12 posts were merged into an existing topic: Gallantt Ispat - Steel producer DRI route

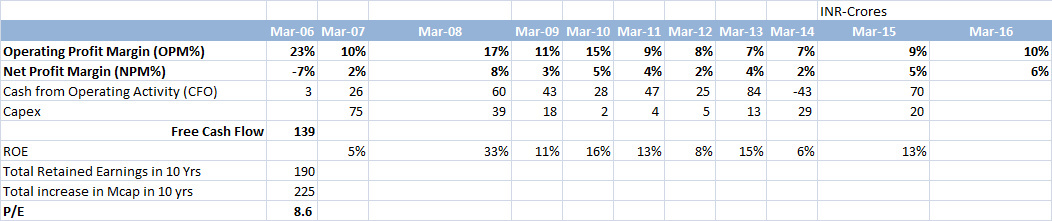

Source:Google Finance

Gallantt Metal Limited is an India-based company, which is engaged in the business of production of iron, steel and power. The Company operates through two segments: Steel and Power. The Company manufactures and produces various kinds of iron and steel products, such as sponge iron, pig iron, cast iron, bars, rods and billets. Billet is a semi-finished product, which is used for feedstock to rolling mills for production of long products, such as wire rods, bars/rods and structural. Steel Billet is also used in forge shops and machine shops for production of engineering goods and as feedstock for tubes. The product portfolio for the food grain business includes wheat flour products, such as atta, maida, suji and bran. Its products are sold across northern markets, including Uttar Pradesh, Bihar and West Bengal under the brand name of Gallantt. It has an integrated steel plant at Taluka Bachau, Kutch, Gujrat. The Company also has a captive power plant of approximately 25 megawatts (MW).

The Company looks fundamentally strong based on Fundamental Numbers and Valuation is very attractive,Will do more research and would be back with more details.

However i see a Positive breakout of the stock price,which may give positive returns atleast in the short run.

Disc:Not Invested

Gallant Metal holds 26% in Gallant Ispat, the market value of which is more than 400 cr. Also, 25 mw power plant is worth min 125-150 cr. Company is almost debt-free. They are making nominal losses in TMT biz. But overall profitable due to surplus power. Any upturn in steel sector should be very beneficial of them.

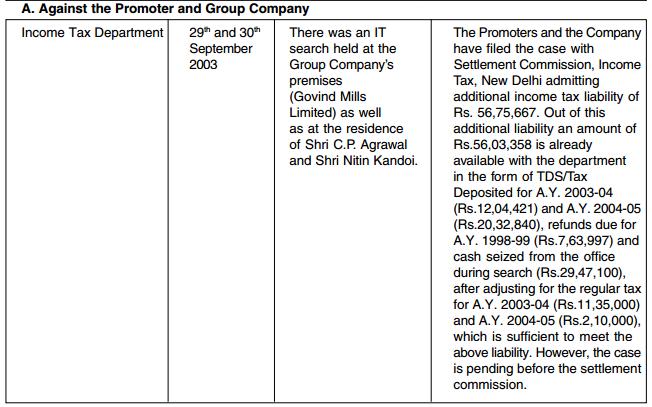

Risk : Nothing much known about the promoters. Any input on this will be appreciated.

Disc: Am invested.

-Jiten Parmar

Source - Prospectus 10 years old…

Poor Q1 results. Sales and NP both are down. Steel cycle still has not picked up.

-Jiten Parmar

This is an interesting company.The promoters have been increasing their shareholding for a while now.51 percent in 2014 to 62 percent in 2017

The management is not earning much as salary .About 68 lakh and not receiving any dividend.How are they increasing their shareholding?

The group continues to post excellent results for last few qtrs - https://www.bseindia.com/xml-data/corpfiling/AttachLive/4b4ca92c-61b9-4555-bc38-2627f6f53bde.pdf

As per the annual report, they also have plans to increase the capacity.

Infact the whole of the steel pack continues to do well while the valuations have remained low (on PE basis). Is it an opportunity or market is smart in preempting the top for the steel cycle?

If you see the overall sales from the FY 13 to FY17, TOI has stayed almost constant. Any specific reason for that? FY18 has seen good growth in all quarters but 5 years stalemate needs some explanation.

FY21 Q2 Updates:

• Approval for amalgamation is not received yet from SEBI

• Company revenue back to almost 80% pre-covid level

• Expansion is not completed yet and on seeing CWIP about 260 crores seems company still building its capacity

• Dip in inventories of about 50 Crores. For very long time company maintained inventories of about 100-120 crores.

• Receivables and payable are stable

• Reduction of 30 crores in borrowings, but I guess company will borrow some amount in near future

Good set of results plus capacity expansion from April 2021 onwards. This can give further boost to their revenue and PAT

Discl - invested

Most of cwip are now part of netblock👍. Gallant ispat has some left. Sooner its going to be gallant limited after merger.

Topic Closed.

Recently Gallant Ispat is amalgamated into Gallant Metals and name of Gallant Metals is changed to Gallant Ispat. Please follow at Gallant Ispat thread

Thanks @Sidharth_Chandraseka for the prompt