market takes time to get over such corporate governance issues. but if performance of company is good then mkt make again take a liking. one example if J Kumar infra … was languishing due to corporate governance issues in the past and then it went up 3 times in last 2 years (also because the sector did well).

yes completely agree, in fact the earlier civil suit filed by the company on one of the promoters was a big-big red flag per me & as a result, although Aegis logistics became 2X from that particular event, Ganesh Benzoplast reduced by more than 25% & these types of events definitely reduces the confidence on the management team.

Therefore, the latest concall will be very important for the shareholders as well as the company to give a better commentary & explanation surrounding this Saga.

4 Likes

Concall seems to be on 6th June 4 pm ?

Ya my bad😅 its on 6th june

1 Like

Ganesh Benzoplast Q4 F24 con-call

Chemical sector for coming financial year => Strong demand in market for our product; looking at optimizing purchases and we can hope to improve performance in our chemical business

Change in management for chemical division => Ramesh Punjabi will be leading the chemical business been there with us for more than 30 years, he is Chemical Eng from IIT-B

Change in approval system for payments and communication with Banks

One of the party has already waived all its claim against the company (total 7-8 parties)

2*30tonns plant yet to get approval and we will get the same soon since the elections are now over; we will start building it after monsoon

Ramakant and Raunak resigned and their family as a whole owns only 1% of the company

Major revamping of the tank done this qtr

Kochi Terminal IOC L1 to handle ATF and Ethanol

LPG Tank expansion

Approval process should complete by July and August

Most of the design work has already been done

There will be no major milestone as such it will just take about 2 years for the whole project to complete

3 parties involved to de-risk the project

Competition coming in JNPT (Aegis) => The land that we are sitting on has very much lesser price than what new player is coming in; our assets are already built so we are naturally more competitve and our tanks can hold class A,B, and C products and hazardous and has rail movement which Aegis does not has

Througput this year was only 1404 but the revenue was still higher mainly due to better product mix

LPG Tank => Capex around INR 700Cr; EBITDA Margin around 80% and Revenue at 1 throughput to be around INR 70-80Cr and 3 throughput is normal

Chemical business at 75% utilization currently

In last 2qs there were some issues due to freight cost and Nigerian currency (20% of our deemed export is in Nigeria); this problem will get resolved in coming 2 qtrs and utilization we will achieve 90-95%

Chemical growth foracsted at 10%-15%

Update on Mangalore port => Technical issue with land allotment and bid timeline was overdue, we are working with the port authorities what can be done now about it

Liquid terminal requires regular maintenance like this qtr we did in JNPT

This year maintenance capex of around INR 20-22Cr last year it was INR 15-17Cr

Other income includes collection of warfage and rent on bhealf of JM Bakshi (hardly 4%-5% margin on this warfage collection)

Liquid terminal => 60% hazardous and 40% non-hazardous

7 Likes

Based on the concall answers to you, the company is taking appropriate actions to avoid these CG issues in future and the company is on track to deliver their promises made. Once again please post your views sir.

Disclosure:Invested from CMP:89 in view of demerger.

3 Likes

Hey, I personally feel the corporate governance issues have been discounted now & given the sheer price run up in aegis logistics during the same period when Ganesh went down due to corp governance issues, I feel it looks really interesting from here.

Key points to track will be the possible realizations of the contingent liabilities & how well they clean up this issue.

Another key point to track will be the completion of capex as management believes that will get executed by FY27 & although they are guiding for EBITDA margins of 80%+, I am pretty skeptical about the same.

Disclosure : holding from Rs145 levels & added at Rs.128

Given the major revenue growth is expected to come 2-3 years down the line, I was planning to adopt an SIP based investing strategy however given the recent fall, it gave a good entry point where marquee investors are putting money at Rs.165-170 levels.

8 Likes

Hi Dhruv,

Could you help me with the throughput calc for the LPG business. I think I am missing something.

Per throughput, the rev can be 70-80Cr. BW has guaranteed 1200Cr. over 15 years, thats 80Cr. per year. So does that mean BW has guaranteed only one throughput per year.

