Consistently sales numbers are good in Q1 FY24.

Expected Q1 FY24 sales should be around Rs. 1520 crore.

Consistently sales numbers are good in Q1 FY24.

Expected Q1 FY24 sales should be around Rs. 1520 crore.

Domestic sales is improving on a month on month as well as YOY basis. Export sales are muted on a MoM basis. However, Production figures are really impressive.

2987 vehicles in July 23 as compare to 2431 in June 23 and 2154 in May 23.

Production figure seems to be highest ever and it augurs well mainly for two reason:

Good set of quarterly numbers by Force Motors.

All time high EBIDTA margins.

Force motors.

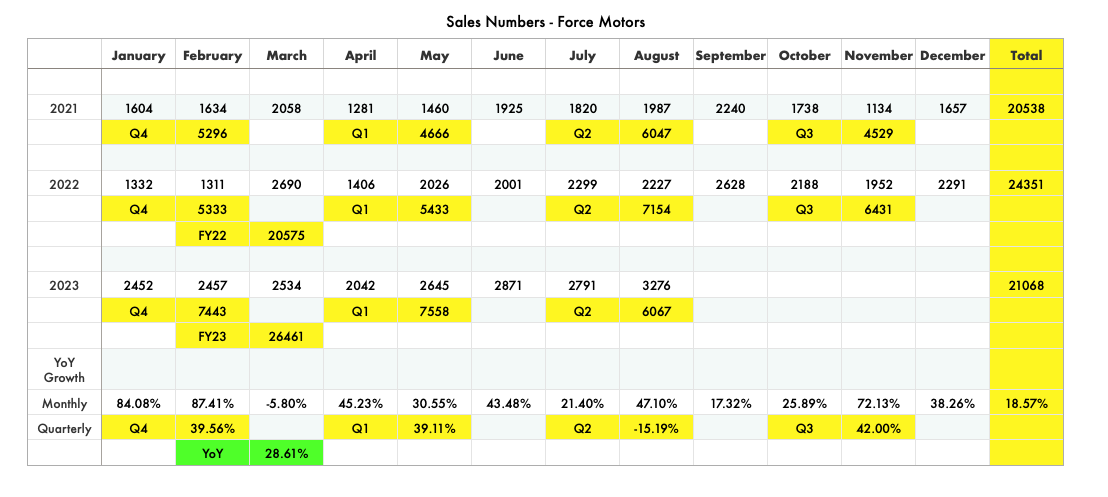

Sales Aug 23 - 3276 units vs Aug 22- 2227 units- up 47 percent YOY.

And it was 2791 units in Jul 23. That is up 17 percent QonQ.

Anyone attending the AGM?

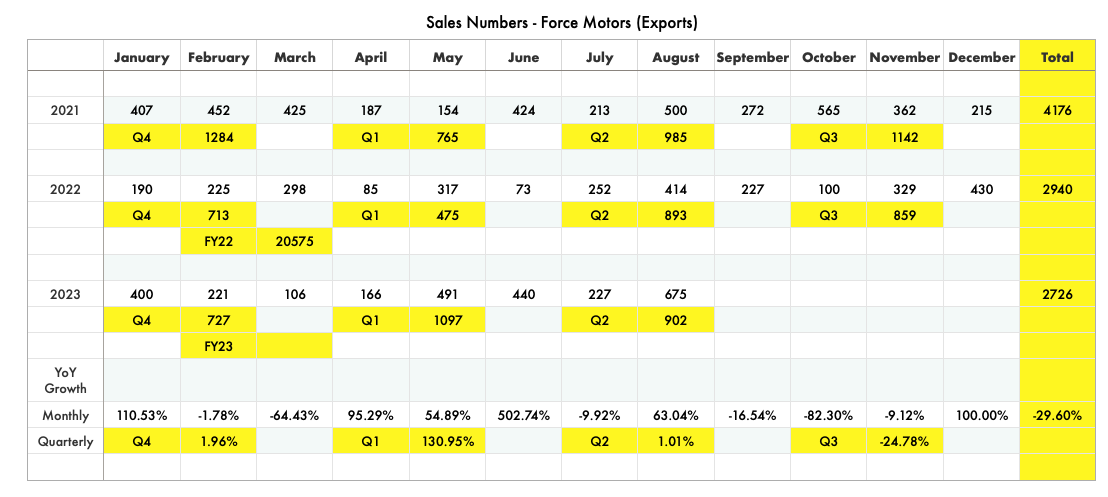

Export sales are impressive at 675 Vehicles and seems to be all time high. Further, Production data is also very strong which is indication that Company is seeing a good demand ahead.

Company is the market leader with dominant position in its segment and you can hardly find any other vehicle in Traveller segment. With the receding of COVID shared mobility and tourist activity is bound to increase.

