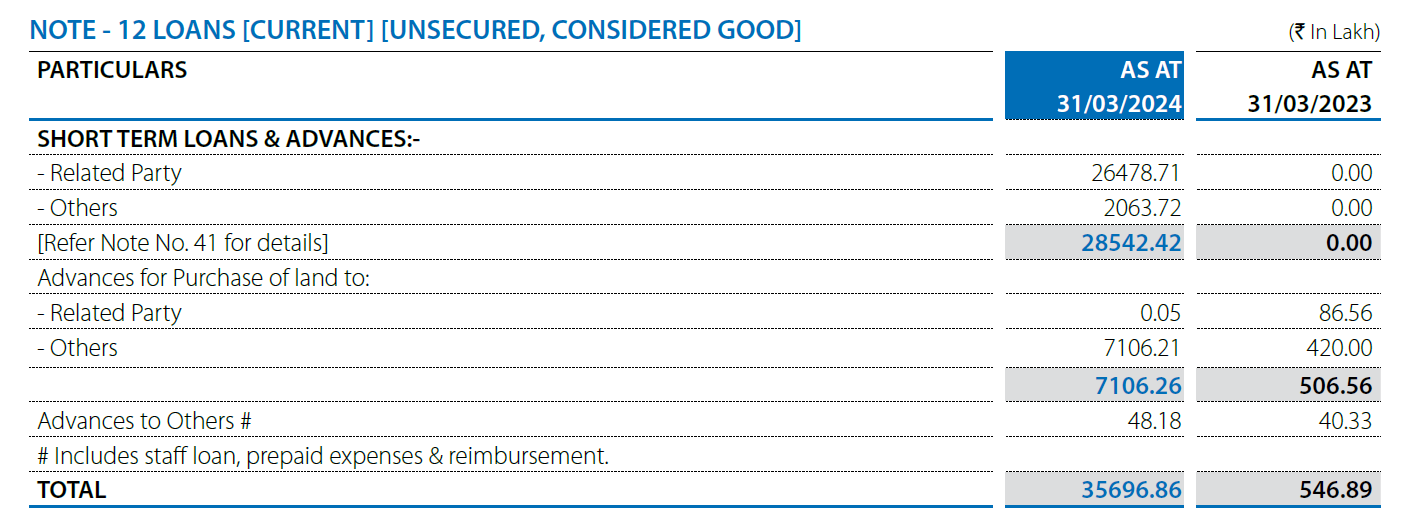

There is a lot of movement in advances to related and other parties for business. Is this normal in real estate business?

FY 21-22 AR

FY 22-23 AR

FY 23-24 AR

From concall dated 17th jan 2025, they sold 25 acres of land at approx cost of 9 crs per acre. They hold 535 acers of land. approx land bank value is 5000 crs