Co. estimates 3 throughputs per month, hence 36 throughputs per year. Then the revenue should be 70x36=2520Cr. No?

Further, Aegis does 80 throughput, GBL once said that 70 throughputs is possible.

Now assuming 2520Cr. is the revenue earned by the JV, then GBL’s revenue share will be 45%, i.e 1134Cr.

Could you please help clear the clouds, I know I have made some mistake in understanding.

Thanks!

they meant 1 throughput per month will mean 70-80cr annual revenue which basically means that revenue per throughput is 70-80/12 - they are expecting 3 throughputs a month and revenue close to 200cr annually while industry does much higher throughputs

1 Like

Thanks @PranayKhandelwal appreciate the clarification.

That means @ 75Cr. approx. 6.25Cr/throughput is the revenue and assuming either 3 or 6 throughputs per month they could make 225Cr or 450Cr per year.

Since they have assumed 3 tp per month, that is 225Cr which they are roughly saying 200Cr.

But this is the revenue at the JV company, so GBL gets revenue of 100Cr assuming 45% economic interest. Correct?

yeah, that seems right

Came across this nuvama report, a bit dated. I would expect that the FY 27 estimated revenue and profits will come in Fy28, as the project is scheduled to go live in Q1 of FY27, so FY27 wont have full year of revenues and there could be delays in commissioning…hence expect the LPG project to have a full years revenue in FY28.

1 Like

while company is into high growth business corporate governance issues can be a major deterrent for investors. With promoter holding at around 40% it adds to the discomfort.

further in promoters there are many promoter groups with small shareholding… is it good or bad?

Personally I have no issues with their promoter groups shareholding structure as well as their % shareholding in the company.

Corporate governance is something one cannot be 100% sure. We recently had an issue, however in that the main promoters do not have any involvement (its the uncle who did it and he is out)…this is what is being told.

Further there is another belief I have, BW which is globally big player in the LPG sector decided to join hand with GBL. For them India is a big market where they want to do serious business and they have committed to a project by part equity and also debt which the JV will take and assuring revenues for the JV such that the debt is taken care of. Now, GBL was a very good candidate for them because they had the land at JNPT so GBL is like a very preferred choice for BW. Having said that, I would expect that BW would have done a thorough financial, legal, tax due diligence on GBL. Also Malabar and Anil Goel participated in the fund raise, so even they would have done due diligence at their end. This is not to say that promoters of GBL cannot indulge in wrongdoing going forward, but for now nothing points otherwise.

9 Likes

Ganesh Benzoplast keeps surprising regularly, now they had the fraud issue and again increased LPG capex costs to 700-750 cr. They had started with LPG capex costs of 400-450 cr. in FY23Q3, increased it to 500 cr. in FY24Q1, 550-600 cr. in December 2023, 650-700 cr. in FY24Q3, and now 700-750 cr. This is the reverse of how Aegis operates. Concall notes below.

FY24Q4

-

Issue of unauthorized bank account and loans

-

Funds were routed into an account that company and its directors didn’t know about, believe that company has indemnification from this issue, wont have any financial repercussions

-

One of the 7-8 parties have waived its claim

-

Ramakant Pilani and his son resigned from the board, they hold ~1% in the company

-

Have changed payment approval systems in terms of the limits for how much are authorized

-

-

Throughput reduced from 1.66 mn MT to 1.4 mn MT, they changed product mix which contributed to revenue increase. Will continue to improve margins via product mix change

-

60-65% of products handled are hazardous (higher margin) and 30-35% are non-hazardous

-

LPG terminal will cost 700-750 cr. (increased from 650-700 cr. earlier)

-

Aegis competition in JNPT: Ganesh Benzo has lower cost land + Ganesh is the only one to have access to railway evacuation

-

Have faced land allotment issues in Mangalore

-

Annual maintenance capex is 12-15 cr. (will be higher at 20 cr. in FY25)

-

Other income of 15 cr. was from wharfage income (4-5% margin only)

