thanks for the detail

1 Like

Can anyone share the breakdown as to which customers are contributing how much to the revenues of the company. I am not able to find that information myself.

Additionally, what are your views on the low profit margins of the company? There are several other key risks associated with the business. Will share it soon.

Thanks

Disclaimer: Not Invested

Main points of the article about DFC:

- 50% lower rate for transport

- 3x Faster speed

- More capacity obviously, “70% of the freight trains will be transferred on the DFCCIL network”

All this will increase demand for railway wagons (and free capacity to run more passenger trains also), which will need more bogie springs, some made by Frontier. Wait has been quite long and will take a year or more to operations.

One of the reasons I do not touch CV stocks, at least not for long term.

CONCOR, Titagarh could be good buys too!

2 Likes

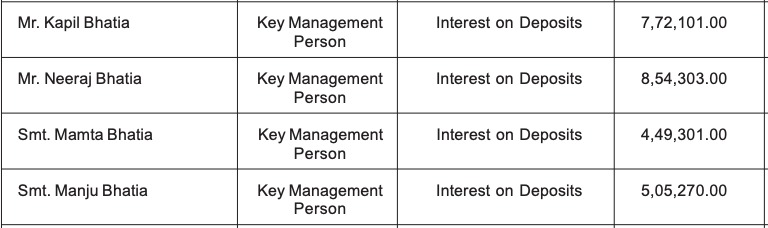

Promoter has given loan to the company and charging extremely high rates on that. Doesn’t that distort the story. After all minority shareholders are also owners in the business.

Also the salary of the promoter is high as compared to the profits.

10 Likes

With respect to deposits, total deposit amount gone down almost 85% to 29,41,297.00 (Pervious year it was 18,331,181.00). Could it be the payment also incorporate principle repayments? Though I couldn’t match exact numbers.

2 Likes

While reading their AR for 2019, MDA states as below

RISKS AND CONCERNS

In the coming decade, the main focus would be on enhancing efficiency and productivity, and on innovation

driven by changing customer demands. Price sensitivity of the Indian consumer, cost optimization needs of manufacturers and increasing focus on environmental concerns

will drive critical changes in market.

Currently, the Company perceives the following main business risks:

a) Exposed to volatility in raw material prices;

b) Pressure on selling price due to increase in competition

Does anyone has any idea as to how it is managing as compare to their peers as i was not able to get more info.

Disc - Not invested

To add to Gurjeev sir’s post - Along with earning ~20+% int on loans …

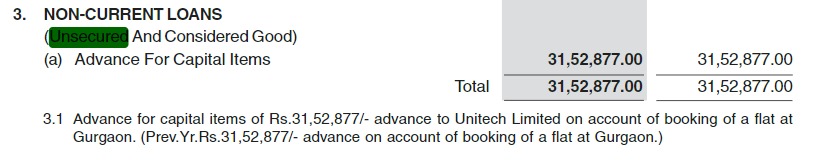

Advance for Booking an apartment to Unitech (for personal use??)

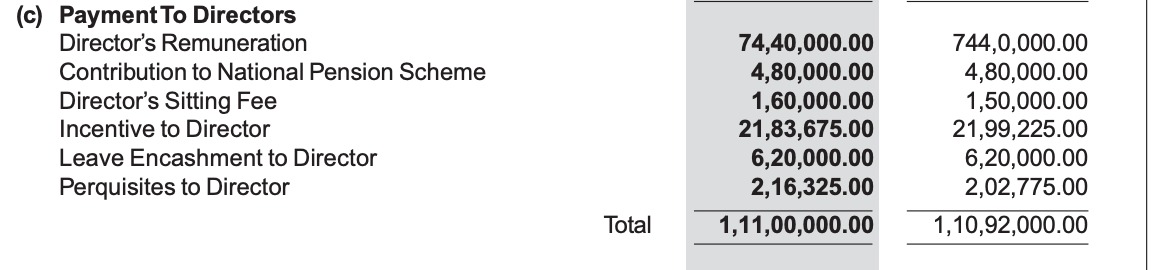

Such High Remuneration - For comparison - PAT was 8cr https://pbs.twimg.com/media/EZnouNMXgAErsxp?format=jpg&name=small

