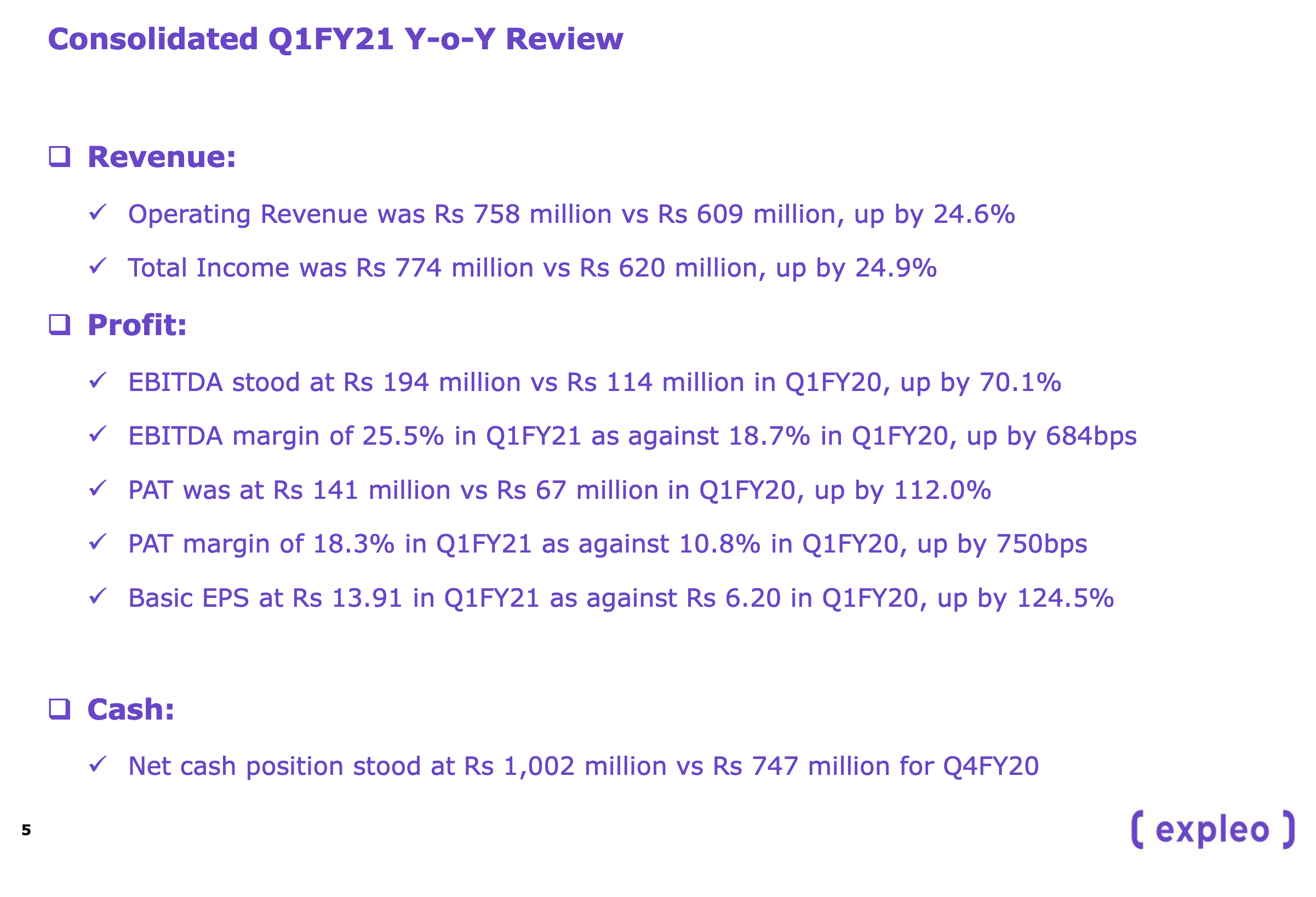

Hi Rohit Balakrishnan, Q4 Consolidated EPS is ₹ 8.71 & Consolidated audited EPS for year ended March 2019 is ₹ 33.80, against ₹29.90 for yr end March 2018. I was expecting EPS of ₹14, though I suspect that some of the receivables, other income will spill over to next quarter, to save the buyback process, without promoters participation.

