I am unable to understand what this declaration means. Can you explain?

This is my first post , I was going through the posts and thought of sharing my thoughts , and if there are any mistakes in my views please accept my apologies.

@ranvir -Schweitzer - I couldn’t find an Italian company like this - Can you post the link if available?

Outdoor lighting - Their product range is very limited as per their website (Plus Light Tech), in this segment their main competition will be with Lighting Technologies ( Subsidiary of Russian Company), Signify , Panasonic,( Roads, Ports, Stadiums etc)

K-Lite - Outdoor lighting portfolio is much bigger than Focus lighting in the outdoor decorative space. K-Lite might be importing housing from china and assembling it in Chennai , this could be to make it more competitive and transfer most of the fixed cost of production to 3rd Party.

@johnsgeorge.cet : Your enquiry about Focus Lighting to IHG , their Client tele is different and probably that could be the reason the sales person of IHG couldn’t know about it. Focus has an office in Ajman freezone and targets major retailers for their showroom lighting, the business is headed by an Indian, who was working priorly with a major German Lighting Manufacturer in UAE.

Focus - Opening an experience center in Saudi Arabia is an interesting move, because of the project volume in all provinces of Saudi Arabia.

Focus is a Manufacturer predominantly focusing on projects, and the order bank will not be regular and there will be payment issues for sure.

Usually companies tries to strike deal with European or American Manufacturers to become there OEM partner for products, by this they can expect sustainable revenue. and i could see only schweitzer in this direction (website not found for schweitzer)

Focus Lighting Q4 FY24 concall notes:

The company is a pioneer in many lighting fixtures. Many of its products have patents with products that are disruptive with superior tech. Its products are one of a kind, with no other company worldwide providing such products (as claimed by the management).

Take a look at their concall presentation conducted on Zoom in which the management has explained their products & initiatives in the first 35 mins - Focus Lighting Q4 FY24 Concall presentation

Financial performance

Stable performance with 60 Crs topline - almost same as last 2Q, 10 Crs bottom line - same as last 3Q. Expected EBITDA margins of 22%. No surprises here.

Growth - Trade division, new products

Retail - The company invests a lot in R&D, innovation & tech. All their innovative products & designs are patented. For ex. they have been able to reduce no of fixtures needed for retail stores by more than 25% using innovative designs & tech. This will lead to lower electricity & air conditioning load for store operators. Using better lighting fixtures with less light spillage. They serve customers like Mercedes, big auto showrooms, IKEA, Reliance retail among others.

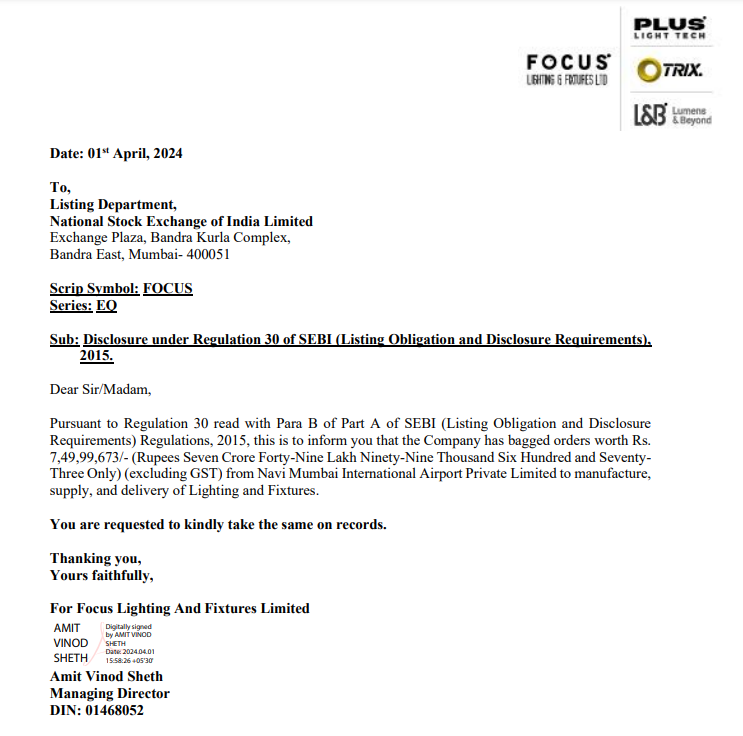

Home & Infra - Both divisions to experience rapid growth. The Infra division will see good traction as they bid for more projects nationwide. Approval has been given for light fixtures for Vande Bharat trains from railways. They recently won the bid for Navi Mumbai Airport.

