Sqs Bfsi Quarter 3 results will be out during January 25, 2019. Usually Q3 is subdued due to seasonal holidays ( Xmas, year end vacation). I can only make a wild guess of EPS in the range of ₹ 6 to ₹10. Let us wait for the results.

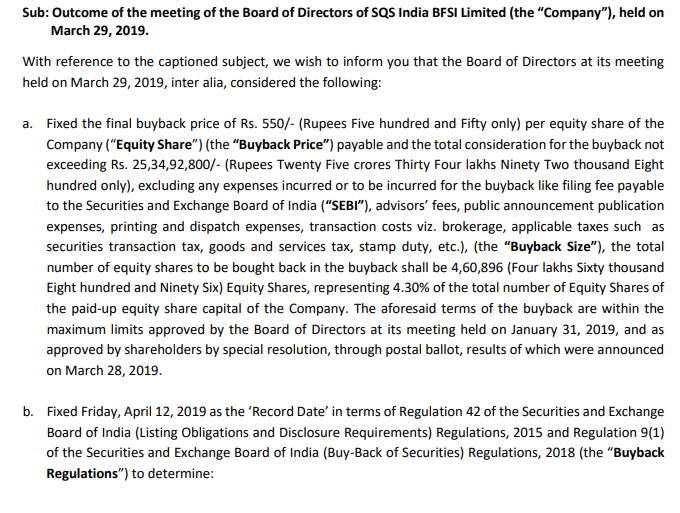

Dear sri Krishna bhutra & Rohit Balakrishnan, Sqs Bfsi has announced a proposal for buyback of shares along with Q3 results on January 31, 2019. Terms of buyback, promoter participation, price etc will be known on 31 January. Rajasthan global securities holding 4 %, has repeatedly been demanding buyback, where in promoters do not participate, to hike their stake.

As of now, 1) buyback will increase EPS, share prices & even promoters stake.

2) company saves on DDT, HNI saves 10.4% tax on dividends exceeding ₹10 lakhs

3) LTCG /STCG plus STT is payable by investors on buyback.

Your views please.

1 Like

Q3 FY19 results for SQS India BFSI were not that great if we look at headline numbers especially growth. Margins were hit due to forex losses, however almost all of them were notional losses. Adjusting for forex losses, the margins were quite good- driven by cost control and also increase in the share of offshore in the overall mix. Company has announced a buy-back at upto INR 550/share. The promoters are not going to participate in the buy-back. The buy-back is for ~ 25 Crores Some of the notes from the call:

-

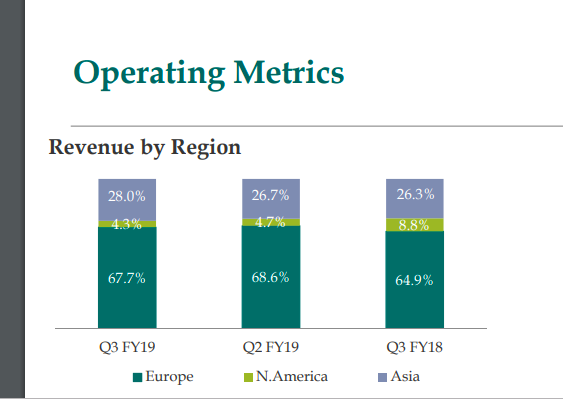

At the moment, the company gets ~ 58-60% of the revenues from the parent. Of which direct are around 18% and the indirect is remaining. By indirect revenues, it means that the sourcing is done by the parent and even the client management etc is handled by them. The delivery is done by the Indian listed entity. The reason for not moving indirect to direct is these are old contracts with customers and they don’t want to change them. SQS India BFSI intends to take this share (direct + indirect) from ~60% to 70-75% in the coming quarters

-

Company also looking to get into new lines of services such data management, RPA . These new lines of services contribute ~ 9% of revenues at the moment. Expect them to double in the next few quarters

-

The model of distributed agile is getting more traction and as a result expect offshoring to increase. This would also lead to improvement in growth from mid-single digits to perhaps double digit growth which was there few years back

-

Offshore mix at 52%, optimum is 60%; as the management see

-

Expect Q4 FY19 to be similar to Q4 FY18, if not better.

Discl: Invested in SQS India BFSI.