-

Chemical

-

75% utilization which should ramp up to 95% in FY25 (10-15% growth expected)

-

Ramesh Punjabi has taken over this division (chemical engineer from IIT Mumbai with 30-years in the group)

-

Faced issues due to currency depreciation in Nigeria (~20% of their sales) + red sea issues

-

Disclosure: Not invested (no transactions in last-30 days)

12 Likes

The increase in Capex cost from Q1FY24 to Q3FY24 was due to increase in planned capacity (reason gave by management) - not sure why they increased it again in Q4

1 Like

Q1 concall notes, growth will remain muted until their LPG unit commercializes in FY27.

FY25Q1

- Reason for revenue decline (but profits being maintained): EPC and wharfage business declined, these are not very profitable. Wharfage collection is offered as a service to customers and is done on pass through basis

- Chemicals: expect growth from Q3 and FY25 sales to grow by 8-10%, 8-9% EBITDA and 6% PAT margin. Exploring new products (methyl benzoate, derivatives of lube oil additives)

- Operating at full utilizations across ports, growth will be 7-8% based on rental price increase (taken in April). Expect approval in JNPT to build new tanks

- JNPT LPG: Expected commercialization in October 2026 (capacity: 64,000 MTPA) at one go (and not in phases) and will cost 700-750 cr.

Disclosure: Not invested (no transactions in last-30 days)

