Faze Three Limited has Listed its equity shares on National Stock Exchange of India Limited (NSE), w.e.f. from the trading hours of Friday, November 18, 2022 on Main Board of NSE. Your Company is now Listed on both Major Stock Exchanges in India i.e. NSE & BSE Limited.

Things are improving on ground.

Similar voice was echoed by Fineotex Chemicals mgt who provide Textile chem to HT co’s.

Inventory levels hv reduced now n re-stocking is yet to pick up.

Fy24 looks far better than Fy23

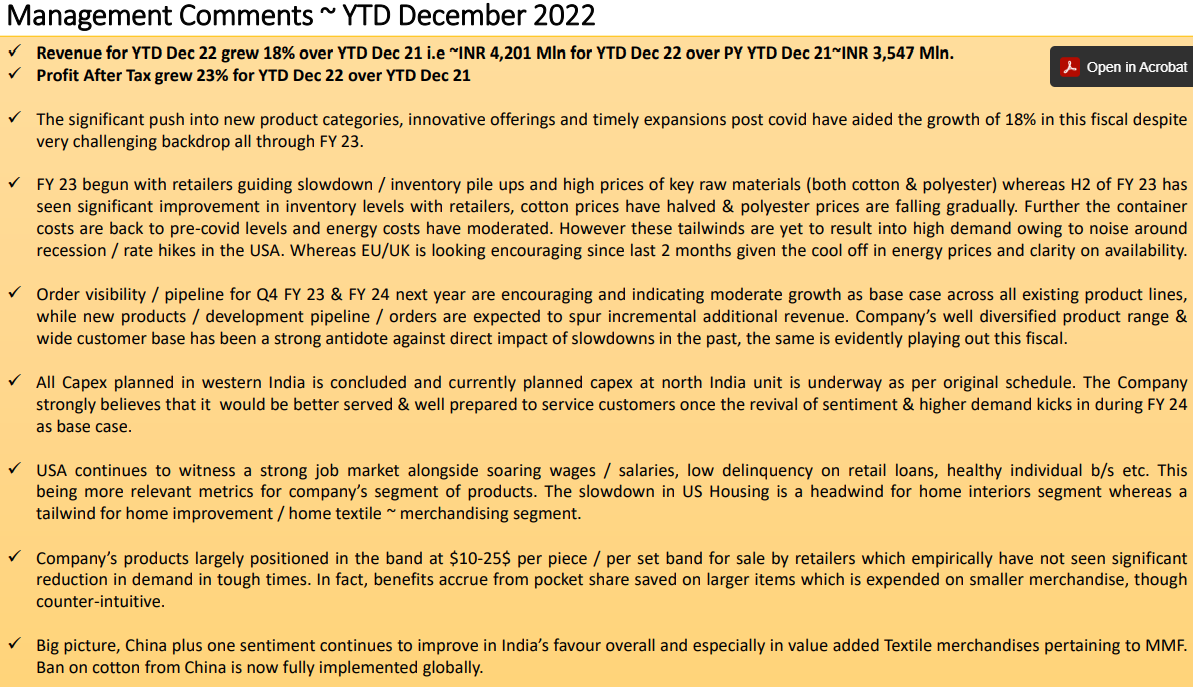

You got to consider the entire scenario. This is an export oriented company with 70% revenues coming from Europe and rest from US. Europe and US markets have been pretty weak over the last 1 year. Even in that scenario, Faze three has not shown any degrowth. Please check other companies which generate revenue from Europe. They would have shown significant degrowth because of soft market conditions. Moreover, Faze three has done major capex in the last 1 year and is expected to double its revenue from the current numbers in the next 3-4 years.

Note : This is not a recommendation to buy or sell the stock. Please do your own due diligence.

Just the way beauty lies in the eyes of the beholder so does valuations. At 13x trailing P/E someone might find it cheap and someone might find it expensive.

My limited point was on numbers. They are not stagnant.

We will have to see what price they set for the buyback. They are also delisting their other company Faze three Auto. Hopefully they don’t plan on merging both the businesses into one. Faze three Auto is a typical commodity play and Faze three exports seems more like a structural business.