I am a SEBI Registered Investment Advisor (INA100008832) and it is fair to assume that I and my clients have a position in the stock and thus my views maybe biased. This is not an investment advise to buy/sell the stock, please consult your investment advisor/do your own research before buying/selling a stock.

These are my notes, and there maybe errors in my interpretation or noting down the management’s comments. Please use your own judgment

5 Likes

Hello,

I have a few questions regarding the buyback.

-

Why was shareholder approval needed for the buyback.

-

Would the promoters also vote on the buyback proposal.

-

How likely is it that the buyback goes through.

Thanks

Dear Rohit Balakrishnan, I was on listening mode during Sqs Bfsi con call & was very happy to hear your pleasant voice, eliciting answer to queries. The MD, also mentioned that due to paucity of time, further queries can be routed through Diwakar pingale of Christensen IR, for replies from the management. Some of the answers I would like to know

- Growth has been subdued for past 3 years, on being asked on this point by an analyst, MD expressed surprise. So do you expect growth in revenues in coming 5 years? MD said growth should surge in the next 2 to 3 or 3 to 4 quarters ahead

- quoting Neelson hall, specialized testing market is expected to grow in double digits around 15 % ahead

- USA market, which constitute 50 % of global market, the MD is talking about a minimum of 10 million in revenues to be achieved in next 2 to 3 quarters

- so I expect a surge in growth & Profitability of Sqs Bfsi in coming 5 years & remain invested for the long haul

- So Dear Rohit Balakrishnan, keep us updated on Sqs Bfsi. Thanks & regards.

1 Like

Hi sarathakkumar, 1) Buyback requires shareholders approval & sebi approval 2) 4.30 % of paid up capital of the company is being bought back at ₹550 per share for around 25 crore on a proportionate basis 3)promoter has declared their intention not to participate in the buyback & hike their stake from 53.72 %.

4) promoter will vote in the buyback proposal & since they hold 53.72 %, even if others object the proposal will go through.

Sqs Bfsi, Name is being changed to Expleo solutions. Expleo is a Latin word, with several meanings like complete, satisfy, fulfill, discharge of duties efficiently etc. In fact in the last concall, MD hinted at name change.

1 Like

Assystem technologies SA France, delisted Sqs parent & india listed entity Sqs India Bfsi, is in the process of being renamed as Expleo solutions, at the behest of Ardian to create a global behemoth with focus on software testing, end to end solutions.

3 Likes

Excerpt from latest investor presentation

Revenue from N.America has fallen by 50% y-o-y. Was there any mention on the concall why this has happened inspite of the investments in US market?

Yes, due to Ramp downs, this has occurred. However under the umbrella of Expleo solutions, the brainchild of Adrian, Expleo is to ramp up the entire spectrum of of software testing solutions, QA, managed services & consultancy across the entire spectrum of the business & industries including engineering, automotive, aerospace, pharma, Railways & industrial segments, worldwide.

However the Indian entity would exclusively focus on Bfsi segment. As of now, the buyback at ₹550 is bound to fail, as share prices may well go beyond ₹550, levels & the company may give an attractive dividend instead!

In my view, share prices may test, life time high of ₹1260, over next few quarters & may test new life time highs.

Sqs Bfsi is likely to show Chinese bamboo tree growth patterns over the next 5 years. Growth has been stunted from 2016 to 2018 & major growth is yet to take place.

Current phase looks like an inflection point, from which, Chinese bamboo patterns of growth looks likely over the coming 5 years. These are my personal views & iam heavily invested in Sqs Bfsi for the long haul. Dear Rohit Balakrishnan, Analyst, tracking Sqs Bfsi & also his website vruddhi capital, will be giving expert views on Sqs Bfsi, in the course of time.

Digitalization will propel growth in software testing & QA business, Managed services solutions & Management consultancy.

Robotic process automation, Blockchain, cloud computing, IOT, Data analytics, Artificial intelligence, security surveillance & testing. Future prospects & potential for Sqs Bfsi, looks promising.

Any idea of the record date for the buyback if it has been announced.

Hi Rohit Record date has not been announced yet. Company may rush through the process, at maximum speed, probably before Q4 results, in April last week. Q4 results are anticipated to be good & buyback may find no takers after Q4 results. However, I also see the possibility of Sqs share prices exceeding ₹550 levels, in a matter of time & buyback may fail & company may give attractive dividend of ₹25 to ₹30 instead. All possibilities cannot be ruled out.

