NBFC under radar for money laundering

SAT gave clean chit to the promoters

2 Likes

Update on Dalmia Cement fraud:

3 Likes

If a company consistently shows high operating margins in the name of changed product mix and operating leverage being kicked in, which is not the case with any of its peers both domestically as well as internationally, can one regard this as a red flag?

Anything to learn from history here or this sign can be ignored when most other parameters are within comfortable range?

Not naming the companies here as it would lead to biasness in answering

1 Like

It need not necessarily be a red flag. One will have to look at several other factors as well such as cash flows, promoter’s reputation (do some scuttlebutt on the management), etc.

Start with gross margins and see what the trend is. Other expenses can move operating profit % but gross margin does not change for a standalone company while the rest of the industry operates at a different level unless the specific company is doing things very different.

One thing I always do when looking at a new business is to compare margins across various companies in the industry - gross margins, operating margin, EBITDA, PAT. Also see how gross asset turns is changing as utilization becomes higher.

If the entire industry operates at asset turns of 2x while a lone company claims 3x, the product portfolio or the technology used has to be drastically different. A good example is the gross margins of Greenpanel and Century MDF, the former does around 55% while the latter does around 42% since the technology used was different. Greenpanel got expensive machines from Europe while Century MDF settled for cheaper machines from the East. Most industries see gross margin cluster within a tight range unless the product portfolio/customer segment/pricing is drastically different.

Which is why it is a good idea to understand the business landscape, competitive structure and profit pools before looking at company specific financials. You cannot tell an outlier unless you know what the base rate/average is for that segment

34 Likes

Interesting presentation by Nitin Mangal on accounting related issues. 45 minutes talk provide good insight about innovative way accounts are dressed. https://youtu.be/dopgd6tZwsk

6 Likes

Under the Board’s Report in Annual Report there is a heading “Transfer to Reserves”. some companies state “it do not propose to transfer any portion of profits

to Reserves” (see marico) whereas some companies state that so much profits is being decided to be retained in the retained earnings - (Example- Divis - “The Directors have decided to retain the entire total comprehensive income of Rs.136750 lakhs in the Retained Earnings”)

Can anyone explain what is the significance of this ? where would the profits go if not transferred to reserves. Thanks

1 Like

Retained Earnings are simply profit retained after all outgo, including distribution of a part to shareholders (dividends). This amount will be utilized by the company internally (say to fuel growth thru capex or reduce debt or something else). You might have heard the words “thru internal accruals” from managements of various companies, retained earnings are those accruals.

Reserves are nothing but bucketing of capital available for a company. Sum of all reserves + equity is book value.

Whether a company decided to distribute retained earning in to buckets (general reserve, capex reserve, employee reserve, pension reserve or something else) is just a matter of accounting entries.

Do note that not all reserves are available for deployment/investment or distribution.