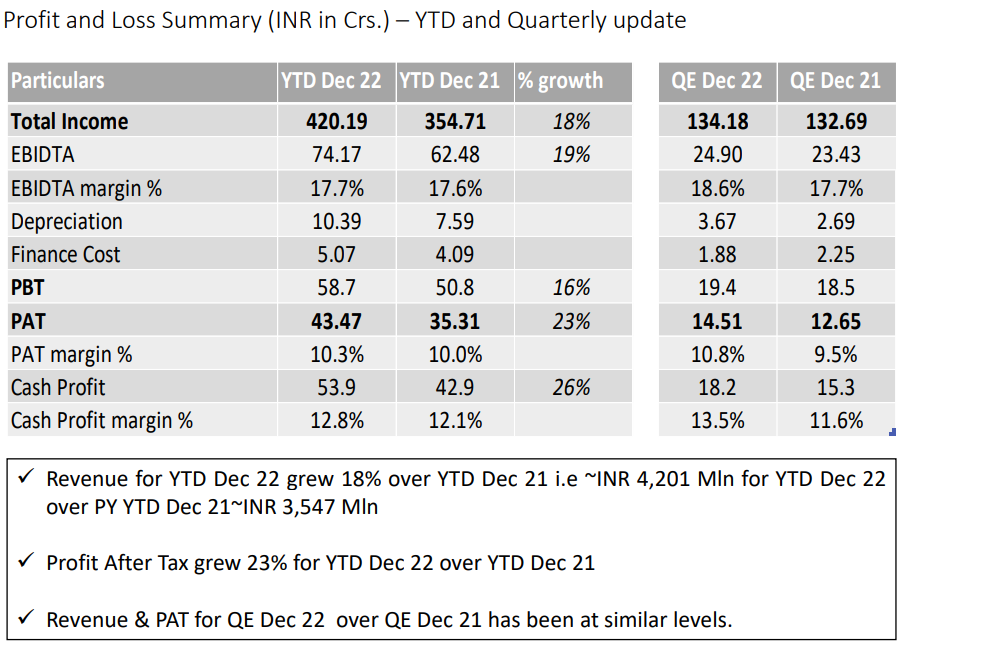

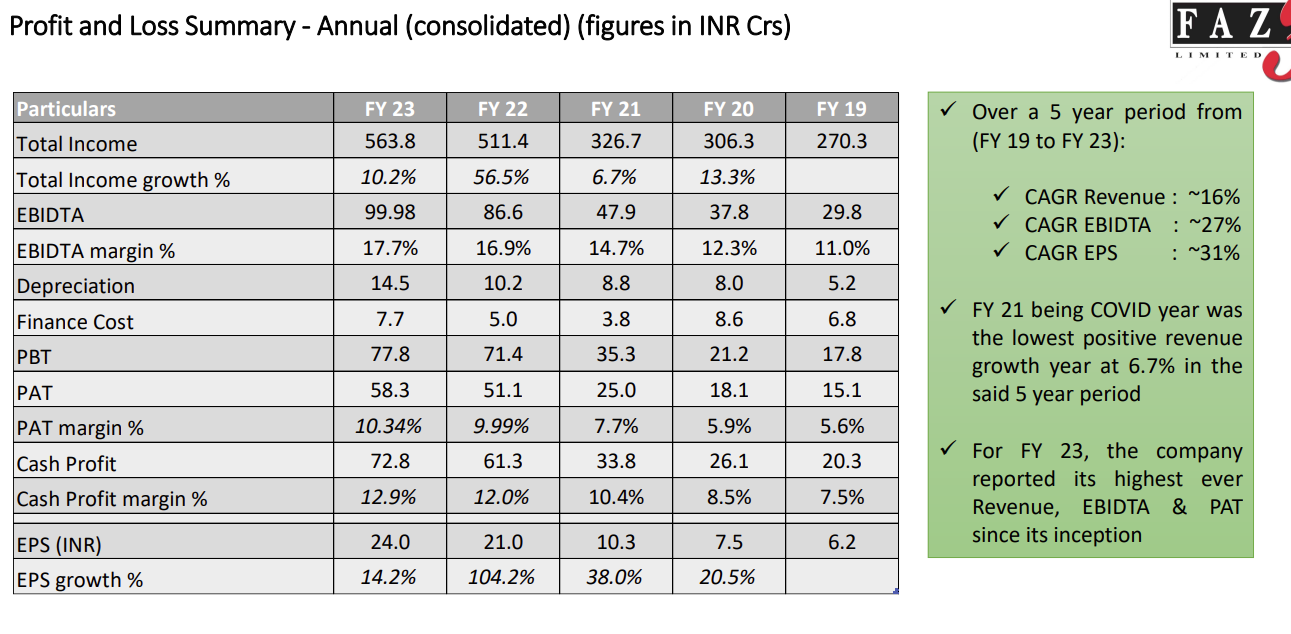

EBITDA margins are actually 15% and not 18 because there is an other income component of 5 Crs in the sales. Dip in margins doesn’t look good. Management should provide numbers on the volume growth because the topline fluctuates depending on the cotton/polyester prices. PAT margin has dipped slightly because of more depreciation post capex. There has been an upgrade in the ratings and the rating report stated that the co is inline to achieve a topline of 600 Crs for this year. This is ~8% increment on last year’s number. Last year’s PAT margins were slightly more than 10% but this year it might be less than 9.5% because of more depreciation. In that case the bottom line will more or less stay same as last year. Just 8% growth for a growing company doesn’t sit well. Last year’s growth was also just 10% . I hope these projections are conservative and we see atleast 15-20% growth on YoY basis from Q2 onwards. EBITDA Margins should improve significantly with more utilisation of new capacity. Let’s see how this story pans out and when can they double the sales and hit 1000 Cr mark on the topline with atleast 10% PAT margins.

The company received 27 Cr of incentive from Govt which i believe would translate into profit directly. Reported PAT was 57Cr last year which would mean ~35% of profit is coming from incentive only and if this incentive gets discontinued which I believe can happen in any budget cycle can significantly impact the margin/profit for the company

wanted to check if my understanding is correct as the company is currently looking at 21PE which might actually be 35-40 if this part gets removed/impacted

