please help me understand this…

Should we calculate a weighted average acquisition price and see if the CMP is less than the acquisition price?

1 Like

I don’t think they can achieve Sula’s margin as Sula has higher margins due to hospitality sector.

Anyone still tracking this company? The stock is getting continuously hammered.

I think the agro commodities trading business is closed and the last quarter results were only Wine and Hospitality business. need to wait for this year`s annual report for restated financials.

last equity dilution was at 180 rs through warrants. so let us take as a good anchor ![]()

For 9 months of FY24-25, they reported revenue of Rs 150Cr from the wine business. Agro commodity business is closed now.

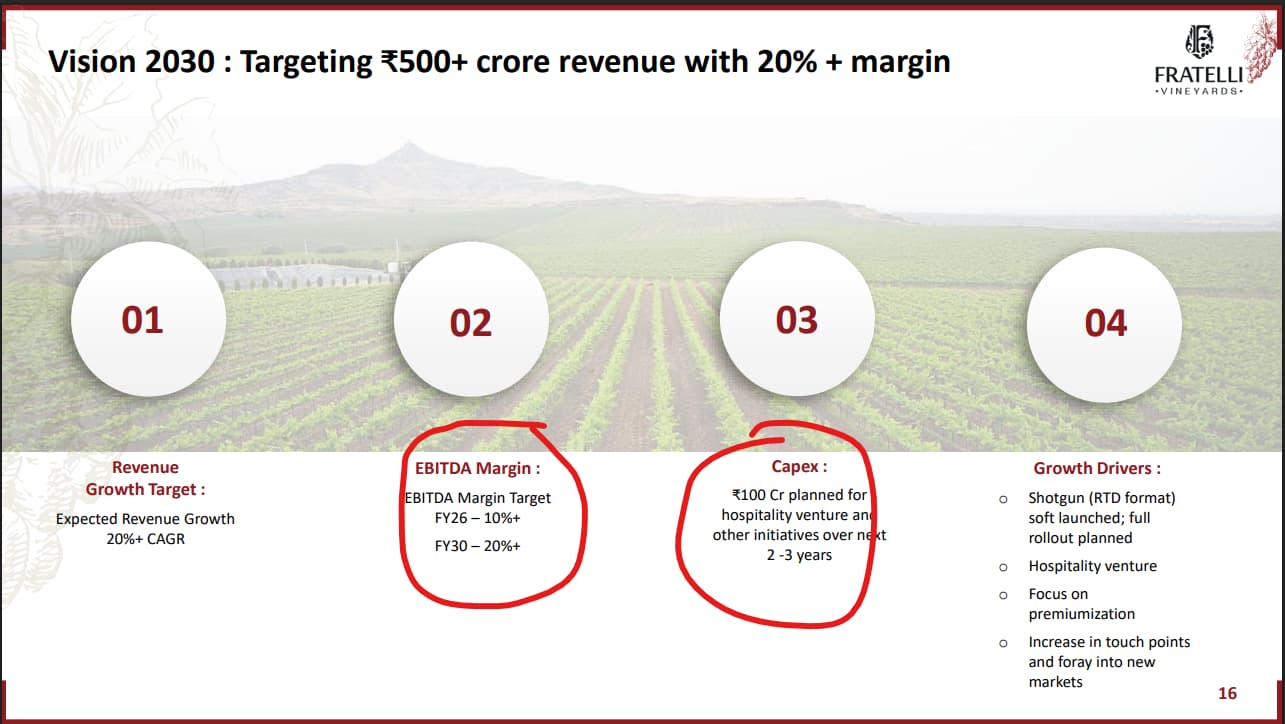

EBITDA margin has taken a hit compared to previous years where it was in the range of 13-16%. The management is taking brand building and category development initiatives. These are currently around 12% of revenue and expected to stabilise around 7% of revenues in FY25-26

Company looks attractive at the current valuation of 600Cr having 30% market share and a strong moat

Disc - Invested

4 Likes

Curious, the same company was at mcap of around 100 cr less than 2 years back…was the moat same then or it developed any in last couple years?

1 Like

Earlier this company was named Tinna Trade Ltd and was into trading business. Fratelli Wines was acquired and made a subsidiary by way of share swap last year.

So comparing market cap 2 years back wouldn’t be justified since Fratelli Wines wasn’t part of the listed company. Fratelli Wines on the other hand was founded in 2007 and was operating as an unlisted company

8 Likes

Their auditor and CFO have resigned over last 8-9 months. What were the reasons for that and how should one read into it?

1 Like

Bit out dated interview (Aug - 24)

From latest investor presentation - https://cdn-media.screener.in/concalls/d582555f-f5c0-466b-a1ca-7953c54dafaf.pdf

Disc: Invested and added in last 1 week.

