Good results in Q4.

878d23ae-c161-4850-82c3-cf47b8ad89a6.pdf (bseindia.com)

Turning into a promising story, especially if they deliver on capex.

Disc - invested in last 30 days

Good results in Q4.

878d23ae-c161-4850-82c3-cf47b8ad89a6.pdf (bseindia.com)

Turning into a promising story, especially if they deliver on capex.

Disc - invested in last 30 days

The revenue and profit growth looks outstanding, however, the cash flows are very poor, even when profits have increased 100% YoY. Any comments on this?

Given the growth they’ve seen, a rise in receivables and inventories sounds about okay. Other current assets is related to other receivables, which would have again increased due to growth in sales. Annual report might give further details.

Investor presentation is quite helpful to understand their business evolution and future plans.

Inflation also plays a part. Large inflation in RMs post Russia-Ukraine war across the board: cotton, oil prices having an impact on MMF yarn, etc. So the Working Capital goes up disproportionately since the new stock and receivables is at much higher prices. Would expect to see some positive free cash flows hereafter.

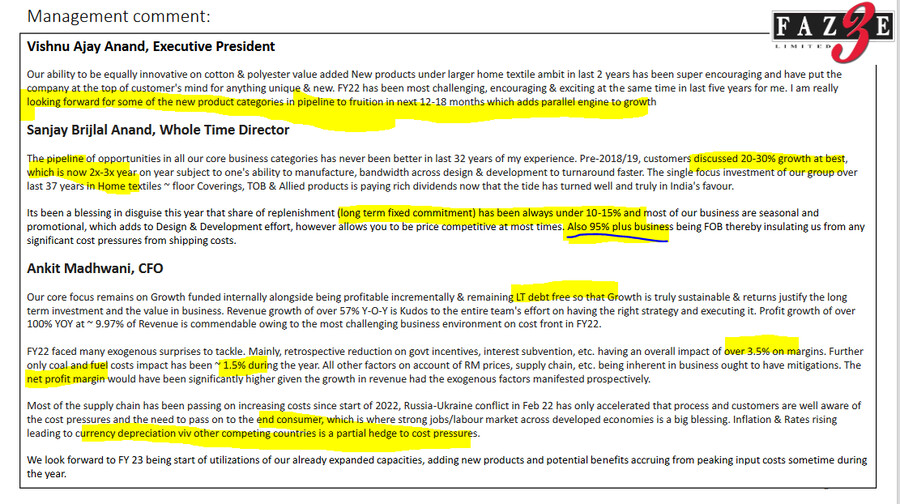

The resilience of the business due to the seasonal rather than replenishment nature of orders on show this quarter. By and large a good margin performance even when large peers who do replenishment business struggled to mantain margins this quarter.

Wonderful set of no’s by FAZE 3.

Margins were maintained although they are down QoQ due to higher other expenses but still they did a commendable job if we compare them with other textile giants.

Whats more interesting is mgt commentary in the presentation.

-95% of the contracts are FOB so they are immune to high shipping rates.

-Long term fixed commitment orders are just 10-15%, allowing them to be cost competitive

-Customers discussing about 2x-3x YoY growth

.-Expansion plans on track and to be funded via internal accruals.

Interesting times ahead!!!

One que looking at FY22 results (Consolidated Cash Flow statement) in case anyone in this thread has been able to get their head around:

Last year (FY21 - y/e Mar 2021), company’s net proceeds from borrowing (Borrowing - repayments) were at 37.79 Crores, and this year (FY22 - y/e Mar 2022), company paid interest cost of 3.95 Crores (so that’s 10.45%). Given this information, why did company choose to invest 10.49 Crores in Fixed Deposits and 10.11 Crores in Quoted Investments (See this years ‘Cash Flow from Investing Activities’ section) instead of using these to reduce their overall borrowing by roughly 20 Crores? This year company has borrowed 66.28 Crores (Net Proceeds from borrowing as per Cash Flow from Financing Activities).

This question adds further weight when you see that company has earned interest of 2.3 Crores this year over last year’s Investments in FD of 38.99 Crores. So that’s about 5.89%.

Essentially, invested money at 5.89% (in Fixed Deposit) while paying approx 10.45% in borrowings. Something doesn’t add up here.

I have one possible explanation in mind, but I don’t want to voice them out in public here, instead would want management to clarify reason behind doing this first.

Has anyone been able to get their head around this? If not, can some existing shareholders send an email to their CFO/Investor Relations team to see if they are able to get any meaningful response?

Disclosure: Not invested, researching!

First of all the point that co. paid 3.95crs on 37.79crs is incorrect. Total borrowing in last Fy was 91.35crs on which they paid 3.95crs, which works out to be 4.32% only.