3 Likes

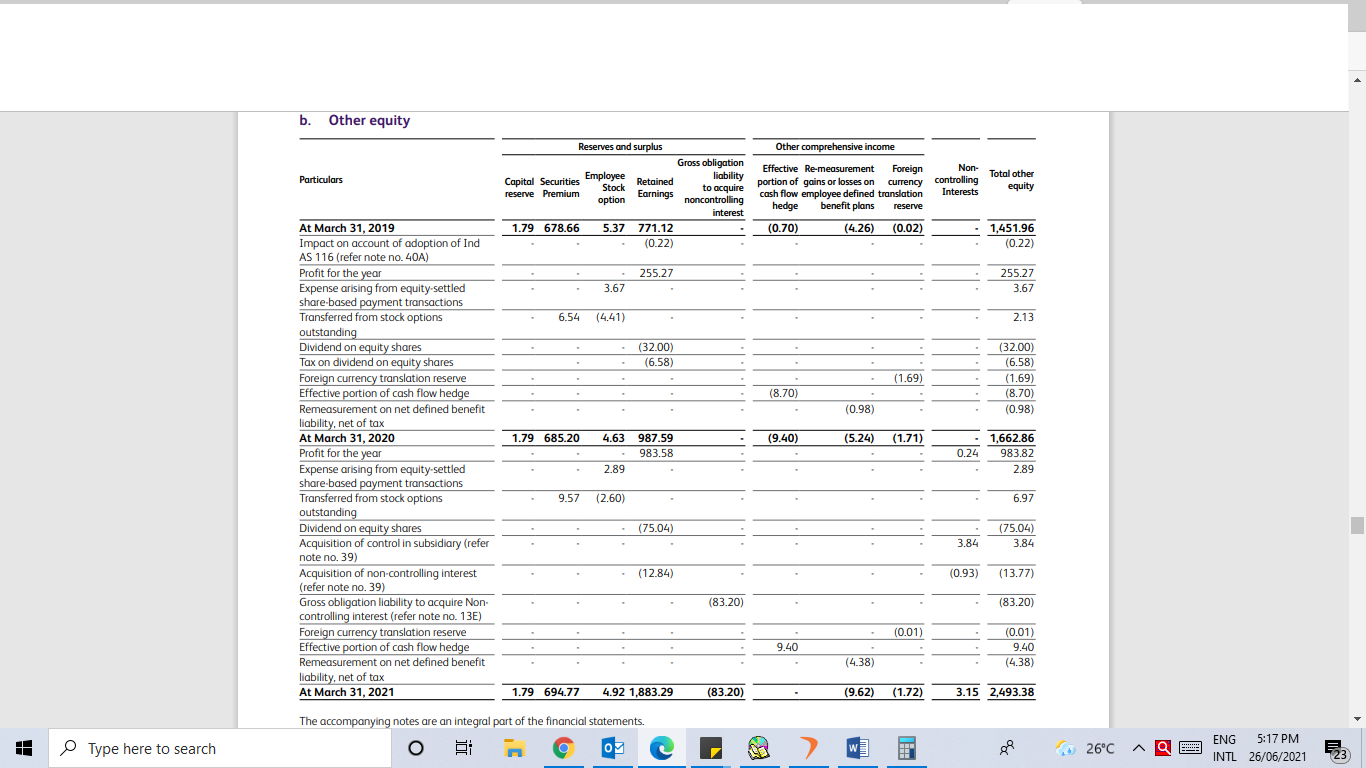

In the annual report of Laurus Labs, they have profit of 983 Crore which is transferred to retained earnings after providing 75 crore for dividend and 12.84 cr towards acquiring some non-controlling interest. So the total in the end is Rs. 1883 core which is the retained earnings as on 31.03.2021. This along with other reserves added the total of Rs.2493 is the total other equity. There is no confusion till here.

But the Boards Report reads thus:

Transfer to Reserves:

Your Company does not propose to transfer any portion of profits to Reserves.

Trying to understand this part. They have transferred the profits to retained earnings and then it forms part of the reserve but what does the Board report in this regard mean.

Just trying to understand things using the above company as example.

1 Like

I think that simply means that they are keeping the options open on how to utilize the profits.

2 Likes

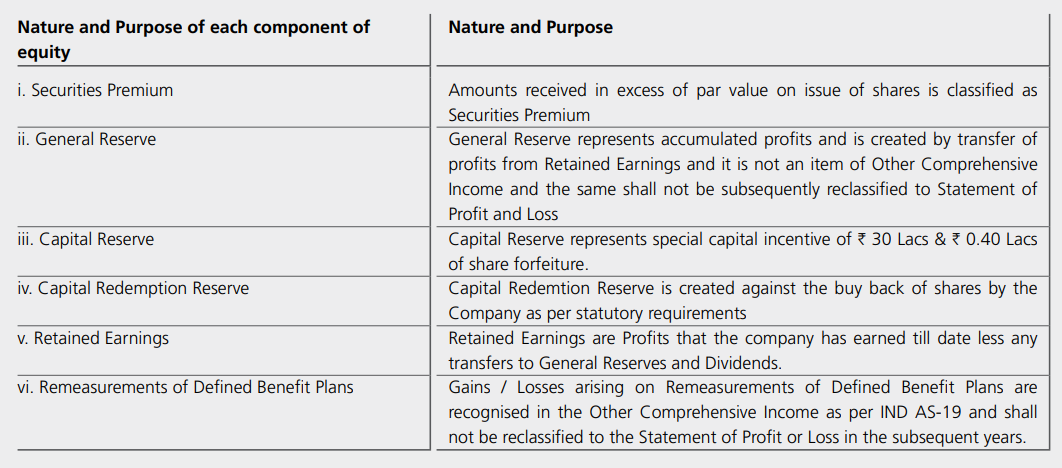

I think that the below may help (snapshot from AR of ’ Vinati Organics Ltd’). Shareholder’s Equity (from issuing shares and profits earned by business) is bucketed among below shown categories)

3 Likes

The Talwalkars default in 2019 was another big lesson for the investors and the lenders. I’ve written how a diligent investor could have identified the red flags as early as 2015.

13 Likes

https://valueinvesting.substack.com/p/evergrande-part-1 an excellent read about the Evergrande issues and deep analysis of their cash flow statements.

1 Like

I believe FCF has a very serious flaw in its computation. Traditional measure is CFO- Capex. But, for a business to grow it needs to spend heavy amount on capex, R&D and SG&A in current year in order to receive the benefit from future. If a business have a good runway ahead, and they want to invest heavily for growth, they will have always fluctuating or even negative FCF like Amazon, Adani green etc.