4 Likes

from 2025 Annual report.

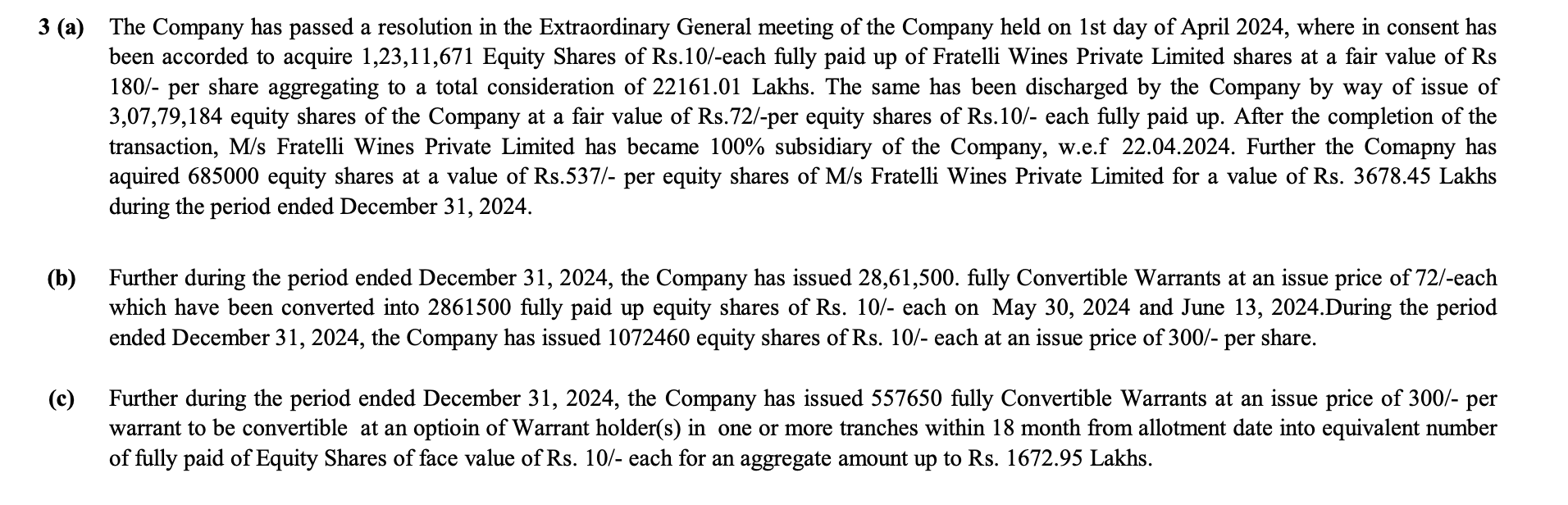

- There was a preferential allotment done at 300 Rs and promoters also participated.

- During merging of Fratelli with Tinna trade, Fratelli shareholders were allocated shares at 72 Rs - Total shares - 3,07,79,184 shares.

@pratyushmittal for some reason the book value shown in screener (36 Rs) seems to be in correct.

From AR 2025,

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2496bddf-a207-4007-b3bc-c123b4a7fd60.pdf

If one goes through the recent concalls, it looks like management wants to raise the funds to build 40 Key room resort in Akjuj.

Disc: Added in the recent fall.

6 Likes

7 Likes

Hi , Harsh vijay Could u please explain why CFO metric when it comes to business transtition

It is possible to get those annual report of the unlisted space

Happen to visit a liquor store in Bengaluru and saw that few Fratelli products were on discount.

Buy 2 Get 1 for products around 900-1000Rs

and 15% for 2000+ Rs products.

Feedback from sales people that company filling in the products more frequently compared to earlier times (6 months) and also told Sula has got more fast moving products compared to Fratelli :). With better M&A and smaller base might help Fratelli to show good sales numbers in future.

3 Likes

Filling in more frequently means sales rate has increased or they have improved their distribution, such that as soon as a few bottles are sold, they are quickly restocked (due to more regular deliveries) or both?

1 Like

Better distribution. The sales person told Sula is still the most sold brand.

1 Like

Massive action seen in the stock price in the past few sessions. Porinju Velliyath took a substantial stake. Promoter (group) are also buying continuously..

1 Like

They are burning like CRAZY. Giving discounts across all channels - Whether personal consumption or HoReCa trying to undercut Sula.

Jiofication attempt…very destructive for the industry health in my opinion.

1 Like

In HORECA they are undercutting literally like Jio to Sula. How sustainable it is for shareholders due to frequent fund raising requirement due to burn for gaining market share and funding excess working capital we have to see

1 Like