Tomorrow 4.30 pm, investors / analysts conference call. So Rohit get ready.

Now my view is if the brand umbrella of Expleo solutions as a brand entity for complete independent software testing solutions, across the entire spectrum of industries where software testing, validation, Quality assurance, security surveillance, management consultancy, Data analytics etc are leveraged by Adrian, sky seems the limit for growth especially with digitalization & Robotic process automation.

Its only one name like only vimal. The unlisted entity is Expleo solutions ( erstwhile Sqs Germany & ASsystem technologies SA) & the listed entity is Sqs Bfsi in the avatar of Expleo solutions.

Now while the unlisted entity will cater to both Bfsi & non Bfsi sectors, the listed entity ( Sqs Bfsi) will focus exclusively on Bfsi sector.

So, my thoughts is, if Ardian steps up the turbo, Sqs Bfsi, can easily exceed EPS of ₹50, any time in coming 2 years.

Now Rohit, will the parent give another ₹ 30 per share dividend or go for another buyback, without promoters participation to raise stake to 60 % next year?

Most unfortunately I was held up in a meeting, at the critical hour, so I could not attend tele conference / investors concall.

I have written to the secretary, to either email me the transcript or upload it on the website, to which he has promptly replied, that he will do it, once transcript is finalized.

In the meanwhile, I would request Rohit Balakrishnan, who regularly attends Sqs Bfsi con call to give us the important takeaways & info.

Growth has been subdued for last 3 years, was the query raised by Rohit Balakrishnan

Management says Europe & UK growing at 7 % along with inability to mine growth in USA ( the world’s largest market) has been responsible for subdued growth.

Further, management has indicated that for next 3 years, buybacks in lieu of dividends will continue.

of ₹100 crore cash ₹25 cr has been expended for buyback & rest ₹75 cr will be used for pursuing growth.

As of now, major growth in Expleo is expected only after 2 to 3 years.

My own view is Expleo solutions is likely to attain annual Consolidated turnover of ₹500 crore in next 3 years & ₹1000 crore in 10 years from now.

would request, Rohit Balakrishnan, to kindly give us his valuable views.

Is there any client concentration risk in the stock ? Like the kind of risk R S Software had, all its revenue were coming from VISA and then VISA pulled out.

Top 10 Contribute ~60-70%. This is similar to most mid/small cap IT services firm. They are heavily dependent on Europe which will certainly impact them.

They are dependent on Europe so they will be impacted but their survival should be ok. They are debt free with cash of around 90 Crores. Market cap today is 130 Crores. Is the business 40 Crores? They generated 32-33 Crores of Profit last year and maybe will generate 28-29 Crores this year.

@rohitbalakrish_ Yes rohit they have cash of around 100 crore and now the market cap is about 135 crore, thats really surprising…

After this qtr result we can even expect a buyback or a dividend…management was even confident for this qtr to be better then the previous one…only one red flag about contingent liabilities on service tax & income tax matter which they didnt convincingly replied me during concall.

Lets see how they perform going forward

The company has recently come put with good results both on revenue and pat front. Looks interesting, couldn’t attend the concall. Anyone who attended would be great if they could share some highlights

Company is on track in implementing strategy to return to double digit growth and Covid-19 disruption hasn’t impacted much. Management is confident that execution of current strategy will take it to double digit growth after couple of quarters to overcome Covid-19 situation.

Increased receivables - Its due to closures and lock down globally. Companies were not having systems in place to pay. That was scenario till March end and now situations are coming to normal. Recovered 30Cr in month of APril. Cash balance is 89 Cr. at present after paying for working capital needs of two months.

Digital - Company is working on automation and digital and 14% revenue can be attributed to digital. There are no accounting practices in place for now to measure it and going forward they will bifurcate same.

Dividends - company conserving cash due to current crisis situation and once situation comes to normal it can declare dividend.

WFH (100% as of now) is going smooth and operations are very much on track. After situation becomes normal - employees will return to offices with and WFH is not seen as permanent though it will continue at some increased level compared to before Covid scenario.

