Ganesh Benzoplast is an interesting company. It was decimated in 2000 with series of negative events which included business downturn along with earthquake. The company was then loaded with huge debt along with almost no profitability for more than decade, and it took long time and constant discussions with creditors to come out of the mess.

After 15 years of this shock, from 2016 , we can see few positive things and profitability returning back. Company operates in niche chemical storage with continuous utilization of its tanks and assured rentals, it is clocking 60-70 Cr PAT since last few years.

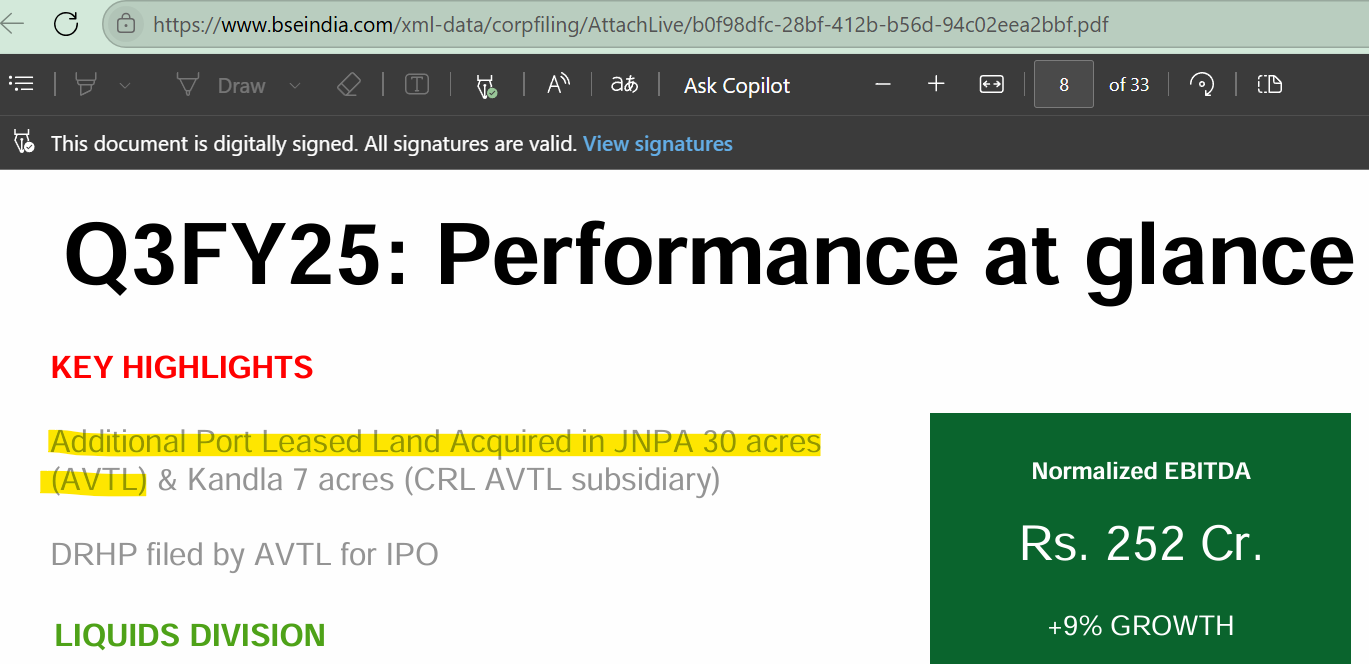

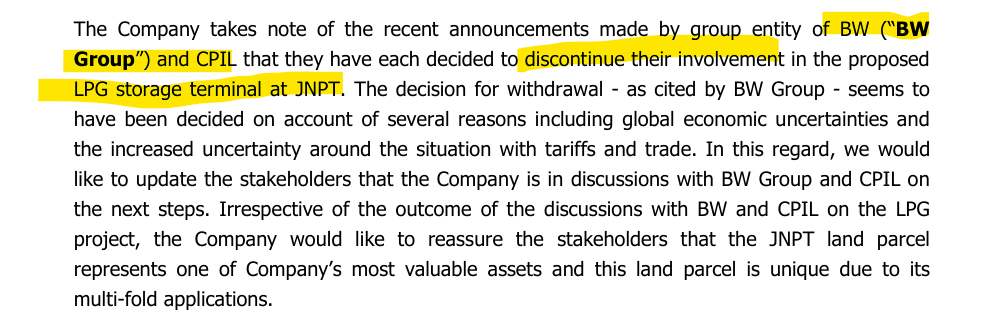

The next growth trigger is LPG setup which may multiply profitability by 3-4X. The CAPEX, that company can implement with 1:1 Debt to Equity, and the modest valuations 13 PE, the company looks good bet.

Few respectable investors are already invested - Anil Kumar Goel and Malabar fund.

However, the major problems as an investor (FOR ME) are the negative surprises that company continue to provide in the form of money siphoning by the CEO (recent event) or past contingent liabilities that turn out to be much larger in materiality when finally settled. Something looks fishy all the time (to ME). There’s never just one Cockroch in the kitchen.

The minor problems off course include is:

- Capex increments - 850 Cr (Last figure quoted by management, they continue to increase by 100 Cr every year)

- Timeline of Capex , which also keeps getting extended (that’s the nature of the game, Capex generally overshoot estimates both in timeline and in budget)

Above (the major problems) just does not gives me comfort to deploy capital, which is a personal bias, and I may miss a 10X opportunity for it.

But I can live with it, I have missed many multibagger in the past, I can afford to miss one more. What I cannot afford is investing in something, where I don’t get comfort and confidence in management, which will continue to eat my mindshare after investing.

These are my views today, I reserve the right to change them tomorrow