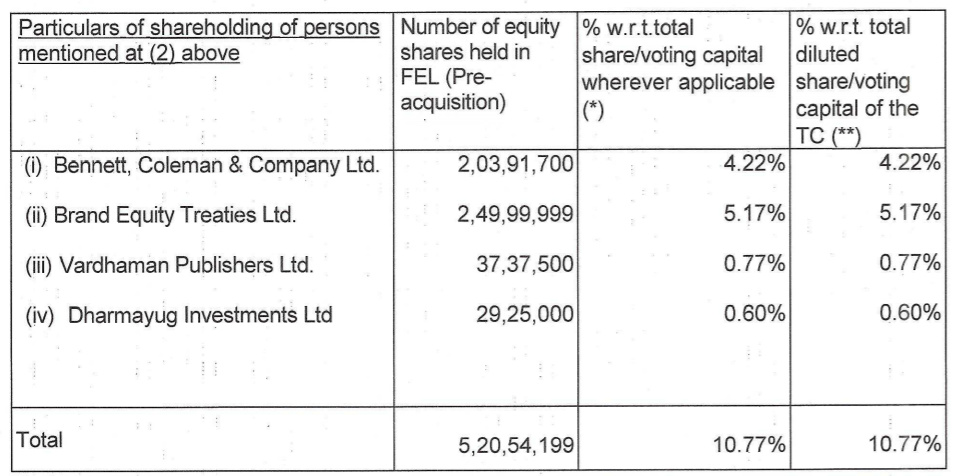

Wow, I think the moves have just started in FEL - Mr. Biyani has given a BSE Notice that he has bought 4 cr worth shares in FEL recently. This obviously speaks volumes and shows how aligned his interests are.

With light of the upcoming Future Supply chain IPO this stocks perhaps looks as good as it did a year ago (the investments have done so well).

People forget that the underlying investments have really appreciated in value since then because of demonitisation and GST as huge tailwinds (Insurance and Supply Chain respectively).

Mr. Biyani seems to acting in the best interests of the company - selling Future Consumer for 500 cr, Future Lifestyle and now the FSC IPO. Then has bought some stock and finally if you look at the AGM resolutions he seems to be broadening the scope of the company - by making this a sourcing co for the group (pls take a look at them). So it really looks like the promoters want to make this a real company.

If we look at the financials of the company:-

1150 cr EBITDA in FY17

this should grow comfortably in FY18 because of the space additions in the Future Group and the expanded scope of operations, I think it will comfortably be more than 15%.

As interesting is the EV.

As of today the Market Cap is 2300 CR

Debt is 5000 CR (March 2017)

Total EV: 7300 CR

Now FEL has sold 480 cr worth Future consumer post the last balance sheet, so we can reduce the EV by 500 cr.

Then there is:-

a 50% holding in Future Generali (which seems to be on sale according to media reports).

Valuing that at (a fair) 1.8x GWP which is a decent discount to other comparable deals.

That gives a value of approx 1700 cr

a holding in Generali Life:-

Unlike General this is not profitable and seems to be much smaller. Yet, with decent growth it is not a bad asset. The last deal was done @ 1550 crore in 2013. With the serious growth + multiple re-rating in the life business since then I think we can safely say it would be worth conservatively 2000 cr (which is fair on an embedded value multiple too)

so their 27% stake would be valued at around 550 cr

Then there is the FSC stake. A 60% stake in a growing business that will be listing soon - this is definitely the joker in the pack as we do not know what it will list at. Assuming it lists at 3000 cr, the stake is worth 1800 cr

If we look at the total of the FCON stake sale + the investments (I’m not applying a holdco discount as FEL very clearly states that they have a monitisation plan for this, unlike a holdco which doesn’t do anything for years…) the Enterprise Value comes to:-

Market Cap (2400 cr)

Debt (4000 cr)

(-) future consumer sale + the holdings

The enterprise value comes to around 2850 cr

If we divide this by the EBITDA calculations from the beginning we get an EV/EBITDA of around 2.1x

However poor the quality of the business is there is if one atleast gives a 5x multiple to this (20% yield!) - there looks like there is something left on the table for us investors.

Disclosure: Entered recently.