Hi everyone, it is increasingly becoming difficult to find good companies at reasonable valuations and those that are reasonably valued or undervalued both in numbers and compared to intrinsic values or in relative individual perception have some sentiment dampness in the form of high leveraged balance sheet, pledged holdings , low promoter holdings, high rm costs severely compressing margins and innumerable other factors …

So one of the Forward looking parameters i want to research on is Capacity expansion in the background of high demand growth in the market sector where the companies work…

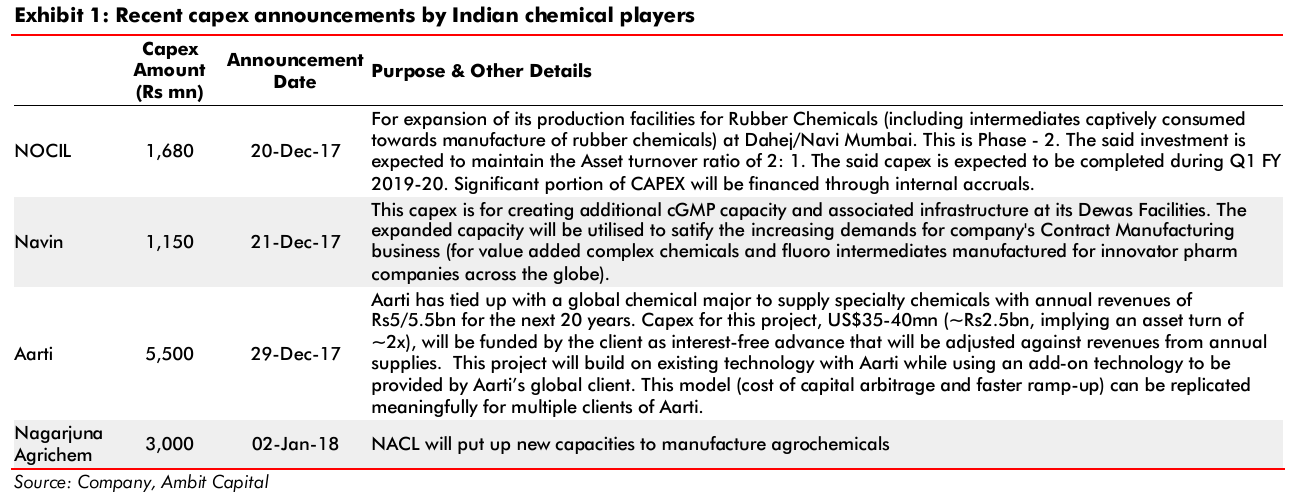

I request all the members of Valuepicker family to enrich each other with ideas in companies who have a significant capex planned in near future or already under process…

Please follow the format of presentation as the following…

1.Company name…

2.Amount or %addition to present capacity…

3.Nature of capex- brown/green field &industry segment…

4.Source of fund(debt, internal accruals, qip)…

5.Incase of funding from debt, present debt to equity ratio…

6.incase of qip, promoter holding before or after qip with %dilution…

7.Timline for capex to come online where ever possible as per management guidance…

8.Outlook on demand growth in the industry segment in which capex is being done

**

Please provide with the latest updated information where ever possible, when in doubt or needs further verification , please mention citation needed…

Please do not discuss about any individual stock in details expect the introductory questions, which otherwise can be discussed in respective company threads in valuepicker…

Hoping the thread to be very useful for mutual discovery…

Thanking you, i will start the thread with my contribution…

DISCLAIMER

Market capitalization and valuation metrics should not be considered while selecting companies for this thread…

This thread does not and should not be intended for any stock recommendation and followers of this thread are requested to follow individual research method for evaluating investment choices if inspired from this thread…