Calculating owners earnings is the better way, which is widely used by most value investors.

2 Likes

That’ where Mr. Buffett messed up by buying IBM. They just so flourished by the management’s quality and forget its still the IBM, fighting in intense competition.

Hi there,

I have a question, we often see transferring resources to other group companies (same promoters) when there is group’s presence on various steps of a value chain, and often send/receive resources as a help or rescue and they mention these in RPTs with clarification. Now, does that mean it is a serious red flag? (given the fact that, other businesses of promoters do not compete directly). I just need more clarification on, when it will be said as ‘Promoters are just channeling out money of the business’ and when, ‘A group company is just helping another group business for commencement of business’. How to differentiate this? Can you please clarify this? It will be a massive help!

1 Like

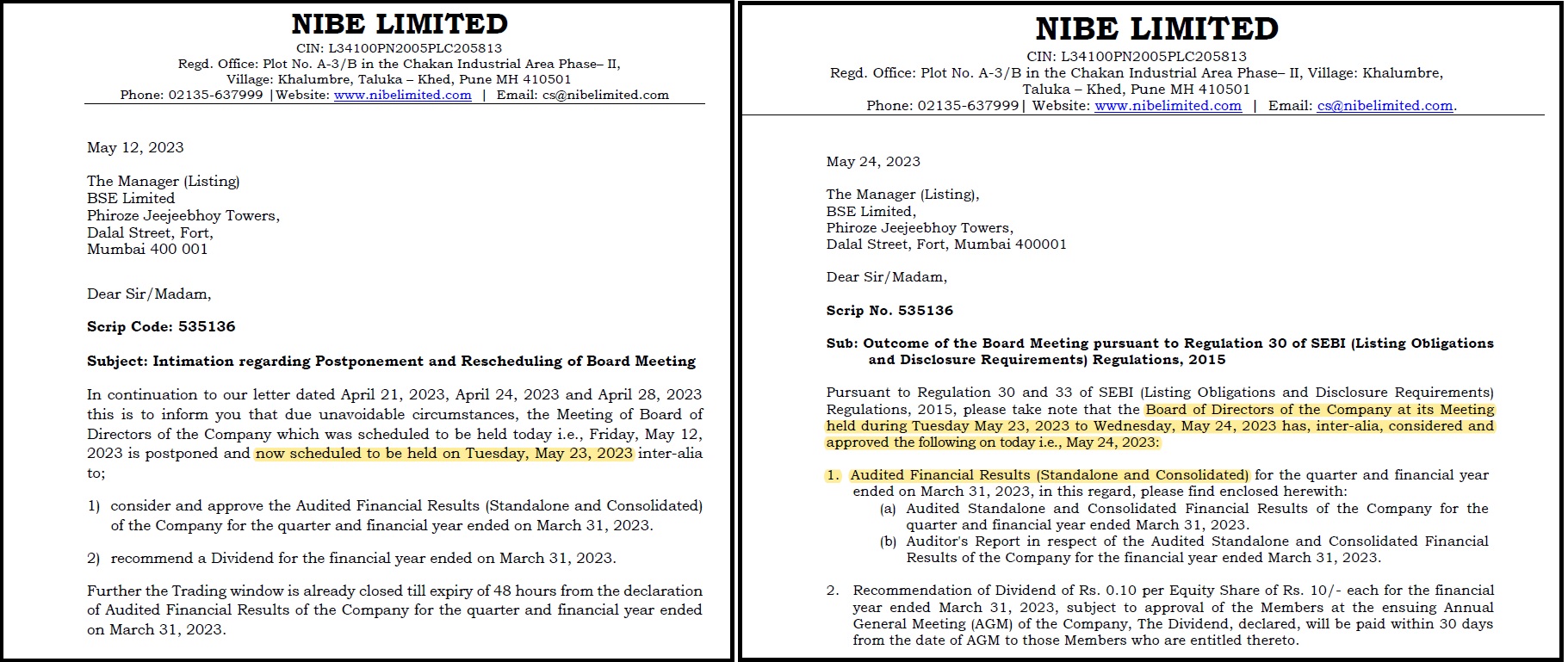

NIBE Ltd’s board meeting for quarterly results went on for 2 days.

Why would a board meeting for quarterly results take 2 days time?

Even if the meeting is concluded on the 2nd day, aren’t they supposed to give prior intimation to exchange about it?

6 Likes

This alone cannot tell us anything we need to triangulate here. But, if there is cultural collapse is brewing, and they do have corporate governance issues like misuse of funds, unusual relationship with managers and board, promoters then yes, holding position as a director in subsidiaries companies and parent company might be a big red flag. one thing to look at in those cases, is to ask one question - Is there is a tightly woven web of insiders? That might allow them to do shady things and cover them up.

2 Likes