12 Likes

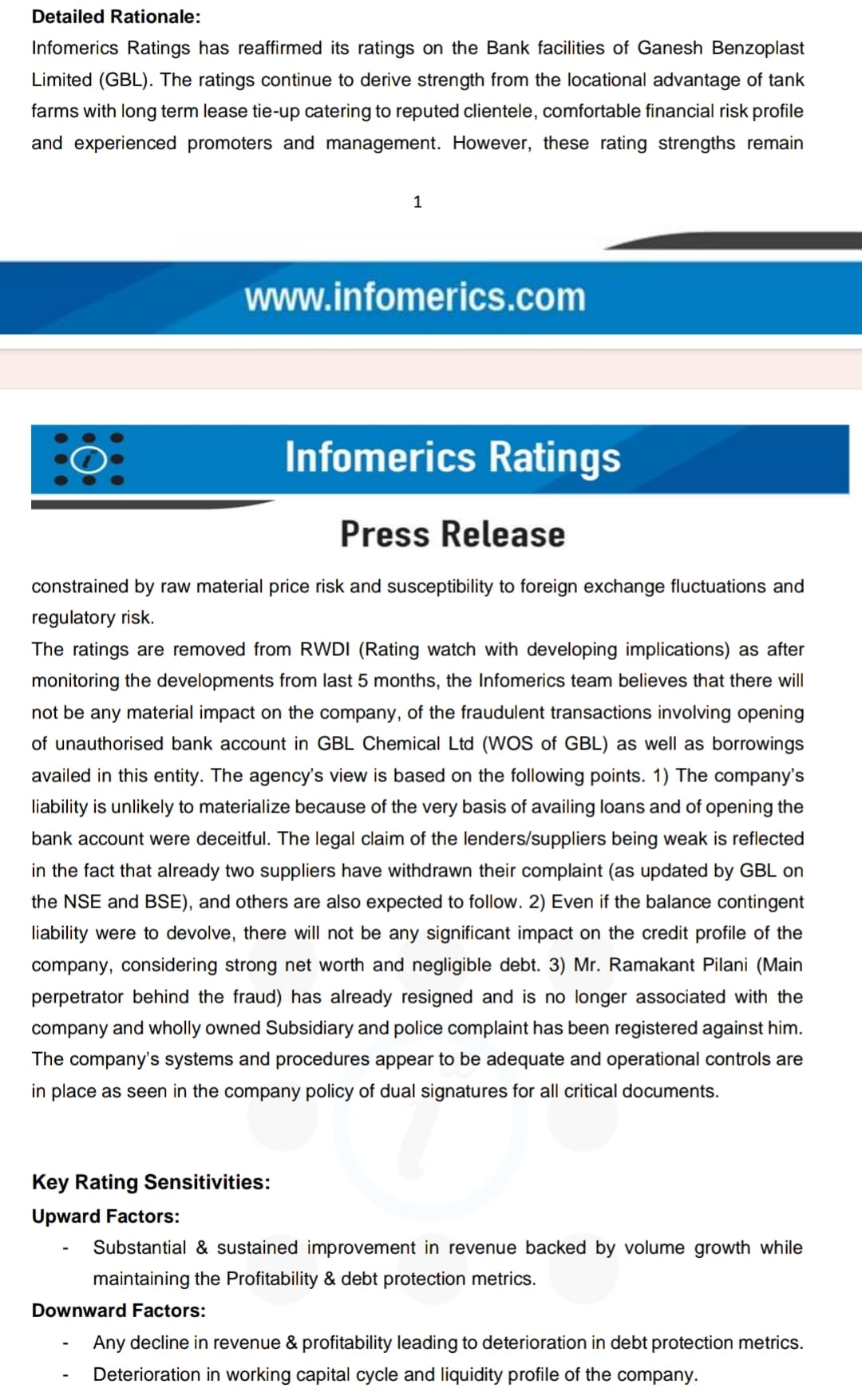

The credit ratings have been withdrawn from watching development & agency is confident about the recent fraud issue being immaterial~

(Disc: Tracking position)

2 Likes

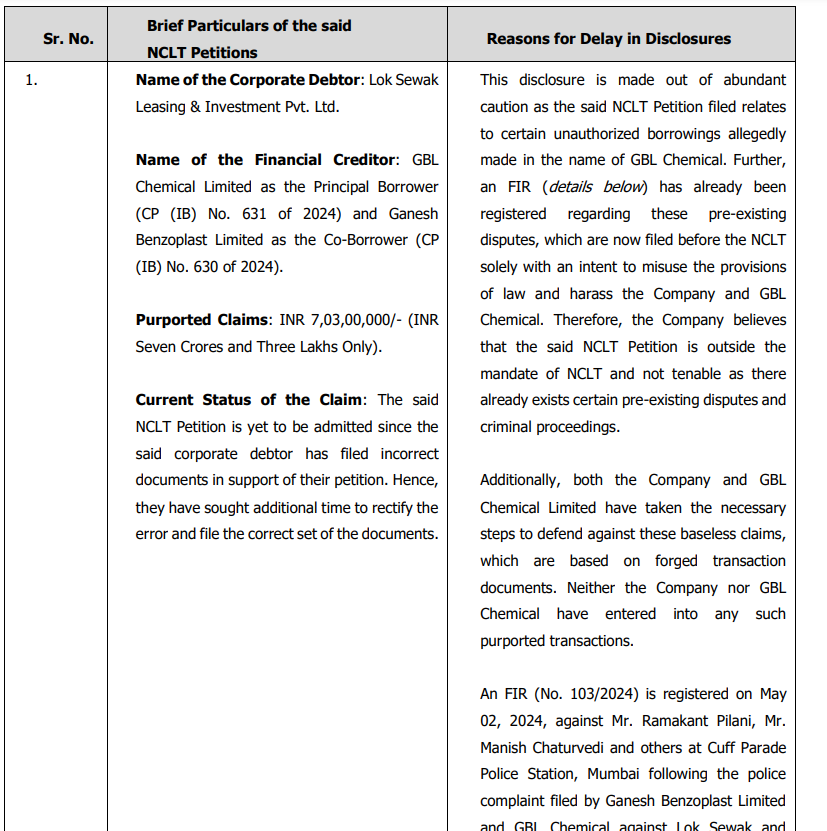

Major hit to the company- Creditors of the Chemical division have dragged the company into NCLT as a result of the recent fraud case~

Core operations should remain un-disrupted as a result of chemical segment being under a separate subsidiary.

6 Likes

Interesting View on Ganesh Benzoplast. https://youtu.be/nsVqc1Ucqq8

1 Like