The Travancore Federal Bank was founded in 1931 at Travancore (now Kerala) with a Share capital of Rs. 5,000.

Subsequently in 1944 it was taken over by Shri KP Hormis, a 28 year old lawyer, and in 1949, its name was changed to Federal Bank.

By the time Shri KP Hormis retired in 1979 (35 years), he had built the bank from a one branch bank to a 285 branch-bank.

Fast forward to the last decade, the Bank has had a very Interesting Journey.

Let’s look at some key parameters over the last 10 years.

| Loan Book | Net Interest Income | Net Profit |

|---|---|---|

| 16.08% | 14.03% | 11.33% |

*Percentages are in CAGR.

Over the last 10 years, while Loan book (Total loans given) has grown (CAGR) at 16.08%, NII Growth was lower at 14.03% and Net Profit growth was only 11.33%.

The Investing community sees this gap between the Loan Book growth and the Net Profit CAGR as a chink in Federal Bank’s armour since this implies that the bank is unable to convert loan book growth into proportionally higher Net Interest Income and profits and is therefore, ‘inefficient’.

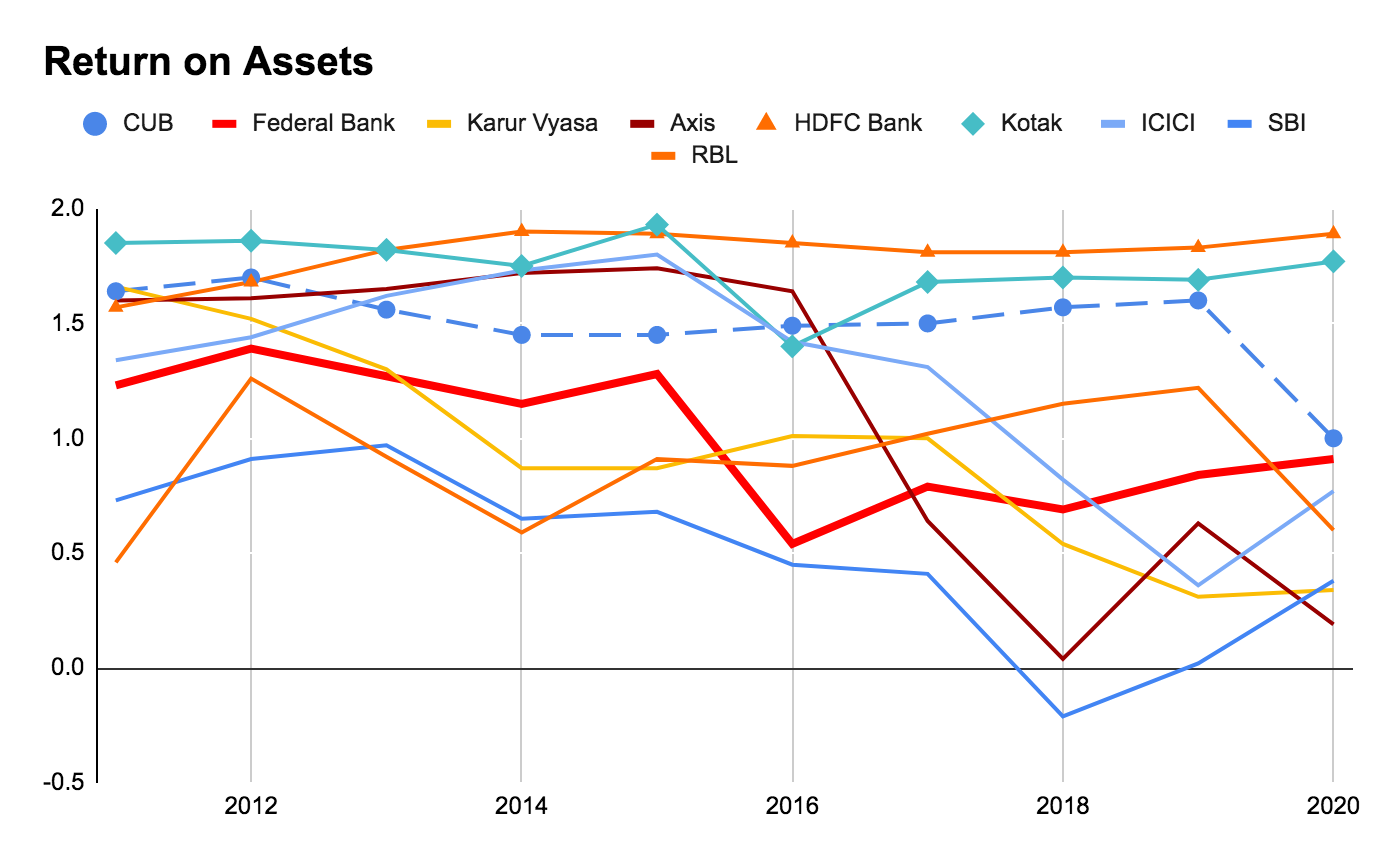

Along with this mis-match in the loan growth and Net Profit growth, the ROA numbers as well are not very impressive compared to say, City Union Bank, it’s well-reputed (but much smaller) regional peer.