BFSI - Company still focus on BFSI and outside BFSI there can be some digital opportunities. But BFSI is bread and butter for company and there is scope to grow in this domain

Testing - Requirement gathering and testing are the main focus areas of company and will remain so. Consulting is another operational area for the company. Testing itself forms 12-15% of IT budget of companies and has lot of space to grow. Company will not become like Bn dollor company in testing space, but there is space to grow.

Revenue from parent - Group CEO and COO are on board of Expleo SOlutions and there will be traction in parent revenue once situations become normal in Europe and other regions.

Customers with more than Mn revenue - there was some scale down at customer ends and customers shifted from more than Mn to less than Mn category. Looking forward to increase this number soon with IT spending coming back to normal.

Expansion in US - It needs capital and focus and currently comapny is focusing on existing presence. There is good traction in Asia and Gulf regions. US expansions looks like on back seat as of now.

Buyback - Definitely price is quite attractive now. Due to cash conservation strategy company hasn’t taken any decision yet. Next board meeting (Jul-Aug,20) this can be brought on agenda and thought of.

No plans to cut headcount, but hiring rate will be slower. There is reduction in employee turnover which is working out well for company. Company expects reduced hiring costs by retaining more of its employees.

Pls add for any missing points.

Disclosure: Invested and looking out to average out with current lower price.

Management is honest, in the last concall MD said that next 2 quarters profits may decline by 10 percent. He also said that the company is likely recoup the decline in subsequent quarter & also attain double digit growth ahead.

Attended by - Mr. Balaji Vishwanathan - CEO, Mr. Desikan Narayanan - CFO

Performance - CEO comments -

Business activity is resuming to normal and see demand coming back to normal or more than pre-Covid level in next 2 to 3 quarter

Digital investment is paying off and revenue share from digital services grown to 20-21% as compared to earlier 10-12%

US and UK geos are stabilizing even though no growth and MEA and APAC - things are much better

seeing traction in offshoring from Middle East region for the first time and that trend is expected to continue

Won 4 new customers with winning back 1 lost customer earlier

some revenue impact might be there (5 to 7%) bcs of some customers face budget cuts and some of them calling off projects because of Covid disruption. There will not be much impact on margins - its related to old contracts and not for new business.

No salary cut for employees or job cuts/layoffs during this entire Covid 5 months. Billability level maintained at 98% from 18th March

cost measures taken have shown improvements in margins and expect trend to continue

CFO -

Margins improvement bcs of increased offshoring and reduced travel

Direct regions (APAC region) revenue has been good impact on revenue and margins along with offshoring

New tax regime of 22% tax also helped to improve PAT margin and EPS

QnA -

Revenue impact guidance - its bcs of ramp down in contracts. If impact would not have not there QoQ growth could have been 5.5% instead of mere 0.4%

higher DSO - bcs of payments delay. Jul company collected 40 Cr. Now customers are paying and things will be coming to normal

Dividends/buyback - managing group level changes for now. Group CEO will settle down before taking a call.

Digital testing (RPA/DevOps) is new trend and company is focusing on digital capacbility

US Market - upfront investments needed to grow. We were tactical rather than strategic to grow. So currently focusing on existing customers but not strategic investment decision as of now

Middle East more offshoring - cautiously observing and trend will not change in medium term at least.

Growth - will come from UK and Europe in short and medium term. Looking to focus on group. To double revenue from 40 to 80 Mn (or 100 Mn) - 40 to 65 will come from Europe and Group and remaining 10-15 Mn from APAC. Company will move to 80 to 100 Mn revenue over the period of 3 to 4 years.

50% workforce right skilling - decline in HC is bcs of downsizing in contracts and freshers hired through third party agency contract has been reduced. But Q2 HC number is increased. Due to increase in Automation - HC will not increase much. Even if revenue remains same - revenue per HC will increase. 50% up skillikng target is on track and Covid scenario has helped in this regard and we think target will be surpassed by year end

Group business - offshoring business coming from English speaking countries. 30 to 70% work is offshored. Company focus to increase offshoring from 30% to 50% and so on in existing accounts.