Trade - This is a new division they plan on starting. Plans to enter the high volume, low-value segment of manufacturing for big OEMs & also begin to create a brand from individual sales. They want to manufacture differentiated products for OEMs which score high on sustainability by reducing weight by eliminating aluminium & reducing production time. They expect blended margins to be stable. Chinese imports do not seem to be a big problem as their products are differentiated & not basic commodity nature.

Experience centers & Exports - They plan to set up experience centers in the Middle East & India to increase brand & product visibility. Middle East is a booming market with good opportunities.

Guidance

Guiding for 15-30% sales growth, more towards the upper side. ~20% OPM’s.

There is some elongation in the receivables days due to infra projects. The company is also investing in CapEx for future growth, as seen in CWIP of 19 Cr upon Net Block of 21 Cr. I don’t know the nature of this capex, whether it’s a new facility for the trade division, new machines for increasing production or the new experience centers they were planning to set up.

*Focus Lighting - **

Q4 and FY 24 concall highlights -

Q4 outcomes -

Sales - 60 vs 41 cr

EBITDA - 14 vs 8 cr ( margins @ 23 vs 20 pc - very healthy margins for a manufacturing company )

PAT - 11 vs 6 cr

FY 24 outcomes -

Sales - 224 vs 168 cr

EBITDA - 46 vs 33 cr ( margins @ 21 vs 20 pc )

PAT - 39 vs 23 cr

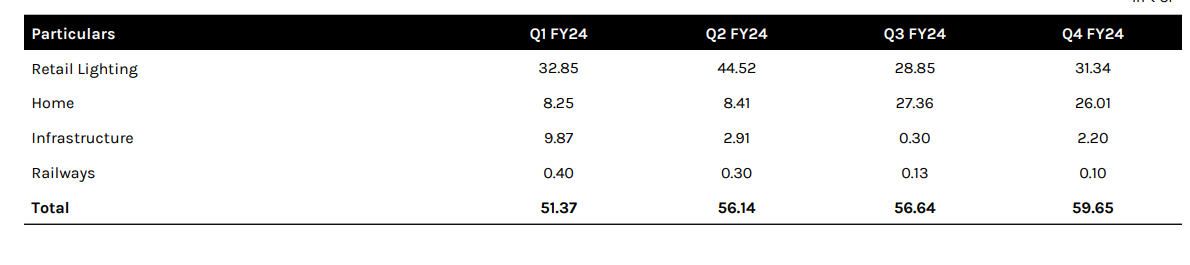

Breakdown of Q4 revenues -

Retail Lighting ( high end / specialised lighting solutions for brick and mortar retail outlets ) - 31 vs 32 cr

Home lighting ( company is into high end home lighting unlike most other players like - Havells, CG Consumer, Surya etc ) - 26 vs 8 cr

Infra Lighting ( basically - projects / orders based business ) - 2 vs 10 cr

Railways - 0.1 vs 0.4 cr

Company’s retail lighting is primarily sold under PLUS - brand name

Company’s MD gave out a presentation on the kind of cutting edge / unique lighting solutions that the company has developed / is developing. Its a must watch for anyone trying to understand the moats that the company is building

Company’s retail clients include - Mercedes, Volvo, Porsche, Citroen, BMW, Tata Retail, Reliance Retail, Ikea, Lenskart etc

Some marquee projects where company has done the lighting work include - Central Vista - Parliament, Surat Fort, Guwahati Airport, ITC - Shanghai, Mumbai Airport etc