1 Like

Rohit Balakrishnan has updated us on buyback price of ₹550 & Record date is April 12, 2019. Now buyback entitlement ratio is 5 % of your holding on record date & for small investors holding less than 400 shares, perhaps it might be 15 %. Company will definitely rush thru the process, as after Q4 results, share prices may be in the vicinity of ₹700 to ₹800 levels. Again if prices go above ₹550, buyback will fail & company will be forced to give ₹24 per share dividend.

For the promoters, who are not participating in the buyback, shows their confidence in the business, also their stake should go up, equity capital will be reduced by 5 % & EPS will go up on a proportionate basis.

Expect higher dividends in the range of ₹30 to ₹50 per share over the next few years, Company’s business is certain to pick up under the global umbrella of Expleo solutions brand. But for small investors, Dividends are best, coz they may lose 15 % of their holding & may not be able to buy from the market at prices below ₹550. So buyback is a losing proposition for small investors.

Any particular you are confident that quarterly results will be so good that company will rush through the buy-back? They can make market purchase too -no?

Usually Q3 is subdued due to ramp down & seasonal holidays & Q4 is period of bumper profits. So if results are good, share prices should be in the vicinity of ₹ 700 to ₹750 levels & buyback will fail as none will tender for ₹550. Precise reason why the company will rush through the process, before Q4 results are out

Further forex, dollar & pound status will also have a bearing, since 80 % of revenues are in forex dollars & pounds.

Buyback is from the shareholders thru tender offer at ₹550. So Purchase from open market is not possible

Again foreign promoter ASsystem France & Ardian France, a major PE investor, has created a global umbrella brand of Expleo solutions, for software testing, QA, managed services & Management consultancy, security surveillance, Data analytics, across the entire spectrum of software testing in automobiles, aerospace, pharma, Railways, & all industrial segments, worldwide, though Sqs Bfsi will continue its exclusive focus on Bfsi sector.

Though iam invested in substantial quantity in this MNC small cap stock for the long haul, volatility in quarterly profits & share prices is inherent.

You can also have a perusal, of analysis by Rohit Balakrishnan, who, regularly attends Sqs Bfsi investor conference calls & attempts to obtain info. Rohit has also given a write up, on Sqs Bfsi on his website vrudhi capital, as well as magnanimously shares & updates info on this board.

The only concern, is growth has been anemic, over the past few years & also volatility in quarterly profits due to plethora of factors like ramp downs, stress in IT sector, brexit issues & resultant pound depreciation has already taken its toll.

Future looks bright & if Expleo branding & aggressive growth, which Adrian is navigating takes place, it should be a potential 10 bagger in coming 10 years or even earlier. As of now, 25 to 30 % of software development costs are reserved for software testing & QA.

2 Likes

Q4 results on Monday, May 6, 2019. Analyst conference call, may follow, the next day. Over to Dear Rohit Balakrishnan, to extract information from the concall. Thank you & Regards Rohit & do keep us updated.

Hi Rohit Balakrishnan, Q4 results of Sqs Bfsi ( Expleo solutions) tomorrow. My estimate is EPS in the vicinity of ₹15 on a turnover of 85 crore, but I’m inclined to suggest that EPS will be in the vicinity of ₹5, by engineering sales, profits, other income, scrip sales, receivables to spill over to next quarter. Perhaps this is essential gimmick for the success of the buyback at ₹550. This will facilitate investors to replenish their shares tendered in the buyback, from the bourses at around ₹430 to 450 levels, keeping shareholders, promoters & operators happy.

Further looks like no final & interim dividend this year in lieu of buyback. If next year, if no dividend in lieu of buyback policy is followed, with another buyback, perhaps at ₹650 levels, without promoters participation, promoter holding will easily increase to 60 %, leaving another 15 % short fall of 75 %.

Again Q1 results may show bumper harvest of profits. These are my thoughts from experience of observing Sqs Bfsi, daily. So Rohit Balakrishnan, should be able to give us a better perspective & also be able to get answers, from analyst conference call by shrewd questioning. Thank you & Regards Rohit.