The correct question to ask is whether the RoA and RoE will improve going forward. And if it does, there can be a swift re-rating as there is a lot of potential for re-rating at one time P/B.

In my opinion, Federal Bank is moving in the right direction with neo-banking partnerships, launch of new credit cards, reducing cost of liabilities (down to 4.57% in FY 21) and maintaining stablequality of the book. The new channels will open avenues for cheaper customer acquisition and lower operating costs, aiding loan growth and improving cost-efficiencies. I see the RoAs expanding gradually and the stock re-rating to at least its peak valuations of two times P/B over the next two years.

Agree with your point on ROA and ROE, that has been clearly established. It’s performance has been pretty sub-par but has been improving too, which is what I wrote in my Update post.

It’s an “Okay Bank available at a decent price”. And by “decent” I don’t mean “Cheap”.

Every business is an evolving story and I think along with the past, it’s important to pay attention to what factors might lead to a better future.

Federal Might have some favourable factors pushing towards a better future resulting in better ROA, ROE, Growth, asset quality etc so we’ll see how it pans out.

But IMO, Shayam has been at helm for 10 years & yet they were not able to improve the ratios. When asked during concalls, he skips the question by saying other banks take more risk and we don’t.

They clearly don’t have a mandate to work on these numbers unlike other midsized bank managements.

Neobanks are just modern DSAs, in terms of cost nothing new is changing specifically for Federal.

Fi,Bharatpe,Jupiter etc though their bring in casa accounts, the impact on the business in federal scale is peanuts. These are just fancy words & no proof that they will contribute to business. Infact, if you take market leaders in this RBL & Yes. Despite having great digital franchise & alliances they never made money. Equitas has some early sucess but 100cr casa numbers are nothing at scale.

IDFC has cleared stopping all partnerships due to regulatory pressure on customer service, direct product competition, complaince etc.

Cards might help in boosting their fee income, but I’m unable to see roadmap for this number crossing 1.5s anytime soon.

COF has come down below 5s for the entire industry and not just Federal. Federal being a leading player in NRI deposits, they should have done better that others.

Investing in subpar banks will only make us poor. Lending is a beautiful business where the virtuous cycle will make you money from ROE + High BV Dilutions. lenders in vicious cycle will endup dilution at =<1 P/B & take away the ROE generated there by loosing on BVPS & price.

CSB is an interesting Bank to look at for sure. Please if you could share evidence, read-ups, anything that might support your statement, that would be great. Thank you

I have been accumulating federal bank since may 2020 and i would like to present my theses as to why I feel it a good idea.

Compared to other small private banks, this seems like the one that is most likely to become a large bank over time as

They have a great liability franchise, this is as good as the large banks and this is because of their niche in NRI deposits. This allows them to compete effectively with large and psu banks in the home loan market, and even though these loans have lower yields, they have lower RWA so the overall leverage can be high

They seem to have a good enough digital strategy. I don’t hear a lot from banks like City Union, DCB etc about things like account aggregators and fintech tie-ups, even though this is all small, I am confident that federal wont be eatten up by fintechs later

The have the ability and desire to expand market share, this is probably mainly due to the low cost of deposits. City Union strictly says they wont go for home loans, DCB is mostly focused on MSME’s but federal has a core of SME, MSME and home loans but is trying to brach into other things like credit cards, vehicle finance etc. They probably have the best runway

The credit underwriting is as good as the larger banks, the covid related slipages are very low

The have subsidiaries (life insurance, nbfc) and tieups (icici sec trading accounts) that should give them the ability to be a bank with a lot of the needs of either a retail or business customer taken care of. This is small but a good to have