Reliance is the biggest retailer in India. Company expects Reliance retail to be back to aggressive expansion mode wef Q3 this year. That’s when they see a lot of domestic retail business to come to them

Retail segment in ME markets is doing well

Overall, guiding for > 15 pc growth in retail segment for FY 25

Expect to see high growth coming from Home and Infra segments for FY 25

All verticals combined, company is guiding for 30 pc kind of topline growth with margins at current levels

Avg ticket size per retail store ( except very large format stores like IKEA ) @ Rs 20 lakh to Rs 1 cr. For Infra, its Rs 5 to Rs 40 cr depending on project to project. For Homes, its between Rs 5 lakh - Rs 3 cr per house

Company is going to enter the trade segment in 6-8 months. Initially, the company will get into contract manufacturing for the bigger brands. But the company will only make the differentiated products. In medium term, company also intends to develop its own brand

Disc : holding, biased, not SEBI registered

The company seems to be truly innovative in terms of product design and applications. They have lot of patents as per their latest concall. This concall and presentation provides lot of insights on the innovation that the company is doing.

Such a company with distinguished products should command some pricing power and favorable trade terms. The trade terms are clearly not in line with that.

The debtor days have almost doubled to 140 days from 68 days. This is the highest it has ever been. The entire amount (almost) of 85 crs of debtors pertain to Home and Retail division whereas management alluded it to Infra division in the concall. This seems to be a key monitorable as this amount is 75% of the sales of both the divisions for the last 2 quarters. The question is if there is anything more to read into this. CFO/Op. Profit = ~9% for last 7 years.

The company will require additional debt / fund raise to achieve it’s desired growth of 30% if debtor days stay elevated.

As you have rightly pointed out, there is clear disconnect between what management claims as their uniqueness vis-à-vis what P&L says and hence what market believes. I have checked with my few interior designer/architect friends and they have not heard of this company, which is bit surprising. If their lights are indeed so unique, world should be running after them or at least should be aware of them.

Secondly if you visit their company website, it is made in WordPress ! It is so poorly designed and many sections like Äbout Us" “Our Clients” and “contact us” do not work. Only investors section seems to be populated. See the link below

https://www.focuslightingandfixtures.com/

A company claiming to be so innovative and wants to attract more customers to itself is having such a poor front end to the world. I am aware that they have separate website for pluslight tech but neither one can visit that website from main company website nor that website shows any connection to main company. Sounds fishy, isn’t it?

In recent concall, I had raised this question to Mr. Sheth about why the company website feels like “work in progress” but he brushed aside my question saying as company is evolving the website would be like this…and this did not reflect in the concall transcript…:- ![]()

Disclosure - Invested but started feeling nervous. Exited yesterday

I agree with ur concerns wrt the poor quality Website that the company has

However, let me share some insights from the Lighting Industry experience that I have ( my brother is a distributor of CG Consumer Lighting in Mohali. Plus he is also into retail of Philips Decorative lighting )

LED Lighting Industry is basically divided into 3 segments -

Luxury

Premium

Mass

Luxury sales only happen through the Architect channel. The cost per luminaire can vary between 5k - 5 lakh - depending on size and design. Per house bill for lighting comes to between 5 lakh - 1 cr … depending on the size of the house / client’s pocket. Even a rich client will never buy such products unless convinced by an architect. These architects do recommend foreign brands. But - here I am talking about very high profile Clients and Architects. Virtually no popular brand available in India caters to this segment.( Philips did it aggressively for some time but now has shifted to the premium segment as this is not a high volume segment ). So - if a company has made a name for itself in local markets of a few cities with a few architects … it’s completely believable. Architects also know, virtually no one in India is making these products. No big brand - for sure. Its an extremely niche but high margin segment

Premium and Mass segments - This is where all brands like - Philips, Havells, CG Lighting, Wipro Lighting etc operate. Here too, volumes in premium segment are limited. Mass segment is where the real volumes are

My two cents ![]()

My suggestion - pls write to the company or the IR person. Generally they respond back

Did that for another query post last quarter results. No response to my email from company. Hence emailed to their IR firm M/s. Kirin advisors (on the email given on investor ppt). After waiting for a week or so, I called up Kirin advisors by phone. (again on number given on investor ppt). They asked me to get in touch with a person who was handling Focus. I told her my query and she asked me to forward it on her company email address. I did that and then followed up with her but no response…

This left bad taste in my mouth and hence decided to exit completely.