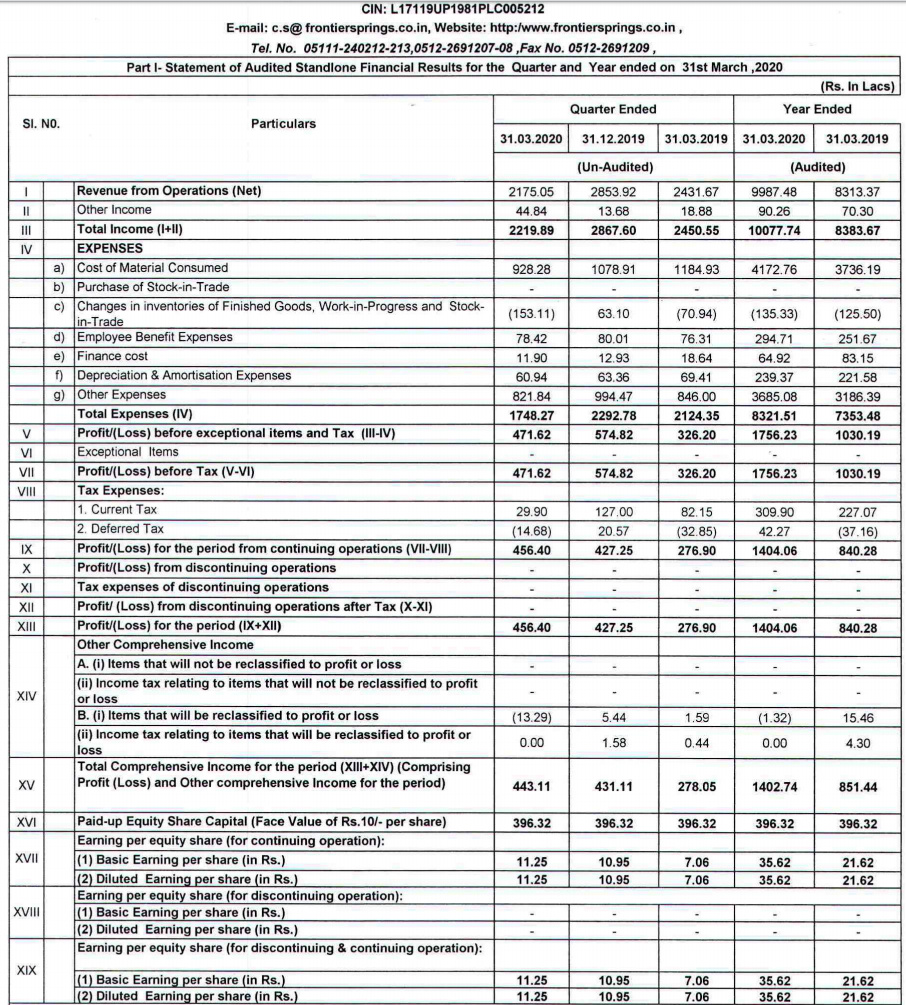

Good results for Q4 FY20, but mainly inflated by exceptionally low tax

https://www.bseindia.com/xml-data/corpfiling/AttachLive/56c10cae-1ac6-45ac-b10e-f8903052e167.pdf

Good thing is margin has improved drastically compared to previous year. CWIP of 4 cr seems to be completing this year. Company has funded expansion through internal accruals.

1 Like

Good results continue…however we need to look at Q1/Q2 results as I am hearing there is drastic budget cut in Railways.

Disc: sold my position on Friday. Was holding it for more than 2 years.

1 Like

Good news if this takes off! ~3000 coaches in ~2.5 years.

Edit: Bad math, each service will take more than one train-set, maybe 2x or 3x or more for higher frequency and longer run duration (long turnaround). But, also same train-set can be used for more than one service if low-frequency and short enough total turnaround time! So, maybe 7-8,000 coaches roughly speaking! Even if only half the list takes off, it is a big opportunity.

