### Company Overview:

- Fratelli Vineyards Limited, previously Tinna Trade Limited, is one of India’s leading wine makers and the second-largest Indian wine business.

- The company was founded in 2007 in Akluj, Maharashtra, by seven brothers from three families and two countries.

- Focused on producing high-quality wines and vineyard tourism, with a commitment to quality farming.

### Business Transition:

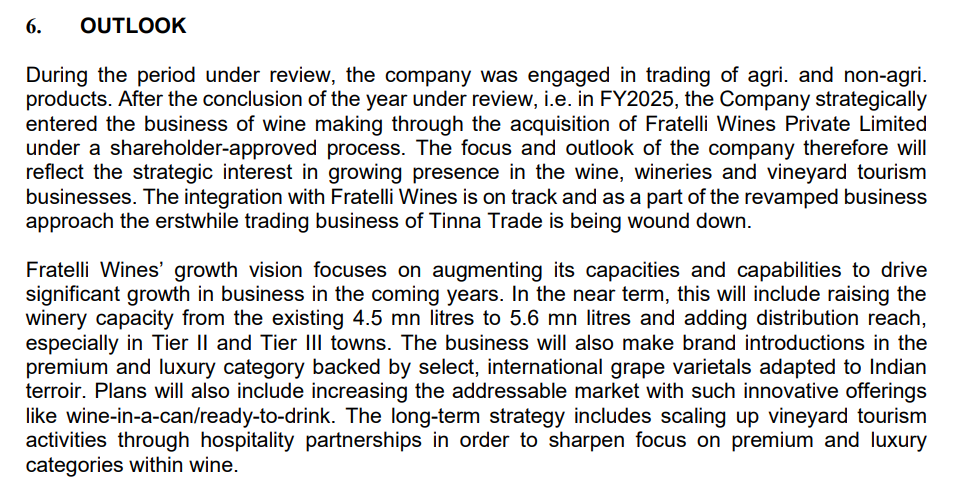

- Transitioning from a trading business to a singular focus on wine production and vineyard tourism.

- Trading activities contributed approximately ₹100 crore in revenue during Q1 FY25 but will cease by Q3 FY25.

### Strategic Performance:

- The company emphasizes the importance of the vineyard in wine production, stating, “good wine is made in the vineyards and not in the cellar.”

- Complete ownership of the grape-to-bottle value chain, which is a unique model in India.

- Strong relationships in the HoReCa (Hotel/Restaurant/Café) segment with 22,000 touch points across India.