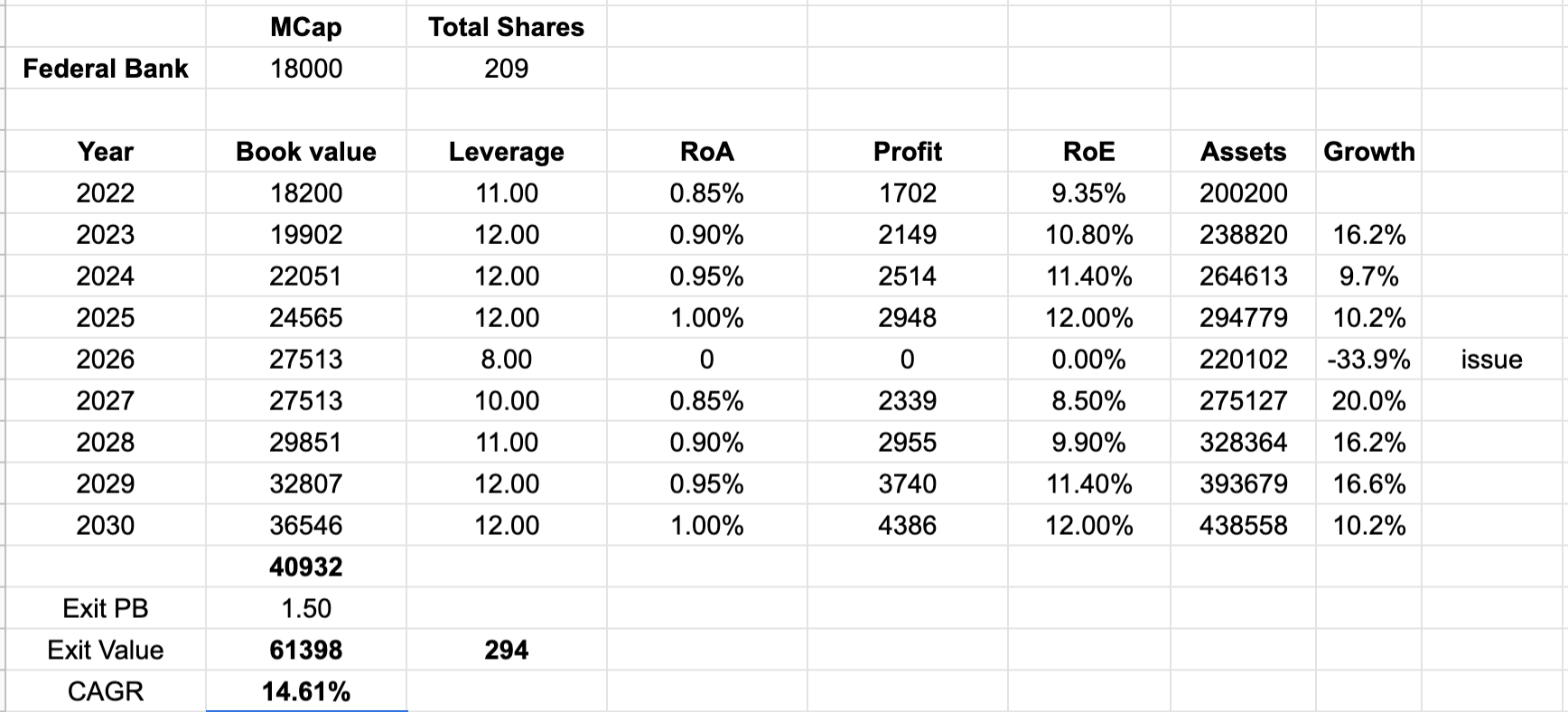

I feel a good valuation for a normal bank should be 1.5 P/B. My reasoning is, assuming the bank is in a terminal state and stops growig and pays out cash flow as dividend then, at a leverage of 15x and RoA of 1% the cash flow generated would be 10% a year, so risk free rate 7% + 3% equity premium.

For me cash flow = book * leverage * RoA = 15% / 1.5 (PB) = 10%

And i kept the risk premium as only 3% because the shareholder would be entitled to the book value which is cash. Also assumed leverage as 15 as a terminal state bank would not keep very high tier 1 ratios as they would not need to keep a growth buffer.

A rough calculation I made for federal bank till 2030 with an exit PB of 1.5 gives ~ 14.5% CARG stock price return, while assuming some economic downturn happens in 2026 and they grown only on they own profits and do not go for fund raising.

Federal bank is going in transtition phase. I have account in federal bank from 2012. Their IT part is top class and recently many fintechs are doing tieups with them. Usually we have two pools of pvt banks. One type HDFC, Kotak, ICICI and other is karnataka bank, KVB, LVB, southindian bank. Federal bank is still sitting in group two. If you look at their account holders it will be SMEs and ordinary people who may have money in their bank account but at the end of day they want to spend, they withdraw cash at ATM and go to shop and pay as cash. They dont have corporate salary account as a meaningful contribution. They are not earning much other than interest income. Even though they started credit cards, they have most of their branches are in place where they still transacting in cash and directly switching to UPI, skipping the card transaction era.

They are already heavily leveraged and their NIMs are average. This does not help them in growing at much faster phase. Even if they wish to do QIP, valuations are trading low that will not definitely benefit existing shareholders.

What i feel is structurally they are not yet ready to say “A Turnaround banking Story”

Disc: Had positions in past and sold 3 years back.

thats a good point, also since they are just starting a majority of their customers will be transactors and not rotator so the returns will not be great.

Here i agree but their strength is the NRI deposits that is sticky, the have a 15% market share in remittances, from my research i found most NRI’s use the deposits when the dollar is stable to earn an arbitrage in yields, but with the dollar strengthening there can be some outflows now

Optically but that is because they mostly lend to low RWA sectors hence they can afford the leverage.

I dont think they need capital soon but this is a risk of dilution.

I dont like terns like turnaround or next hdfc either. My only point was it is a bank that has good valuation comfort and even without valuation expansion should give reasonable returns over a decade.

It’s also mindset, i am pesismestic by nature and dont believe that banks with > 3x PB can grown fast enough to justify the valuations, since they are priced to perfection any disappointment can cause a negative reaction, at < 1x PB there are no growth expectations at all in the bank so any growth would be a surprise.

I’m not against growth investing but i think the next phase of growth will be in the SME, MSME and microfinance space since these are untapped spaces, middle class retail has way too mush competition and large corporate are actively deleveraging and not have access to bond markets so the growth will not be like before. Also with PSU banks getting capital, these two sectors will face intense competition as elections come close and the gov pushes easy credit, SME and microfinace is a mush harder area for PSB’s to reach

Hi,

wanted to understand the effect of the FedFina IPO on Federal bank. Currently the co holds 73% and wants to dilute 16% stake. The total issue size is about 2000crs and post listing valuation of 6k-7k crs (as per a MC report). So would the market cap then effectively go up and since that will take place, would the share price effectively go up?

Federal bank Q4 FY22 result and con-call, they have a family pension provision of Rs. 140 crores. So, i like to understand why it is Rs. 140 Cr while in FY21 the Pension plan cost was Rs. 90 Cr.