The recent results (Jun FY 21) show huge EBITDA margin expansion. Any idea why this expansion and how sustainable it could be?

I think there was no travel costs for MR and also no promotional costs due to lockdown.

Similar trends in other pharma companies.

Hi Was going through the last AR and found below statement:

Apart from the Positive growth in export (50% YOY) I was unable to exactly pinpoint the transformation that they had started in April 18. Does any one else have more details on this?

Price of the company has shot up over past few trading sessions. Company says that a brokerage house has given a report on the company and that might have caused the spurt. Any idea on which brokerage house has given the report? I’m unable to find anything online…

ANDA approval for Ofloxacin otic solution

Understand used to treat infections of the ear canal (google search)

FDC could be poised for a decent year ahead, especially next couple of quarters, due to pricing and RM tailwinds. Excerpts from the last concall point are suggestive that the management is looking to take the full extent of the NLEM price hikes.

-

Management points to the fact that Q2 FY 22-23 will see the full impact of the NLEM price increases (10.7% increase) with all old inventories getting used up now. FDC is especially a beneficiary here as >40% of their Indian portfolio fall under the NLEM portfolio. And considering market leadership of brands like Electral, this could be interesting to monitor

-

A second tailwind could be cooling off in RM prices. This should further give a fillip to margins (apart from price increase). FY 22 OPMs were lowest for a decade at ~17%, same consequently with ROCEs (15%). Average OPMs and ROCEs over the last decade are comfortably 20%+ and 20+ respectively. With margin/pricing tailwinds around the corner, could this depict a cycle bottom?

-

Last quarter results were very impressive in terms of sales growth. They delivered topline growth of 10% despite June 2021 being a COVID affected quarter with an abnormally large base This number was significantly higher (>40%) than June 2019, the last normal comparison quarter

-

Small amount of promoter buying going on in the stock, last in June’22. Company is sitting on reserves close to 50% of its market cap. Fundamentally still quoting at just above 2 PB which is low cycle valuations. In terms of sales also looks reasonable at 3x sales. PE not cheap, obviously because of base with very low margins

Technically also looks interesting (I am not an expert in technicals)

- Could we be looking at a reverse H&S pattern indicating a trend reversal? Closed above a major resistance of 275 and now breaking out into a new range. Above 30 WMA (tilting upwards)

Disclosure: I am invested as a techno funda position and am biased. This is not investment advice and I am still learning technicals. Do your own research before investing

FDC Ltd stock story -

India focussed maker of branded formulations and APIs

Domestic sales-83 pc

Export sales -17 pc(mostly from US - generics)

Top brands in India Mkt - Mkt share

Electral-oral electrolytes - 75 pc

Zifi-Cefixime - 24 pc

Enerzal-Energy drinks - 42 pc

Zifi CV- Cefixime+Calvulanic acid - 46 pc

Zifi O- Cefixime+Ofloxacin - 14 pc

Zocon- Fluconazole - 27 pc

Simyl MCT- Infant powder and oils - 34 pc

Amodep AT- Amlodipine+Atenolol - 7 pc

Company facilities -

Formulations plants at Sinnar, Baddi, Walnuj, Goa

Foods Plant at Sinnar

APIs plant at Roha

Top brands by yearly sales -

Electral - 350 cr

Zifi - 320 cr

Enerzal - 150 cr

Vitcofol - 86 cr

Zifi CV - 75 cr

Zocon - 54 cr

Cathrin - 59 cr

Zifi O - 53 cr

Simyl MCT - 51 cr

Amodep AT - 40 cr

International business - currently US dependent. Working hard to diversify into Middle East and Latin America with focus on Peru and Chile

Aspire to grow at 15-18 pc range (topline) for next five years. Bottomline growth may be better due better absorption of costs

Cash on books-aprox 800 cr

H1 is always stronger for the company due higher sales of energy drinks, electrolytes and antibiotics (in Q2)

As sales of Foods category+brands like Zocon grows, seasonality may reduce slowly

Management is aware of the fact that they have to reduce dependence on Electrolytes and Anti-Biotics. Now focussing on products like - Foods Division, Zocon, Opthal, Cardio & Diabetic products

Initiated a small tracking position

Inclined to add more if business performance improves / management is able to walk the talk

Buyback Announcement: @Rs 500 worth 150 Cr (CMP: ~390ish / MCap: ~6500)

Link: https://www.bseindia.com/xml-data/corpfiling/AttachLive/ae13aebc-63a1-45c9-a652-fa2403c70cf5.pdf

Disc: Invested (Portfolio sizing HERE)

Chanced upon the stunning buyback history of the company and couldn’t resist digging deeper into it.