City Union Bank (Top) vs Federal Bank (Bottom)

For these reasons, Federal Bank has always been valued as an average bank but still better than its lesser Prosperous Regional peers : South Indian Bank, Karur Vyasa.

This ‘average valuation’ is evident from the P/B valuation the Bank has received from Investors historically, which has always been under 2X over the last 10 years.

City Union Bank has commanded a higher P/Bx than federal bank’s over the last 10 years.

India’s Top Private Sector banks such as HDFC Bank and Kotak Mahindra have commanded PBx ratios of 4X and 3X respectively during this period, for good reason, one can argue.

However, despite these apparent weaknesses, Federal Bank has a competitive advantage amongst the Smaller Regional banks - Lowest Cost of Funds by virtue of Access to Low cost, Sticky Funds from Non-Residents.

Since the 1960s, remittances from the Gulf have increasingly become the backbone of Kerala’s economy, making up ~ 20% of the state’s GDP.

And the Federal Bank not only has ~30% Market share of Foreign money sent back home to Kerala but also a ~17.5 % share of foreign remittances of the entire country.

As you may know, one of the ways banks can gain an advantage is by accessing low cost funds. These usually come in the form of CASA (Current Account Savings Account) + Deposits, and Federal Bank not only has access to NR Deposits, which are stickier because

- Interest is Tax Free on NR Deposits

- Interest rate arbitrage - NR’s enjoy higher Interest rates than in their resident countries,

- NR keep a portion of their money in Deposits for other than consumption purposes.

Not only this but ~90% of its deposits are granular i.e - less than 2 Cr deposits, which are again cheaper than bulk (2Cr+) and Wholesale deposits.

This gives Federal a 30 bps/120 bps cost advantage over its peers City union bank, Karur Vyasa, South Indian Bank and CSB Bank.

The strength of the liability franchise can also be seen from the fact that the bank was able to slash 1 Year Term deposit rates nearly as much as the major banks and 50% more than ‘other banks’.

Yet, despite the advantage Federal bank enjoys on the cost side, a real change in perception and consequently in re-ratings (P/Bx) will only happen when the following structural improvements are visible within the business :

1. 1-1.2%+ ROA & Higher ROE

2. Higher ‘Other Income’ Growth

3. Higher Proportion of ‘Other Income’ in Net Operating Income.

And in order for the above parameters to improve, certain structural improvements must happen fundamentally at the business level.

For Example, in order to achieve higher ROA & ROE, the bank must earn higher Net Interest Margins. And higher NIMs are a function of :

- Recoveries (higher the better)

- Slippages & Provisioning (lower the better)

- Higher Yielding Product Mix

- Low Cost of Funds

- Low Operating Costs

- Consistent Loan Growth, Net profit & EPS Growth

Fortunately, the Federal Bank’s management has been actively working on improving the above mentioned issues since 2016.

As a result, ROA have been improving consistently since 2016 :

There has been improvement in ROE as well but its still way under any reasonable investors requirement. I mean, nobody is getting excited hearing about a bank that earns ~11% ROE.

Also, NIMs are still under 3%.

Additionally, While Price to Book Value has improved since 2016, it has been negatively impacted by a host of factors shown below.

And the current P/Bx as on 2nd February 2021 is 1.04X, up from 0.5x at the end of March 2020.

The banking system is currently enjoying regulatory & legal cushions which may be hiding some of the pain our banks are enduring because of Covid-19 induced slowdown.

Federal Bank is no different, however, the assessment so far is that the quantum of bad loans is a lot lower than initially anticipated.

Even if we consider NPAs that would’ve been declared had the Supreme Court order against declaring NPAs not been in place, the GNPA & NNPA numbers would have been 3.38% & 1.14% (Q3FY21 - Con-call) respectively.

All this aside, the most interesting parts of the Federal Bank story are the kind of developments that are happening on the fundamental business level - Product mix change, mining existing data for cross-selling etc.

These developments are responsible for a 3X increase in EPS over the last 4 years.

If you would like to learn more about the Federal Bank Story, let me know I’ve done more extensive research on the bank and would be happy to share the research.

(Disclaimer : Not Invested. Also, because I’m a new member, I am not allowed to embed more than 1 media item which means at least 7-8 graphs were left out of this article. My apologies if you feel that the article could have been better illustrated with graphs.)