In FY22 the debt was 157crs on which they paid 4.99crs as interest cost - 3.17%

So, effectively co. is earning more by keeping money in bank rather than paying off debt.

Moreover they are long term debt free, this 157crs of debt is wc debt on which they get several incentives by the govt.

Thanks @Aditya942000

Could you please share source for these numbers?

The reason I ask is, interest rates of 4.3% or 3.2% seem to good to be true even after adjusting for interest equalisation levy provided by govt given even the best of banks have their cost of funds around 5% and even large institutions usually borrow around 7-8% at the minimal unless ECB or private equity.

Even large institutions are not able to secure lending at these lucrative terms as clearly people could borrow and then park those monies in fixed income instruments and make money on arbitrage.

Some other questions I am trying to wrap my head around so far (I have just started my readings, excuse my naivety)

The industry seems very cyclical in nature (given these are usually not fast running items, people buy them once and then they usually last for at least a few years before replacement). Given this, are these boom times and hence low valuations falsely represent good margin of safety?

What if scenarios (In the interest of protecting downside)

China (deserves its own section!)

– What if China decides to reverse its Zero CoVid policy rather publicly and it is taken as a positive political development by developed nations.

– Even with Zero CoVid policy, what happens when Chinese lockdowns come to an end? What happens when they start selling even more cheaper goods to woo importers in order to jump start their businesses? Will importers really say no and still choose India?

Pricing Power

– They deal with really large buyers (reputed names), do they really have pricing power? And if they do, why was the EPS really languishing between Rs. 7- Rs. 8 from mid/late 2018 to early 2021?

– What if due to cheap products (once Supply Chains ease up and/or Chinese lockdowns end), they (reputed brands from whom Faze3 derives majority revenue) try to squeeze Faze Three or choose to move their business elsewhere?

Political Environment

– Due to inflationary pressures, can govt puts export duties on textile? Especially as cotton prices have been on an upward swing for a while and they still continue to? Similar to what’s happening with Steel, Sugar and possibly more commodities in near future?

Valuations

– Best Case Scenario: Even if business grows its earnings at 50% next year (Taking one year ahead instead of 3-5 years ahead as there are lot of variables/what-ifs and predicting too much further ahead seems very difficult)

Great questions Deep!

I wouldnt read too much into this. The borrowing is all working capital borrowing (which is usually at lower rates since it is secured) and it gets a govt subsidy on interest, it wouldnt make much sense to fund the WC via equity when there are capex plans. It wouldnt make sense to pay off this low cost debt and then borrow more to fund the 80 cr capex at higher rates.

I think this is a concern, clearly looking at the numbers of the listed players; the last 2 years were abnormal in terms of demand. Bullwhip effect means that any deviation in retail sales would cause an even larger effect the further back in the channel you go. It is possible that we see a reverse bullwhip going forward given the high level of inventory on retailers shelves. What in my view insulates Faze Three to an extent from this is the seasonal/promotional nature of the orders vs peers; but still it is logical to assume that if there is extra stock with the retailer, fresh buying will be lower. However, these are all temporary cycles and last a few quarters at the most.

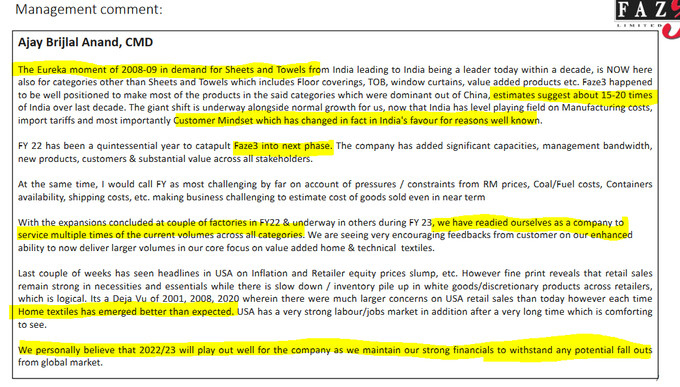

China is the biggest factor. The hypothesis is that the boom in Faze Three Sales started in FY20 before Covid due to trump tariffs which levied an additional 25% duty on the products that Faze Three exports. This made India competitive vs China. Therein is the crux of the story. What essentially an investor betting on is not retail sales in the developed world increasing quickly, but rather a shift in Market share from China to India in Faze Threes categories led by increased competitiveness. We can see the same happening in the earlier part of the last decade in towels/bedsheets. Sales for Indian listed players (Welspun, Indo Count, Trident) exploded despite low retail sales growth in developed markets. As long as that happens, a lot of wealth is there to be created. One only need to look at the stock price appreciation of Welspun, Trident, Indo Count from 2011-2016.

To me that looks cheap, doesnt it? If we annualize Q4 results (which still had an impact on margins due to inflation), the ROE comes to ~25%. I think we would really struggle to find a company with a 25% ROE, growing earnings at 35-50% available at 10-11 PE.