Since the thread here doesn’t contain much recent information (except for Ranveer’s post above), adding some info for anyone interested to follow:

- Listed on both BSE and NSE

- ROE / ROCE are in the 10 to 12 % range but company sitting on lot of surplus cash. Return ratios ex of cash would be higher. About 20 % of PBT comes from Other Income

- Promoter holding is high

- Debt is almost nil

- LT OPM was always 20-25 % range but has declined in FY22 and thereafter to 14 to 17 % range. But Q1 FY24 has again shown a sharp improvement. Management says in H1 FY23 the RM prices were very high and more than offset the gains in the realisation and hence margins have dipped.

- LT sales growth is mediocre but has shown a sharp jump in recent times. Profit growth has also shown sharp improvement

- Consistent buybacks through tender offer route by the company but no dividend payments post 2020

- CFO to PAT is around 85 % in the long term. Okay but not great

- Last major capex was done in FY16. Some capex done in FY22 and 23.

- Working capital requirement is not high, CCC is around 3 to 4 months and W/C days are less than 2 months

- Company’s business can be classified into three divisions - formulations, functional foods and API.

- Key brands are Electral, Zifi, Enerzal, Zocon and Vitcofol.

- ‘Electral’ dominates the Oral Rehydration Salt (ORS) market with a commanding 70% share

- In FY23, Electral earned more than Rs.400 crore, Zifi Rs.350+ crores and Enerzal Rs.150+ crores

- 82 % reveune is domestic and 18 % is from exports

- In FY 2022-23, the growth came from anti-infective, gastro-intestinal and vitamins / minerals / nutrients

- Highlights and key developments in all the three divisions are mentioned in the Annual Report

- There is a seasonality in the business, which is dominated by ORS and anti-biotics. ORS sale begins from Jan and peak in summer (Q1) while anti biotics peak in Q2. Hence H1 is always stronger than H2. Company is making efforts to reduce this seasonality. The new initiatives such as ophthalmology, diabetic – cardio and nutraceuticals will reduce the seasonality.

- The new portfolio is also outside the NLEM which is another advantage.

- Expansion in Waluj plant will commercialize in Nov 24 since it takes around 18 months to get the US FDA approval for the plant.

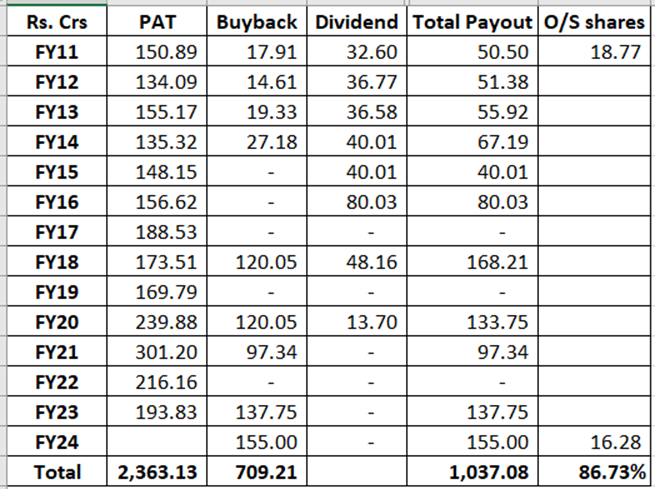

- Over the years, company has done several buybacks starting from August 2009. Since 2011 from where I calculated the numbers, total payout has been more than 40 % of PAT. This may not be great but the buybacks in the last 2 years have been even bigger, indicating payout distribution of almost 70 % of PAT. If this becomes the norm going ahead, it would be a big positive. Reduction in share capital is to the tune of 87 % in more than a decade.

