Hi everyone,

FEL (Future Enterprises) & FRL (Future Retail) were demerged some months ago.

Everyone knows FRL is the Retail business of the Future Group but a very few people understand FEL.

FEL basically has 2 standalone operating divisions : A) Lease rental biz. B) Manufacturing biz. They do the above businesses as a back end operation for FRL itself. Hence, they have solid & long term earnings.

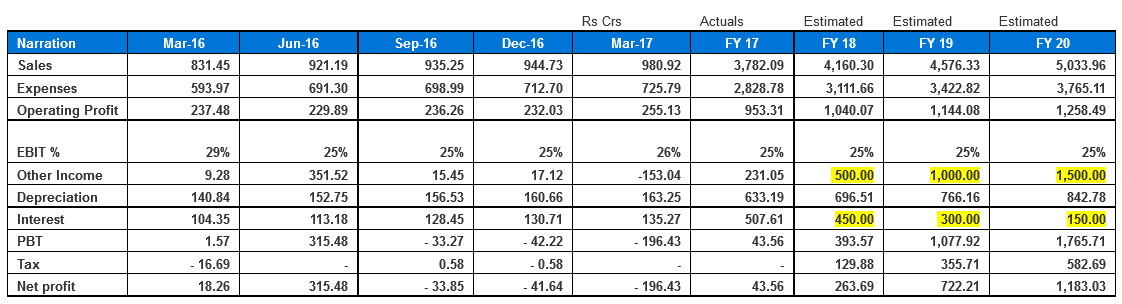

Its interesting to note that FEL has done FY17 EBITDA of 1000cr rupees. Hence we have a strong core standalone business here. (Mkt cap is just 1400cr).

They also have debt of 5000cr approximately. This number sounds scary.

But here is the interesting thing - They have assets on their books which are currently valued at 5000cr too. Some of these are absolutely crown jewel assets such as stakes in Future Generali Insurance, Future Supply Chain (IPO expected this year according to Mr.Biyani), Prime mill land in the heart of Mumbai - Apollo & Goldmohar mills and some other stakes. A conservative valuation of the above assets on FEL books is 5000cr rupees.

*The management has indicated at the time of demerger that they plan to demerge all these assets in the coming quarters and make FEL a debt free company.

Valuations are very interesting:

Market cap of the company is about 1400cr. Debt is 5000cr. So, we have approx 6400cr EV.

We have FY17 Ebitda of 1000cr. Hence, we have EV/EBITDA of 6.4x on trailing numbers.

Now, if we believe that the management sells all their stakes as guided, we are going to have a debt free company and essentially have an ‘Adjusted EV/EBITDA’ of 1400/1000 = 1.4x.

*I have double and triple checked my numbers. FY17 reported EBITDA is 1000cr and this is rock solid and sustainable income because they are contracted through lease rentals and manufacturing for Future Group companies.

The company also has scary looking debt but its all entirely Long Term Debt via NCDs maturing after 5-6 years. The bonds too are trading above par. (Bond market thinks that the debt position is solid).

Forget everything else, the current trailing EV/EBITDA is 6.4x. That in itself deserves a 8-10x multiple due to the robustness of the income.

Also, according to me, their Future Generali & the Future Supply Chain businesses are doing very well and growing. With GST, the Supply Chain IPO will also be very strong.

The Apollo & Goldmohar mill land are absolutely coveted assets too. Their value has also risen since FY16 valuation.

Theoretically, if we assume the debt is canceled out by the investment sales, we will have a standalone company with 1000cr trailing ebitda and 1400cr market cap (debt free). Also to note is that, the standalone business is growing too.

Any feedback on my thesis will be very appreciated. If I am wrong in my thinking, please let me know. I have studied this over and over and I am baffled.

Disc- I own this stock.

S.I