Current sales data is multi year high and the last high was 4518 vehicles in Mar 2018. It means company is capable enough of reaching to above 4500 which leaves a lot of room for upside and with the commissioning of recent CAPEX it can achieve substantially high sales and manufacturing figures subject to favorable market condition.

Also with rising income people will spend extra money for tours and travellers. The traveller segment of the Company is a proxy to tourist industry.

@Investor_Mohit , please share granular details as your a re maintaining very impressive data base.

The company has done exceedingly well - way beyond what I expected them to do.

Still operating leverage is yet to play out - in last quarter, ebitda margins improved because of expansion in gross margins. As the capacity utilisation has improved in current quarter and fixed costs remain the same, margins can improve further.

Note - these numbers are ex-Gurkha as they are yet to launch BS-VI Phase 2.0 variant of Gurkha, by september end it will be in their dealership stores most likely.

Their export sales are at highest level since Jan-2021.

Q2 can be bumper as they are only 1500 short of their Q1 sales figure in just 2 months.

I won’t be surprised if the stock gets rerated again as commentary is bullish in the annual report also.

D - Invested from 1100-1200 levels, no reco.

Lot of growth levers to play out. Force was spending huge capex for last 5 years.

Sky is limit going forward. Entered in 2017, long wait:joy:![]()

Extracts from Annual Report:

Positive comments and outlook for the future by Management. Mangement had been conservative in the past also and such outlook gives positive sentiment on the Company:

It can be noted with pleasure that demand in the market for Company’s products has steadily risen over the last several quarters. After severe contraction of business over 2 years, due to

the impact of Covid where significant market segments like school buses, employee transport and tour & travels were severely affected, today fortunately all three markets are performing well, as was expected. From the last quarter of the financial year 2022-23, the business has been steadily rising. Along with the topline, the bottom line has also performed well. We do believe that this trend will continue.

The new generation products introduced by the Company, comprising of the completely new platform of Vans – an extension to the Traveller range - and branded the “Urbania”, also the very high-tech monocoque 33 and 41-seater Monobuses, (first anywhere in the world -approximately 1 ton lighter than competition), and the very attractive and rugged, the new platform of “Gurkha”, are all seeing increasing demand.

The Urbania is in the initial stages of marketing. The footprint for sales is being increased

in a calibrated manner. Feedback from users is very positive and encouraging, for all the three new technology and improved product platforms.

We now have, in full flow production the Engines meeting the rigorous emission requirements of BS 6.2 level, while maintaining our excellent standards of reliability and performance. The

development of the latest engines enables us to offer excellent power output and fuel economy, on the Traveller, Trax, Gurkha, Urbania and Monobus series.

The Component businesses of the Company for supply of engines, both to Mercedes-Benz India Pvt. Ltd. and BMW India Pvt. Ltd. has improved on robust demand volumes. These high-end world-class vehicles, in the top bracket of the passenger car market, are seeing

good demand due to the stability and improving spending ability in the market. The dedicated Plants for these products are functioning well.

Finally, while looking today at the future outlook, one can feel more confident about the prospects of the Indian economy, and thereby of the essential manufacturing industry over the next several years. The energy in the economy is higher than before. Steadiness of

demand and increasing opportunities to enter new segments, and introduce world class products, is a matter which enthuses the Company’s Management Team.

INDUSTRY STRUCTURE AND DEVELOPMENTS

The Automotive Industry, both in terms of vehicle technology demanded by the market, and in terms of the technology of the componentry required - is evolving rapidly. It is clear that the latest generation of Diesel Vehicles meeting BS 6.2 standard will have validity and demand for several years ahead. We are required to continue to make continuous efforts to

improve the Diesel and CNG Engines as we go along. The diesel fuel will survive for longer than recently predicted. We have well established and highly acclaimed diesel engines and drivelines, which is a cause for satisfaction.

In the case of Commercial Vehicles such as ours i.e., such as Vans and Minibuses, clearly the market opportunity for electrified vehicles lies in last mile connectivity. Electrification is logically only justified, in terms of the total life time cost of the vehicle, on the basis of substantial mileage to be covered, because the savings in electric vehicles stem fundamentally from the very high efficiency and very low cost of electric traction in comparison to fossil fuel drivelines. The more the EV is run, greater the justification for the

extra cost of the EV system. Commuter vehicles in the normal sense are not best suited for

electrification at this stage of the evolution of the market.

The opportunity is seen mainly in last mile public transport, in conjunction with and complementary to the trunk routes of large electric buses, metro and local trains, to facilitate passengers to travel from homes or place of work to the main line metro, railway or

large bus transport.

The electric vehicles developed by the Company are undergoing introduction trials, and we expect to get orders during the next two quarters to really bring our vehicles on the road. Since this process involves State Governments, Municipal Corporations and Specialized Fleet Operators, etc. the nature of the sale is different from that of individual vehicles like motorcycles or cars, sold to an individual user.

