Of late, I am a big convert to practical distilled wisdom from Bharat Shah. it’s best to simply reproduce how he explains why Banks and Financial businesses occupy a special place within high growth compounding machine space.

Within high growth and compounding machine space, banks and finance occupy a special place. Given the ubiquitous need for and lubricating presence of money, and also given the real large size of opportunity, successful finance businesses can get to be very large. Observe the pole position that finance sector occupies in a large and tertiary sector economy such as USA, not just before the cataclysmic events of 2008 but even thereafter.

Bank and finance businesses represent a very unique opportunity in several respects.

1. They are inherently a compounding machine, especially in a continued phase of high growth of the economy since they represent a proxy on the growth of the economy

2. Typically, these businesses tend to be a lead indicator of the growth rather than a lag, in the sense that typically the growth of the banks and finance firms precedes the GDP growth i.e. the growth of the sector tends to be a multiple of the growth of the GDP

In terms of the character of business, there are other distinguishing aspects as well, compared to most other businesses.

1. There is no concept of return on capital employed for obvious reasons

2. It is legitimate for these businesses to have a significant leverage as compared to other businesses such as manufacturing

3. Dilution of capital is part of the game and is not a ‘crime’ as it would be regarded in the other businesses simply because the raw material is money and to that extent the size of the growth will call for well-timed and efficiently priced dilution at defined intervals.

4. RoE is not just an outcome of the earnings growth, but a cause as well

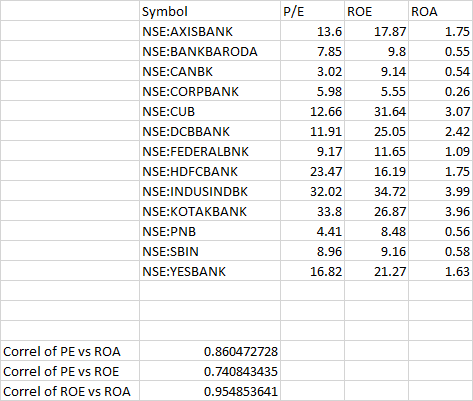

The key value creating parameters are, typically, a matrix of the quantum of growth and quality of the growth (i.e. return on equity). the RoE would be a function of how good is the return earned on assets, how well is the balance sheet quality maintained i.e. deinquency is contained (balance sheet is even more critical than profit statement in judging the health of these businesses), how efficiently have the expenses been managed and finally what has been the level and appropriateness of leverage. Return on Assets (RoA), in turn, is a function of efficiency of the asset book, cost of liabilities, duration management and asset-liability mismatch

The aspects would percolate from a given level of RoA to a RoE. So the critical part of the quality is the RoE which subsumes within itself all four of the above parameters. The growth again is an outcome of a superior RoE, the size of opportunity in the external space and ability of the management to harness the environment, to appropriately take advantage of this opportunity by strategic and well-timed dilution of capital. Thus broadly the matrix would be that the superior RoE combined with superiority of earnings growth will provide the most potent combination and clearly a mediocrity of the RoE would have the most telling effect on the size and the extent of value creation, as well as the size of growth.

When we try to apply this practically to current markets, a few opportunities immediately would call attention. Thought it relevant and topical to start a discussion now on the special compounding machine thesis, and obviously draw attention to value-price mismatched winners.

Hope to see folks giving this some attention:)

Cheers