Union ministry of railways on Wednesday invited request for qualification (RFQ) for private participation for operation of passenger train services on over 109 pairs of routes across the country. Railways is planning to deploy 16-coach 151 modern private trains in the country by April 2023. It is expected to entail a private sector investment of about Rs 30,000 crore. Private firms will be responsible for financing, procuring, operation and maintenance of the trains. The trains will be designed for a maximum speed of 160 kmph to reduce travel time.

No existing trains will be cancelled! Now even passenger trains, (D)EMU etc. are being LHB-fied!

Disc: holding

3 Likes

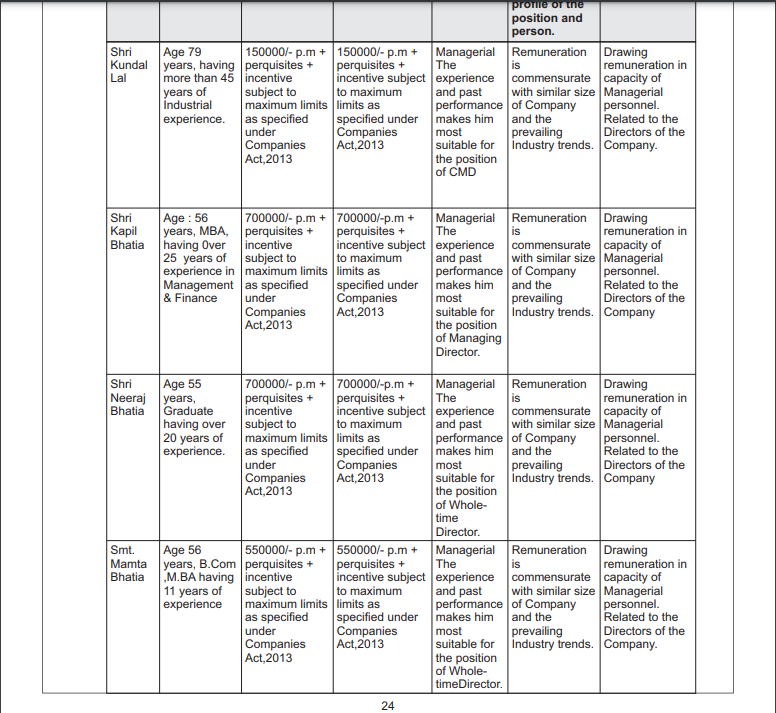

Though the numbers & biz seems good … Does Renumeration for Promoters and related party transactions looks good ? @vikas_sinha @Sneh_Kagrana

2 Likes

All numbers indicate a good business. Risk is dependance on government.

Sadly, the related party transactions seem to indicate that promoters are inclined to take cash out of the company for personal use.

Has any one questioned them ? and any answers?

1 Like

The remuneration for KMP to Net profits have been more than 30% consecutively for last 3 years. Is this normal to a business in this industry ?

3 Likes

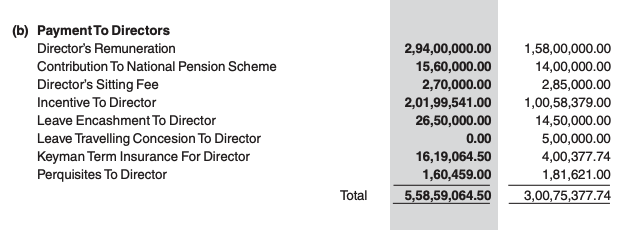

2019-20 & 2018-19 Remuneration details.

2 Likes

As per Section 197 of the Act, the total managerial remuneration payable by a public company, to its directors, including managing director, whole time director and its manager, in respect of any financial year shall not exceed 11% of the net profits of that company.

Net profits of the company stands at 14 crores. Is my understanding right. Senior folks kindly help with this.

1 Like

Sir @hitesh2710 this seems like a major turnoff for a very good looking company.

I was planning to track it more but this post has put a stop to it.

Kindly share your views in regards to this and if you track this company.

The future of railways has been painted quite beneficial for this company but for small cap companies, corporate governance is the most important thing I look to.