- Cash balance as of Mar 2023 was Rs.800 crores with the company

- Promoter remuneration has been to the tune of 0.5 to 1 % of the sales, which is okay.

- In FY 2022-23, growth mainly came from anti-infective, gastro-intestinal and vitamins / minerals / nutrients

- The Company says in FY23, they completed the successful registration of I Lube Eye Drops - Polyvinyl Alcohol BP 1.4% w/v + Povidone BP 0.6% w/v in Malaysia. This marks a significant milestone for FDC as it takes its first step into the medical devices segment in Asia

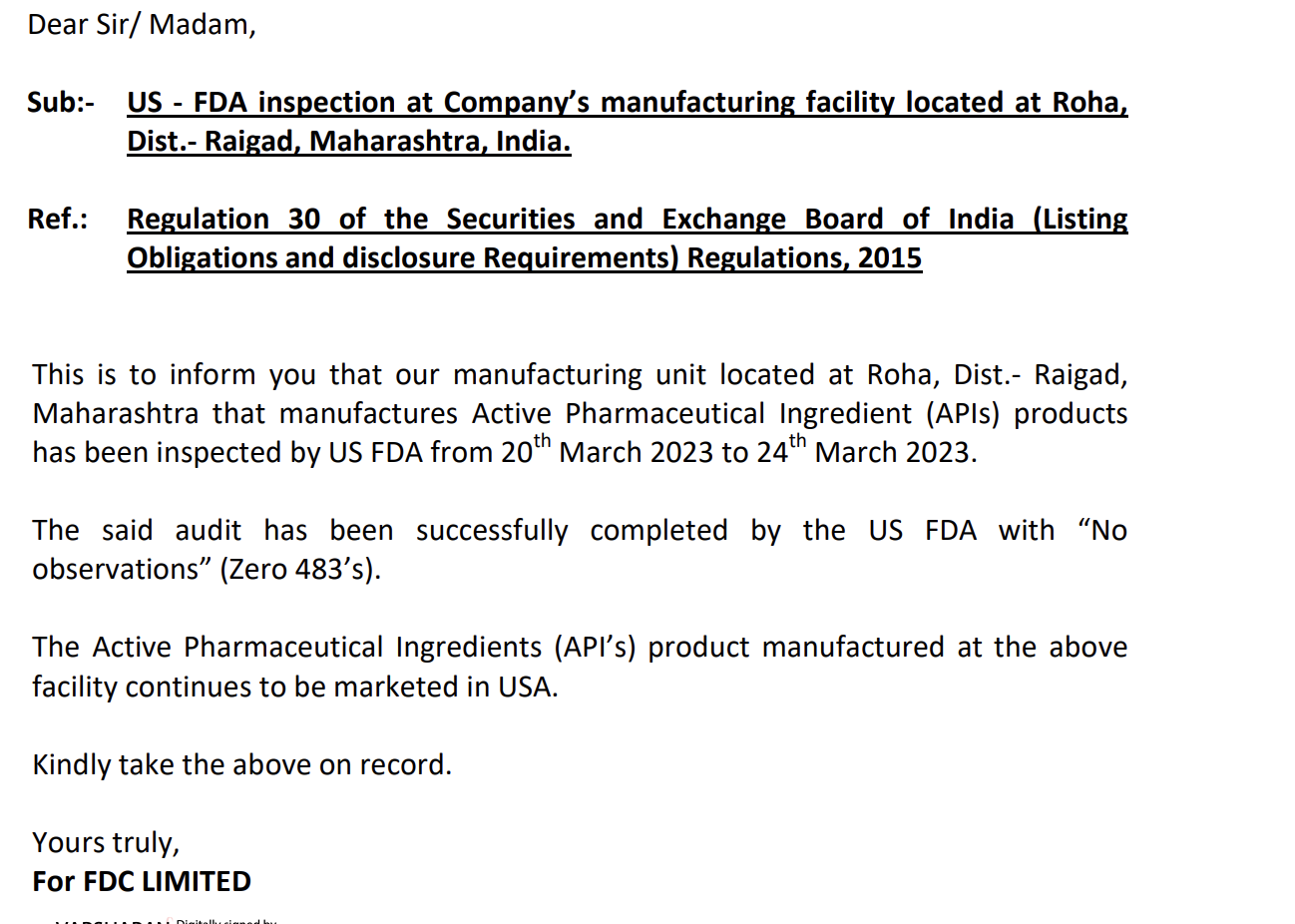

- US FDA recently completed inspection of Roha plant with No Action Indicated report