You can write to the company CFO, he replies promptly

Technically too, the chart is forming rounding top with higher than normal volumes. Looks like it’s in Stage 3.

It is Smallcap company , how you can feel sad when your friend doesn’t know it ,

Most of the people don’t know value investing , it does not mean value investing doesn’t exist

Website is minor issue ,it is not affecting their business and fundamentals , it is a issue but minor

You can also accept it as it is small cap category

You will regret it afterwards for selling it

There orders are enough for vouch their growth story

You are judging too early

One should have Guts and convinction in their investments

Every company has its pro and cons

I appreciate your comments and concerns. But I would prefer to go by my own thumb rules and gut feeling. After spending many years in the market (and in micro caps mainly), I understood that I need to be comfortable holding onto any investment. In this particular case, I could be wrong in my assessment. I played it both ways in the past and this learning is from burning my fingers few times. So its better safe than sorry for me. In economy like India, there are so many opportunities, so why remain invested in company where one feels iffy. Thats just me. Needless to say, this is not an investment advice.

Can you share his email ID?

Total Infra sale for year was 15.28cr. Receivables increased from 32cr to 86cr…When question was asked about icrease :-

Q) So, my last question is, this significant jump in receivables this year, any comment on the same?

Amit Sheth: See, infra projects are increasing. We started two years back and it’s actually becoming bigger than home, maybe it will be parallel to retail. Now we all know that government money is secured. Infra is mainly with government or large contractors like L&T, Shapoorji Pallonji or Tatas. The problem is that till the time the project is not executed; the payment is not cleared and that’s where it is a little bit stretched out. But what I understand from our CFO, maybe Tarun, if you can come in and explain what you had during our annual sales meet how the payment has improved.

Payment in regards to retail, home and other sectors, we have controlled over it and as sir rightly said only in infra wherein there are government formalities are involved. In that, it is taking time. Otherwise, if you see in retail and home and in railways, we do not have substantial outstanding at all, I mean every outstanding has been controlling below 180 days. So, it doesn’t go above 90 days in short, to be very honest. But it is well in control in those three verticals.

Q)But if we see the fourth quarter, the main contribution was coming from retail and home. But still our receivables jumped to 81 crores, while the turnover was just 60 crores.

It’s an accumulated receivable. It’s not of that quarter. You are looking at the turnover of the quarter, but the receivables are accumulated of the whole year, no. See, as a company, what we see is whether it is 30 days outstanding, 60 days outstanding, 90 days or 180 days. So, it has got nothing to do with the turnover of that quarter, but it is not possible technically that if you have 60 crores turnover, you will run outstanding of 80 crores, right? So that is an accumulated over a period of time.

Q)More than six months, what is the receivable we have?

I think what we can do is you can ask these questions on e-mail also because there are a lot of people waiting, they’re almost 19 messages here so that it can just move a little faster and those questions can be answered in between also. Tarun, just remember this and answer it once you see it.

Neither invested nor tracking the company.

All the infra projects for the company are based in India. However, If we look at the standalone Receivables, it has hardly changed from 35 cr LY to 34 cr TY. It’s the overseas subsidiaries receivable which has increased from Nil Last yr to 52 This Yr (Against an Overseas Revenue of 90 cr) !!

Not sure why the management would not mention anything along these lines and put it on Infra. Am I missing anything ?

However, to be fair to them, ~85% of their receivable is under 6 months and only ~12 cr > 6 months which corresponds more closely with the infra number.

Not Invested. Tracking.

How did you get these figures, AR is not yet published?