One needs to be careful while drawing conclusions from this data:

Are you sure the company uses only Mumbai port and not any other port in India

This is import data (not export data). Which means this would some portion of raw material imports. If company has high inventory of raw materials end FY22, why would they import more in current quarter.

Good results. They hv managed to maintain their topline and margins even in this tough environment.

But definitely there is some impact on the demand.

They commissioned new capacity under Floor covering & rugs segment during April month. But could not see any contribution from it in Q1.

Otherwise topline growth could have been far better.

Lets wait for the mgt commentary in the presentation.

If anyone attended the AGM today then please share notes. It would be interesting to see what the management thinks about future growth prospects given that Europe is reeling under the effects of recession right now.

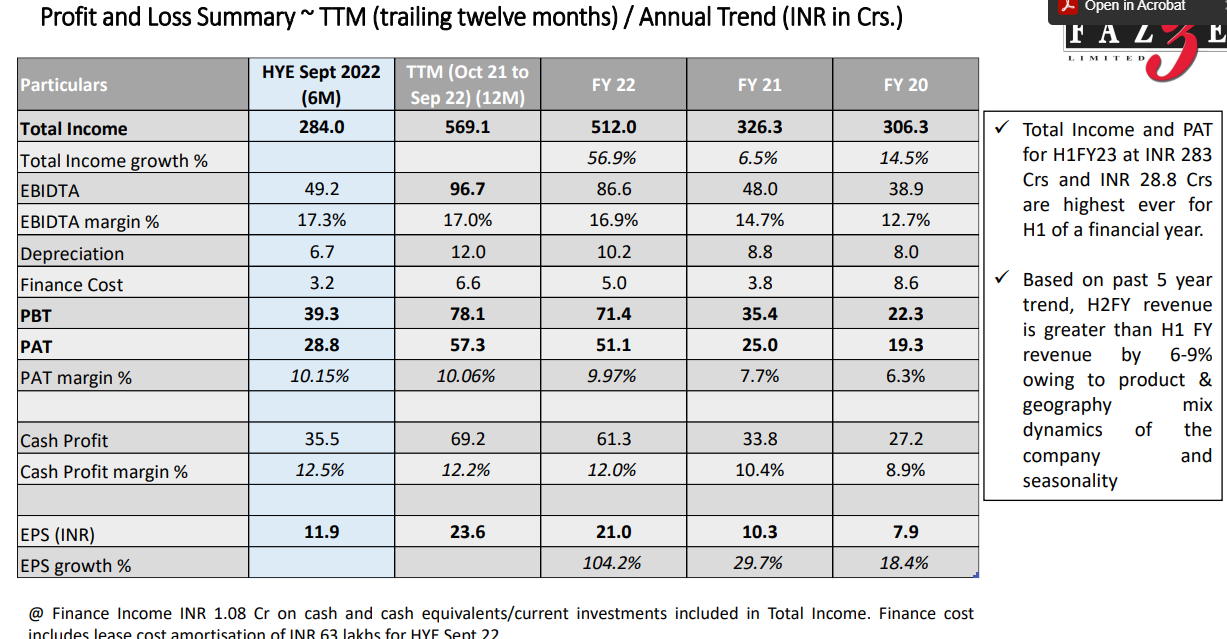

Achieved growth of 50% in revenue and 100% in Pat

Major capacity expansion was undertaken , considering we would hit peak capacity by 2022.

Made significant addition to the Mgt Team across functions over last 18 months to get us ready for the next big run.

over 95% of business comes from existing customers across different product lines and regions.

Have added many new products and lines in FY22 which is very satisfying and shall reap good rewards in coming years.

Questions from Ayush Mittal

Q.Visibility to double revenue from FY22 BASE?

In last 4 years co. has doubled its revenue.

Similar trends of the last few years is expected going fwd in next 3-5yrs.

All the building blocks are in place.

95% business come from existing customers and these are large retailers and the scope to deliver to them is quite large.

Capex

100crs plan has been disclosed and 65% has been undertaken and balance will be undertaken in next 12 months . All this expansion is brownfield.

Once this capex is over we will be able to 3x of our revenue.

Since we are multi product, multi factory, multi raw material kind of set up so there is no standard measure of capacity.

We had similar situations 3 yrs ago when we said that with existing capacities we can double our revenues and we delivered on it.

China+1

Its a reality.

If we go by the standard vision statement of the largest retailer of US.

They intend to more than Triple their purchases from India.

To quantify the largest retailer has intend to buy $10bn from India by 2027 from current $3bn.

US Inflation

Jobs and wage market is very healthy right now.

We have gone through 3 recessions in 2001,2008 & 2020 also. our mgt has gone through those last 3 recessions.