These incentives provides a cushion to the companies to reduce their margins & sell products in the market at a competitive prices.

Assuming the worst case scenario (which seems highly unlikely) that these incentives will be discontinued ,then the co’s would still be able to maintain their profitability by inc. their prices or increasing their cost efficiency.

By the time this happens, the scale at which these co’s would be operating will be totally different .

So, that does not mean that ~35% or any % of profits would be wiped out.

Everytime you exports products you have to pay duties to Government of India.

Government uses duties to discourage exports. For example let us say we had bad rainfall and agricultural output comes down. Duties are used to prevent exports of whatever little is produced as this will lead to bigger shortages in India causing price rise or inflation.

Government wants to encourage textle exports not discourage the same. So the duty drawback is the government giving back or refunding duties to a textile exporter the he/ she has already paid. So these drawbacks are here to stay.

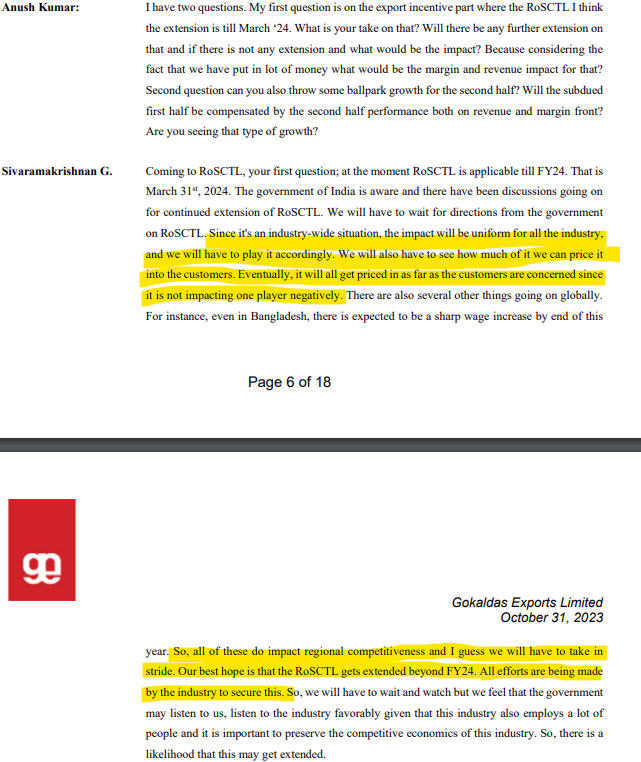

Question was asked in similar lines to Gokaldas management during Q2 concall. Management indicated that it will get priced into customers to what ever extent possible as it will be industry wise phenomenon and also depends on regional competitiveness compared to other countries like Bangladesh. Govt of India may extend the RoSCTL benefits beyond Fy24. Below is the transcript snippet from the Gokaldas concall: