Update:

Past week events suggest that for AA and his backers, the chickens have come home to roost.

Past few weeks, the media was abuzz with gr8 comeback of AA with positive stories about RPower and RInfra.

But this was not evident in June SH of both:

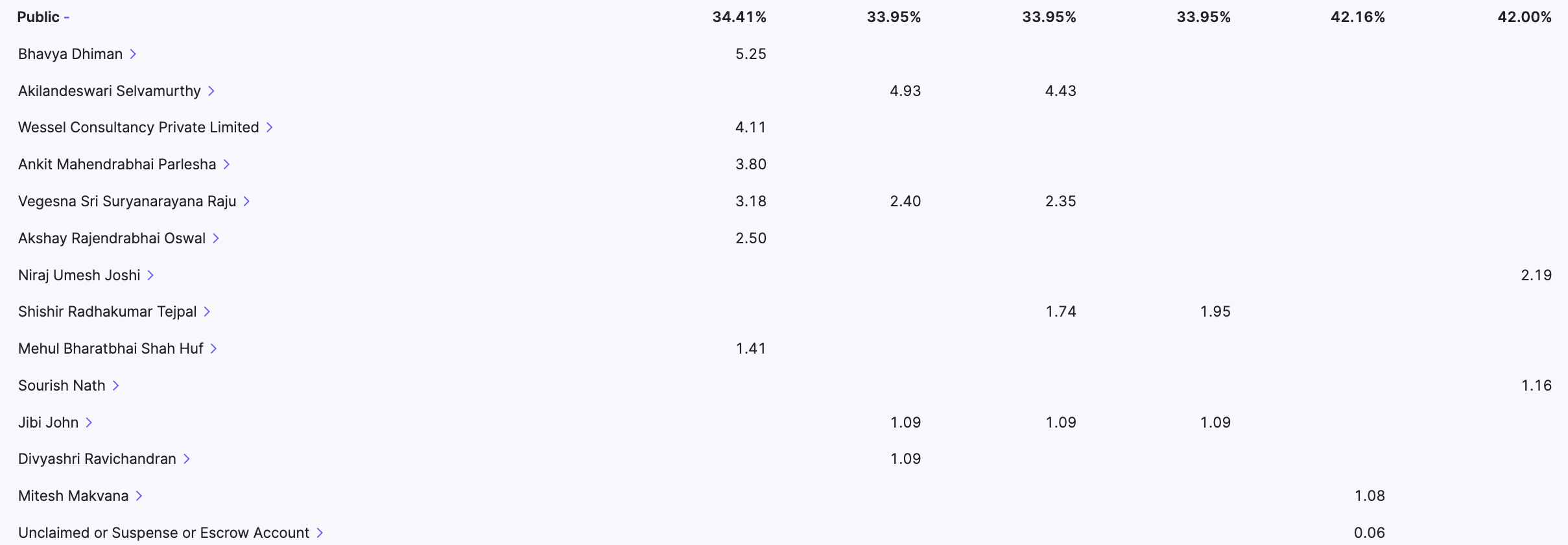

RInfra:

Mathew Cyriac - 1,29,63,593 to 55,28,596

Authum - 4,31,21,879 to 4,12,59,850.

Vanguard - From 90,25,054 to 48,50,557.

Florintree - 86,21,066 to 62,55,559.

RPower: Highest number of shareholder numbers in past few years → Dilution rather than concentration.

After this falsified bank guarantee episode, the SECI chief who took the action was removed and RPower was showered with many contracts.

Past week, suddenly AA has come again under scanner.

Both the companies have issued multiple clarifications distancing themselves from AA.

Another curious thing: Authum promoters sold about 3.5% stake via bulk deals on the day of ED raid and later revealed their plan to lend the same to the company → ? Liquidity crisis: Both R Power and R Infra has authum as backer.

It appears political patronage driving favourable decisions has temporarily been suspended or withdrawn.

Lets see whether AA companies can ever create wealth for retailers !!