But the HOME IMPROVEMENT segment or merchandise segment where we belong generally do not see steep decline as compared to home interior or housing sector.

US unemployment is all time now

Not seeing any major issue there.

As against very high growth we will see moderate growth in this year.

On cancellations of orders

We didn’t face any cancellation of orders due to made to order business model.

We might not see high growth as of last year which was around 50-55% but we will see moderate growth.

Margins improvement- Operating Leverage has played out in last 2 years

Better product mix

Going fwd we don’t see any reasons why we should not sustain and grow margins as soon as our capacity utilization improve.

Margins are not there bcoz of China+1 but bcoz of inherent advantages of our business model.

Customer addition- We are yet to start business with some of the large retailers of the world. There are almost 5-10 large retailers across US with whom we are yet to start business with.

Thanks a lot! Going by the management commentary it seems that they will clock somewhere between 625-650 Crs of topline and should be able to maintain their operating margins around 15-16%. Seems like Q2 and Q3 could have similar numbers like Q1 in terms of topline and PAT with slight deviations and Q4 is always the best Quarter for them based on historical trends.

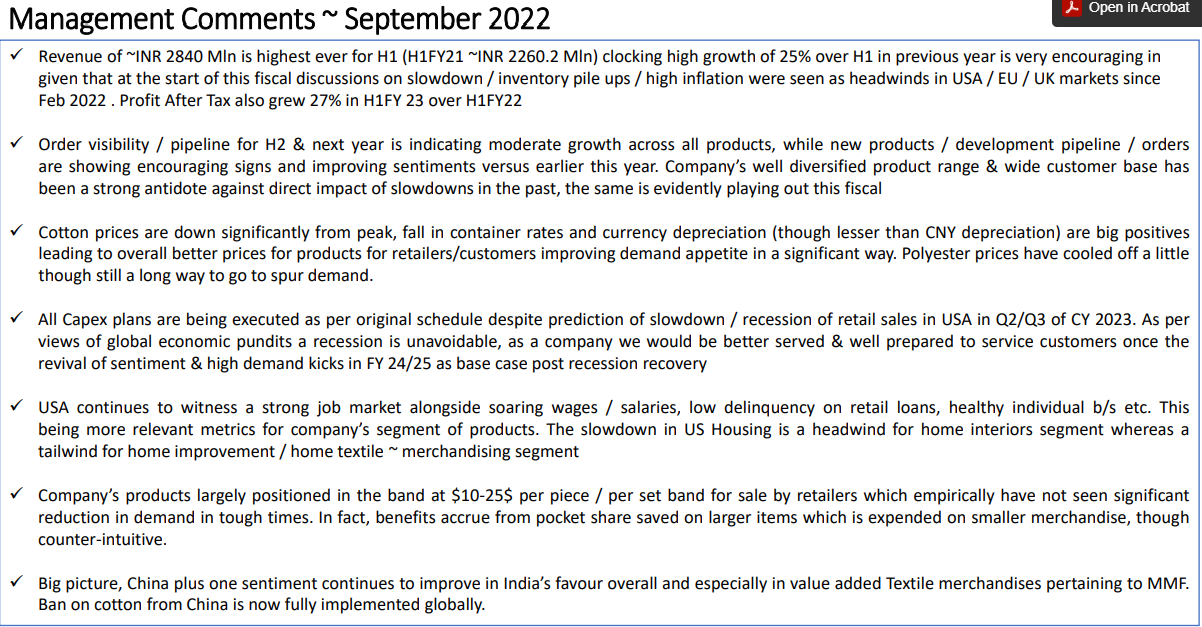

All Capex plans are being executed as per original schedule despite prediction of slowdown / recession of retail sales in USA in Q2/Q3 of CY 2023. As per views of global economic pundits a recession is unavoidable, as a company we would be better served & well prepared to service customers once the revival of sentiment & high demand kicks in FY 24/25 as base case post recession recovery… from inv presentation

Results seem to be ok. With margin improvement QoQ

Good thing is healthy CFO and cash balance to the tune of 100crs.

Currently the industry is going through one of the worst times (Hope it doesn’t get more worse than this)

If they are able to maintain margins and have strong bal. sheet during one of the worst phases, then they should come out with flying colors when the tide turns.

Result seems pretty good considering the current headwinds in the US and European markets. Welspun, a bigger player in a similar space has posted poor set of numbers. Specially the home textile segment took a beating. As for Faze Three, balance sheet looks strong and margins are stable too. Need to watch out the next couple of quarters over growing fears of recession and slowdown specifically in US and Europe.

Company said in Investor presentation that growth will be moderate in FY23 due to Geo Political issue and high inflation. I believe this is the reason of the correction because 90% of the revenue comes from USA and Europe.