On the flip side, sales and PAT growth however has been inconsistent over the years. June quarter domestic sales growth was 5.7 % vs. 21 % in March quarter and 28 % in June 22 quarter. Company did concalls in FY22 but seem to have stopped thereafter.

Overall the company is a slow-moving ship but seems to be on the right track. Management is projecting 15-18 % growth in sales and profits in the next 5 years. This forecast is significantly higher than the historical rates. If it materializes, it could be a significant trigger for the business. Need to wait and see.

(Disc.: No positions)

FDC Q2 highlights -

Sales - 486 vs 445 cr

EBITDA - 76 vs 67 cr, up 13 pc (margins @ 16 vs 15 pc) Margins in Q1 were 23 pc

PAT - 70 vs 52 cr ( other income @ 27 vs 13 cr )

Sales breakdown -

India formulation sales @ 391 vs 369 cr

Export formulation sales @ 76 vs 57 cr

API sales @ 19 vs 18 cr

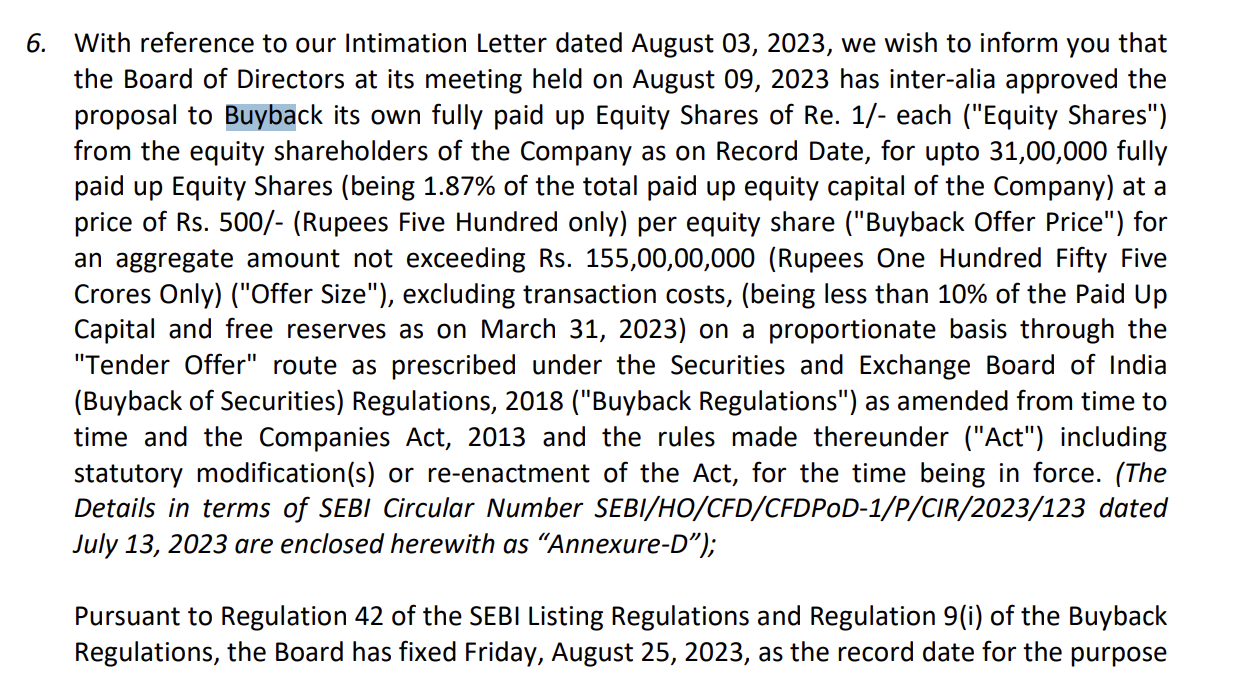

Board approved buyback of 31 lakh shares @ Rs 500/share - that amounts to a buyback amount of Rs 150 cr - a significant amount

Last 5 yr growth data -

Sales growth @ 13 pc CAGR

India formulations sales growth @ 13 pc CAGR

Intl formulations sales growth @ 17 pc CAGR

API sales growth @ 11 pc CAGR

India business -

4800+ MRs

9 brands with sales > 50 cr

6 brands with no 1 rank in molecule category

Electral has annual sales > 400 cr

ZIFI (Cefixime-anti bacterial) has annual sales > 300 cr

Enerzal has annual sales approaching 200 cr

ZIFI-X - Ceftriaxone injection - (cephalosporin antibiotic injectable ) launched in Jun 23 - doing well

In H1, price growth is around 4.9 pc with new product growth at 0.9 pc. Legacy portfolio’s volume growth has been flat. Company finally seeing volume growth in Oct 23

Have filed 2 ANDAs in H1

Company focussing on expanding in East India where it was traditionally weak. Making descent inroads in Bihar, Orrisa, WB

Also investing behind Nutraceuticals and Derma portfolio

Certain one off expenditures in Q2 led to suppression of EBITDA margins vs Q1. However, Q1 is always the strongest Qtr with best margins for FDC Ltd

Export business momentum remains strong, expected to remain strong

Export business is already profitable, capable of funding its own growth ( minus the R&D expenses )

To focus on Opthal business wrt US mkts as the company is strong in this particular therapy

Company has 6-7 brands that generate sales > 50 cr ( except for the top 3 brands ). These are the brands where the company intends to extract higher growth and make them into 100 cr + brands

Hence the company intends to not go for aggressive new launches. Focus shall be to grow above mentioned brands into bigger ones

However, company intends to launch brand extension of the a/m brands

Henceforth, the company intends to conduct half yearly concalls

Mum-Mum infant formula is a very promising brand and company intends to grow this aggressively

Regular maint capex @ 50 cr/ yr

Disc: holding, biased, not SEBI registered

A few points from the FDC AGM yesterday whatever I could recollect (E & OE):

-

Domestic growth - Low growth in FY24 result of NLEM price reduction, especially on Zifi range of products.

-

Rs.250 crore odd amount lying in capital WIP – a) For new Corporate Office. All the teams sitting scattered at various places and be brought together which will improve efficiencies. b) Also, there is capex for ophthalmic ear and nasal drop business. It has already gone live by now.

-

Capex – Annual maintenance capex is Rs.70 - 90 crores across all facilities, no other plans for major capex as of now

-

Growth break up in FY24 - (Something like volume growth - 0.3 %, Price growth - 6.4 %, New product introduction - 1.1 % = Total 7.7 %)

-

Prescription base increased from 58 % in FY23 to 60 % in FY24

-

Filings in USA – Current no. of Approved ANDAs - 8, new ANDA filed during the year - 1, plan to submit 2 more before Q3 this year

-

Not impacted by recent fixed dose combination ban in India

-

Ad spend - Has increased in recent years but Increases are limited to Electral and Enerzal brands

-

FY25 - Price hike not expected due to NLEM portfolio, have shifted strategy to volume and new product introductions. Results are already visible from April onwards

-

Capex - New ophthalmic line is commissioned this year

-

Capacity Utilization - across locations is around 70 to 75 % currently

-

Top 10 brands - Contribution in FY24 was 64 %, in FY23 it was 66 %

-

ORS - Market is expanding, growth is higher in liquid. Enerzal is no.1 brand as per IQVIA

-

Buyback - Will decide what is the most suitable mode of capital allocation (given that buybacks have become less tax efficient now)

-

No plans to monetize land

-

No comment on holding quarterly concall

(Disc.: Holding)

82% of FDC Sales are in India and 34% lower exports means export are hit. They have been forced to revise down the prices of Electrol by the National list of essential medicines and that is hurting margins. Depreciation from new office is also hurting margins. Stock looks headed back to the 2020 lows of 200