Faze Three, as a business is heavily dependent on totally external factors (relationship between US and China). There can be uncontrollable headwinds. Though I am yet to read more into Towels/Bedsheets story. Some readings in this direction:

Lastly, on valuations:

The problem is not yet expected RoE, the concern is with predictability of this RoE given extreme dependence on the uncontrollable factors. As a result of this, I would expect a better margin of safety in pricing.

Other way to look at it is, currently the business as next few quarters worth of orders in hand, post that (say the cotton harvested in September) the RM prices will really start to show effect unless cotton prices go down (but given China to India preference, and the competitive nature of this business, suppliers are struggling to get Cotton and Cotton Yarn, hence expecting prices to come down drastically may not be a viable thing, but I am no expert in commodities, and have no idea.). At that stage, the RoE will likely take big hit and if elevated prices continue, the risks of export duties by Indian govt will loom over the exporters continuously.

All this, either inclines me move this business to “Too Hard Pile” or demand a higher than normal margin of safety, say a yield of at least 1.5x of otherwise expected yield of around 10% from equity investments.

As for if you’d find other business at such RoE numbers, that’s subjective based on one’s research, understanding of businesses, predictability of returns, preferences on position sizing and what not.

Yes i agree, I think any movement on trade tariffs is a far bigger risk than Covid, inflation, etc since thats a long term headwind. As such its a key monitorable.

I would say look at the numbers of some of the peers. The cotton prices are already at absurd levels and it is showing in the margins of peers but not Faze Three’s. There is something in the business model that insulates the company from too much RM fluctuation: that seems to be the seasonal nature of orders.

I think valuation is in the eye of the beholder honestly. At 10-11x PE one isnt paying much for future growth. I dont think anyone would buy such a company to make 10% returns. The hurdle rate on the investment needs to be far higher: 25%+ imo to justify the risks taken. End of the day the investor has to be able to justify if they think the business can scale revenue and profitability for eg 3x from here for it to make sense.

ICICI securities have mentioned in there report on Faze three that “the company indicated that there main raw material is polyester based (40% of total RM) which has seen lower inflation as compared to cotton. Also the company uses coarser counts of cotton where the prices has not gone as high as the prices of finer count cotton”

IDirect_FazeThree_Q4FY22.pdf (434.6 KB)

Just an update on the cotton scenario - There is no issue on the availability of cotton, even mills hv started cutting down on their production levels, not due to unavailability but due to lower demand and lower spreads.Production is already down by 15-20% and if situation persist the cotton prices would be impacted.

Secondly,prices spiraled in Q4FY22 due to roll over of contracts by the traders and those contracts were top be settled in Q4 but now they hv been deferred till July month, which caused spiraling of prices.Once these contracts are settled it will lead to some cooling of cotton prices.

Third- Currently in India, cotton sowing is going on & looking at the current prices there should be higher sowing of cotton this year. Given the monsoon forecast to be normal, higher production will also lead to cooling off in prices.

Same it actually seems that the cotton prices have peaked and they will start to come down.The major RM affecting the textile industry is actually power and logistics cost I believe going forward. Coal prices and oil prices might remain elevated for the coming year globally once china starts to come back online .

Company did Rs51crs profits. Conservatively just extrapolating 4QFY22 profits of Rs16crs, the company should do greater than Rs64crs profits in FY23. The stock is trading at 12.5 P/E FY23 at the current market cap of Rs802crs

Disclosure: Invested

Not to mention this was during a time period when textile industry was facing immense pressure from raw material inflation. If these fade as most analysts are predicting will happen by the second. half of this financial year. Profits can be even more.

Welspun fell by almost 60% in last 5 months and has been the market leader in home furnishing category. why do you think faze 3 will do well or has a moat over welspun or trident?

I am also aware that this business is in a superstar portfolio and soic recommends the pf study of that superstar. However i am not able to find any moat as I am in the garment export myself and the prices of raw material is going through the roof. Add to that the impending recession in us is very real.

Basically Textile is going through headwinds which will drag margins & sales down in coming qtrs, although cotton price peaked & consolidating , as export will be down for next 2-3qtr bcoz of USA, EU inflation issue, Geopolitical issue , Fed rate hike , we can expect hammering in stock price as well, Also the sector is kind of commodity so clients can change vendor frequently, pump & dump game with the help of social media is common phenomenon now a days , one must do their own research before trapped in fomo, long term story may be intact , Disclaimer not invested but tracking

The headwinds due to inflation will be offset by revival of hospitality and hotel sector which is evident by record flight travel. Faze three supplies high end/luxury products- sheets, pillowcases, blankets, carpets, curtains, dining room tablecloths, cloth napkins to top hotels in US.