3 Likes

Yes…you right Rohil, i also impress with growth results but when i check remuneration for 2018 to now…each and every year promoter taking more than 70% of net profit which i believe very very bad sign…

see this in 2021 net profit 7cr but promoter remuneration is 6CR…which is not at all good…

3 Likes

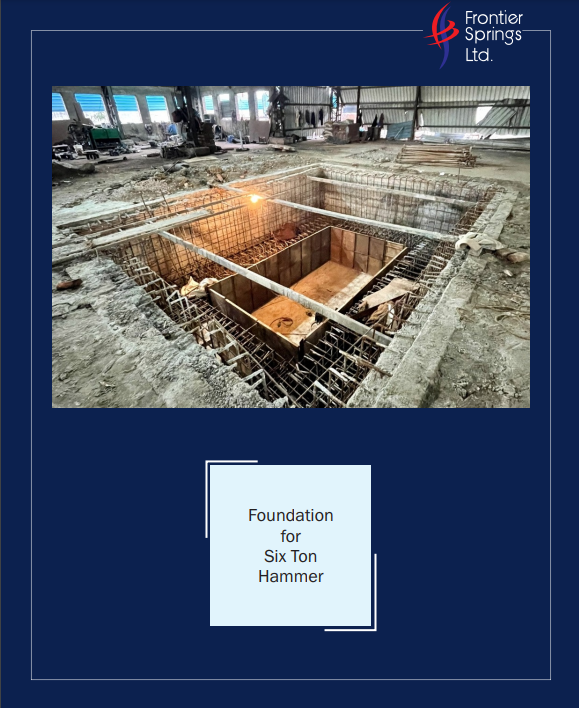

Some things that caught my eye in this years ANNUAL REPORT

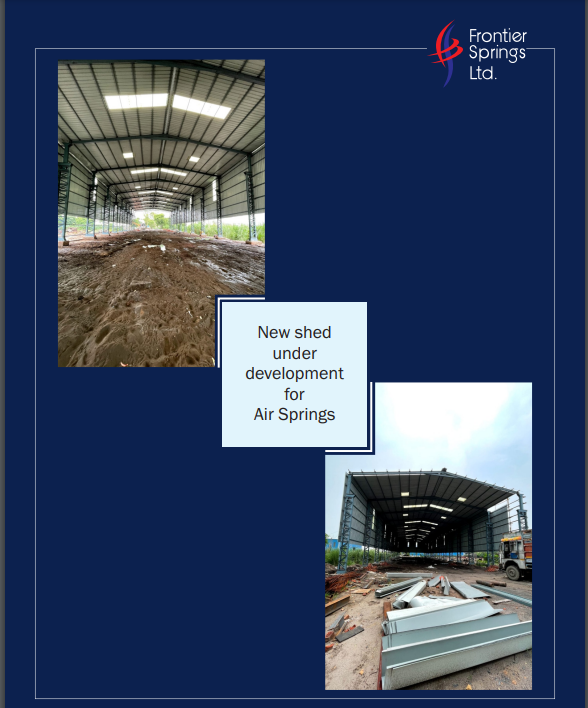

Company is moving into air springs

One of the biggest concerns was the management remuneration. This time they have not taken a hike. Obviously the results of last 2 years are also not great which could be one of the reasons but could this be a sign of change (I might be over-expecting a bit here though).

Disclosure : Invested and views may be biased

4 Likes

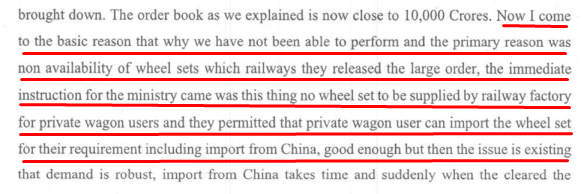

Also i was expecting good results from the company in Q1 of FY23 only but since it was not upto the mark so read the last con-call of Texmaco rail to understand what went wrong. Turned out that there was severe shortage of wheels in the quarter because of which the company was not able to execute the wagon order which was in hand. From next quarter onwards the supply of wagons should increase.

4 Likes