The business structure, the contractual and financial arrangements required for implementation of such fleets do need time. While metro trains and electric bus routes over long distances in major cities are now getting established, the next expansion phase, must logically include last mile transport, which is the area we hope to participate in. The Company is enthusiastically engaged in delivering efficient, attractive and economic solutions, for this usage.

Hi Mohit, will you be attending the AGM?

Most probably, I’ll be attending the AGM.

Force Motors Update : (AGM Key Takeaways)

I didn’t attend the AGM but this is what the people had to say who attended :

Management has guided for around 15-20% volume growth in OEM business for next 2-3 years.

Urbania exports to start by early 2024, Urbania-electric to be launched by mid-2024.

Guidance of around 15% growth in Engine business (to BMW,Mercedes) for next 2-3 years.

JV with MTU (subsidiary of Rolls Royce) to achieve breakeven this year ; guidance of 500cr annual revenue in JV (in short term).

Consol operating margins can sustain in double digits.

D - Holding from lower levels, not a buy/sell reco.

Force Motors AGM was quiet detailed. Some KTAs:

→ Indian economy continues to be resilient in the face of a global slowdown. Company expects demand for it’s products to continue and current volume run rate is sustainable.

→ Management is looking at 10-15% volume growth CAGR. When questioned whether company is being conservative,they responded by saying that it’s better to be pessimistic than be very optimistic.

→ Seriously looking at Defense as a key growth driver.

→ Export markets like Middle East,Africa were adversely affected due to Covid. However,everything is on track now thus the accelerated pace of exports. Africa is a high potential market for the company from both existing and new platforms.

→ Company’s efforts to rationalize on cost side & improve profitability have started bearing fruit. Focus will be to leverage market position and improve on profitability further.

→ While EV is the future,management doesn’t foresee any adverse impact for many years to come. Yet company is readying for new products in this basket. Overall,1000 cr will be invested over the next 3 years on new product development.

→ Breakeven of JV was delayed by 3 years,mainly due to Covid. Fy24 should end at breakeven & contribution to bottomline should accrue from Fy25. 500 cr revenue here is a low hanging fruit.

Almost all participants asked good questions. Some questions on tax rate & concall weren’t taken up. Overall,the management seemed very happy with the company’s progress in the last year or so & was confident of sustaining current numbers.

Disc.: Invested. Views are biased.

Sales in september 2023- 2973 vs 2628 last year

Sales in Q2 23- 9040 vs 7154 last year Q2

Domestic sales in Sept 23 (2580) are in line with previous month(2601). Export sales have fallen from 675 to 493.

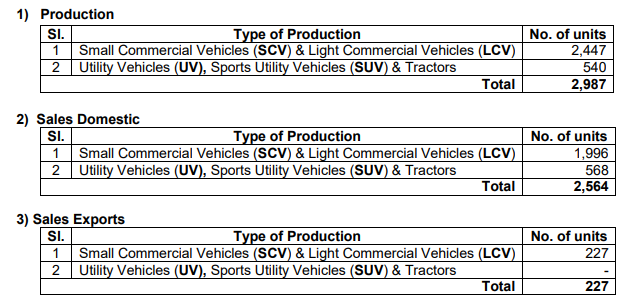

However, production figures are very impressive at 3438 as against 3032… which shows that company is anticipating good demand for the festive season… There is substantial improvement in Monthly , Quarterly and Half Yearly figures during current FY as compared to previous FY.

Very solid quarterly numbers from FM.

With Q2-2024 total sales of 9040 vehicles, FM is expected to report sales of Rs.1790 crore (a rough estimate). With a margin of 10 to 12 % it can report PAT of Rs.96 crore and Rs.132 crore respectively, alongwith EPS of Rs.76 and Rs.103.

Production figures are also very encouraging, hinting at least similar sales numbers.

Monthly sales number for Oct have fallen which is line with past trends.

Oct 2021 : 1738

OCt 22: 2188

OCt 2023 : 2254

Monthly performance was better then last year but more was expected from the Company.

why this stock stopped trading on NSE ?

Greatt set of results from the Company…

Reduction in long term borrowings.

Cash Flow from operations for H1 was at Rs 316 Cr

Recievable levels have also come down in absolute as well as in days.

Sales and Profit have improved substantially.

EPS for H1 FY 2022-23 was around Rs 2 & for H1 fy 2023-24 is at Rs 123.

The main thing which i like about the Company is the undisputed leadership in the segment which it has presence (Traveller) and I hardly see any of its competitor on the roads across India.

This segment is bound to grow substantially as it mainly involves Tourism, School and daily commutation of employees…

Current levels of sales are equivalent to that in 2017-2018 and company has done CAPEX of around Rs 1000 Cr after that and as such there is lot of room to play for operational leverage and improvement in margin.

At the peak of valuation of the Company in April 2017 the stock price was around Rs 4700 and EPS was 137. The current H1 EPS is 123 and valuation is around Rs 4000.