### Financial Highlights:

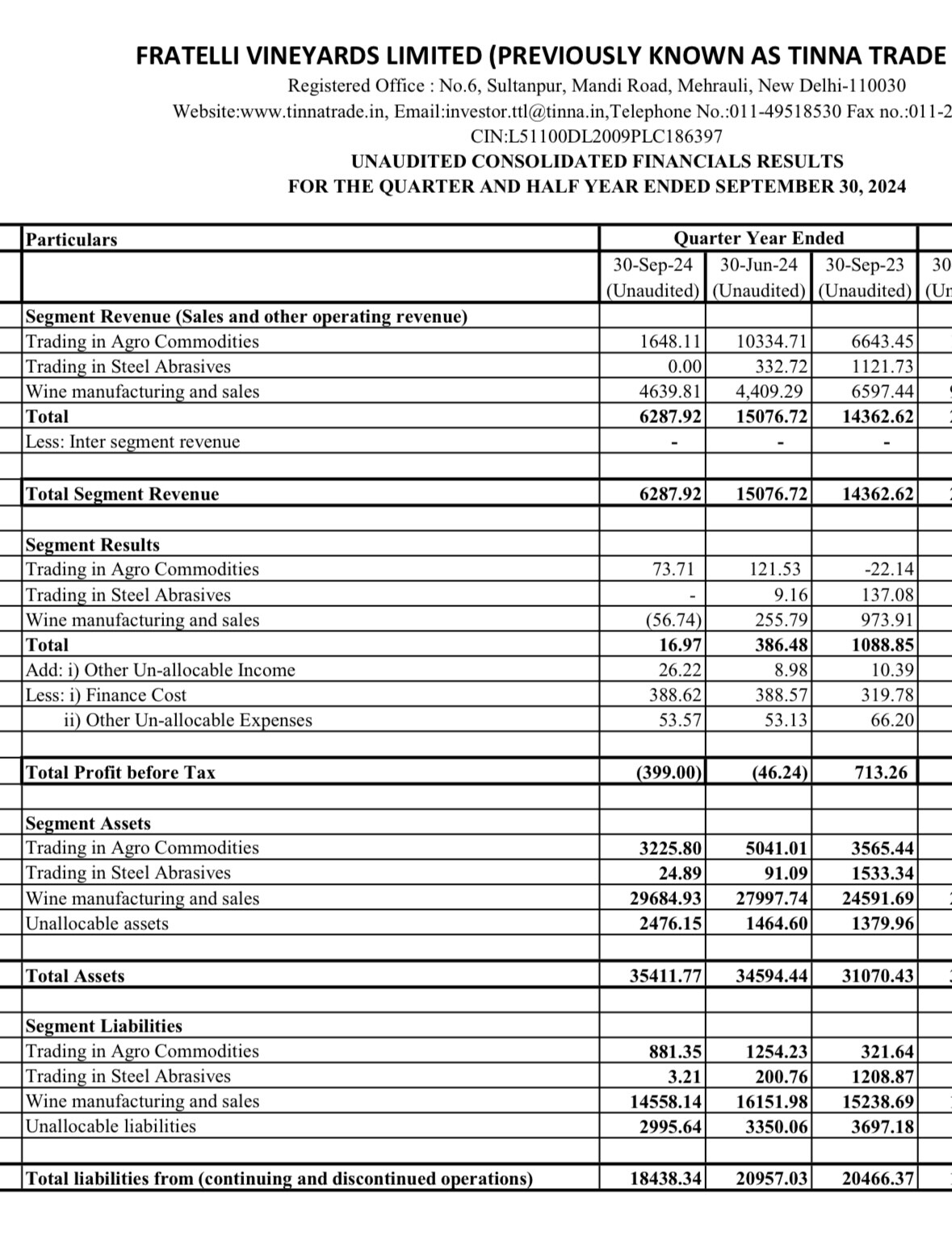

- Q1 FY25 revenues were approximately ₹45 crore, slightly down from ₹46 crore in the same quarter last year due to election-related permit challenges.

- Revenue guidance for FY25 remains above 15%.

- EBITDA margins have improved, with a current margin of ~13.5%, expected to continue an upward trend.

### Growth Strategy:

- Focus on premium and luxury segments, with a diversified portfolio ranging from luxury wines priced above ₹2,000 to value segment wines priced between ₹250-₹550.

- Plans to introduce new brands and renovate existing ones, particularly in the Super Premium and Luxury categories.

- Expansion of vineyard acreage and ramping up winery operations to support growth in premium wine production.

### Vineyard Tourism:

- Investing in a 40-key multi-use property on 170 acres at Akluj to enhance brand visibility and profitability through vineyard tourism.

- Expected occupancy rates of 40% in the first year, increasing to 60-70% in subsequent years.

- Anticipated construction costs for the hospitality project around ₹50 crore.

### Market Position and Competition:

- Currently holds a 30% market share in the Indian wine industry.

- Competing effectively against established brands like Sula and Grover Zampa by focusing on quality and brand development.

- Unique selling proposition includes the cultivation of Fratelli-owned grape clones better suited for Indian conditions.

### Challenges, Risks, and Outlook:

- Facing challenges due to natural calamities impacting crop yields; mitigating risks by acquiring land for diversified farming.

- Management remains optimistic about growth prospects, citing a robust operating model and strategic investments.

- The wine market in India is expected to grow at about 15%, with Fratelli aiming for a higher growth rate of 25% CAGR based on past performance.

Some of the risks that the Company is exposed to are:

Financial Risk;

The Company’s principal financial liabilities, other than derivatives, comprise loans and

borrowings, trade and other payables. The main purpose of these financial liabilities is to finance

the Company’s operations. The Company’s financial risk management is an integral part of how

to plan and execute its business strategies.

Foreign exchange risk

The fair value or future cash flows of a financial instrument will fluctuate because of changes in

foreign exchange rates. The Company has limited currency exposure in case of sales, purchases

and other expenses. It has natural hedge to some extent. However, beyond the natural hedge,

the risk can be measured through the net open position i.e. the difference between un-hedged

outstanding receipt and payments. The risk can be controlled by a mechanism of “Stop Loss”

which means the Company goes for hedging (forward booking) on open position when actual

exchange rate reaches a particular level as compared to transacted rate.

Commodity price risk

The Company is exposed to fluctuations in price of pulses, grains, Sunflower Meal and Crude

Degummed Soybean Oil (including fluctuations in foreign currency) arising on purchase/ sale of

the above commodities. To manage the variability in cash flows, the Company enters into derivative financial instruments to manage the risk associated with the commodity price fluctuations relating to all the highly probable forecasted transactions.

Credit risk

The risk that the counter party will not meet its obligation under a customer contract, leading to a

financial loss. Customer credit risk is managed by each business unit subject to the Company’s

established policy, procedures and control relating to customer credit risk management.

Liquidity Risk

Risk that the Company will not be able to settle or meet its obligations on time or at reasonable

price. The Company’s objective is to at all times maintain optimum levels of liquidity to meet its

cash and liquidity requirements. The Company closely monitors its liquidity position and deploys

a robust cash management system.

Equity Price Risk

The Company’s listed and non-listed equity securities are susceptible to market price risk arising

from uncertainties about future values of the investment securities.

Political and economic environment

Any changes in political and economic scenario of the country will impact the business of the

company. Change in government policies may adversely impact the business of the company.

Regulatory Risks

The Company is exposed to risks attached to various statutes, laws and regulations. The

Company is mitigating these risks through regular review of legal compliances carried out through

internal as well as external compliance audits. The Company has implemented an enterprise-wide compliance management system,

### Innovations and New Products:

- Recently launched Pinot Noir and renovated the Master Selection range.

- Plans for further innovations and product launches to cater to diverse consumer segments.

### Margin Guidance:

- Currently experiencing EBITDA margins of 10%-12%, with an expectation of gradual improvement.

- Focused on maintaining a steady stream of premium brands to sustain leadership in the market.

### Capex Plans:

- Anticipating a capital expenditure of approximately ₹30 crore for capacity expansion and brand building.

- Additional ₹5 crore planned for expanding vineyard acreage and ₹45-50 crore for the hospitality project.

### Export Markets:

- Currently, exports contribute less than 3% to overall revenue, but there is a plan for a 20% increase in exports this year.

- Focus remains primarily on building the domestic market, with exports to about 10 countries.

### Conclusion:

- Fratelli Vineyards is positioned for growth with a strong focus on premiumization, vineyard tourism, and innovation in product offerings. Management is optimistic about the future, backed by a solid growth strategy and market positioning.

Disc: Invested, bullish and therefore biased