Export incentive reduction (mention in AR) - There was no govt notification for 19-20 for export incentive and hence its not accounted. If government notification comes it will be applied in accounts. No clue on government will continue export incentive or not.

Europe market focus through group - it will improve revenue as well as margins.

US Market - current revenue @5%. Currently not focusing much on US market.

Rajesh krishnamurthy (Expat Infy) is joining as group CEO based out of France and will be on board of Expleo

Group Support - BFSI business at group level is 125Mn aprox out of which Expleo do 1 Cr currently. So there is huge opportunity to grow. Also need to sell offshoring which needs different skills than group sales has. And another one is R&D enagegment where group R&D facilities in Europe and company facilities in Chennai can collaborate more.

My Comments -

Next 2 to 3 years look good runway for the company looking at management comments. Need to observe results and activities closely.

No focus on US market may auger well for company in my opinion bcs of US policy uncertainties regard to outsourcing/offshoring

Group revenue business focus should give both topline and margin growth

Automation focus/upskilling/increasing revenue per HC looks good along with more than doubling revenue target in 3 years time. Management has history of under committing and over achieving. Lets hope it will surpass the guidance.

Testing as a overall to specialized third party company like Expleo will see increasing trend bcs of digital/automation/security requirements

increased offshoring trend from ME and other regions is interesting trend to watch coupled with remote working capabilities will help improve margins

Concerns -

Margins may come a little bit down once Covid scenario recedes and things come back to normal. Travel and other expenses will go up

Any challenges in Banking and related industry will be a setback on company revenue

Deputy chairman - K Kumar letter to shareholders -

21% business coming from Expleo group against 19% of last year.

UK and Europe was slow, US revenue remains weak despite great potential for rise there, ASia pacific does well where company revenue comes directly from

Adopting new technologies in faster way especially around mobile, RPA, iOT, API and PLM

50% of the employees to be techno functional skills by end of 2020 to adopt to the digitization needs of BFSI

Financial Highlights -

working capital is 123 Cr for FY 20 against EBIDTA of 61 Cr.

Revenue split - 62% Europe, 32% Asia Pacific and 3% from US

offshore revenue 47% as compared to 42% last year

5% revenue from new client additions

banking vertical revenue de-growth of 12% and now stands at 35%

Employee HC of 1062 as comparedd to 962 of last year

Management Discussion and review -

Focus areas - Digital, IOT, Data management, Automation and DevOps

Asia focus bringing results in terms of deal size and revenues (27.5% to 35.4%). Even though major Europe revenue got affected (68% to down 62%), Asia focus was able to coup up that. US remains challenging geography

UK and Europe remains focus area along with building capabilities for Asian market. US needs significant investment and long waiting period for results

last few years saw drop in large managed testing services contracts. This is due to Agile and DevOps adoption which is demanding continuous testing and up-skilling of employees. New-gen testing sees CAGR potential of 12.5% over the next few years

techno functional workforce (50% target) and offshoring approach for cost effective solutions will help customers of Expleo

Risks (My comments) -

Automation and AI/ML hampering testing business for testing firms? How Expleo is adopting to provide automation solutions with may be reduced revenues but maintained/improved margins? With initiatives in RPA and automation Expleo looks like turning this threat into opportunity. Need to see impacts on numbers in coming years.

Slowing UK/Europe revenue. Group revenue is one positive side and other one is increasing APAC revenue. But will this have impact on margins? Need to watch closely

Dear friends, the main concern is that revenues & growth has stagnated from 2016 to 2020 , due to a plethora of factors.

Management is now, talking about double digit growth,ably supported by the parent, Asssystem technologies, France & It’s PE investor & Financial power house, Adrian having an investment of 100 billion USD , worldwide.

The management intends to double revenues in 3 years to 100 million dollars , with an estimated net profit of ₹120 Cr , giving an EPS of ₹120 , assuming all goes favourably well with this company.

Taking a PE of 25 ,( which was commanded by this scrip in 2016 ) ,I will not be surprised to see a price of ₹3000 per share on this small cap, MNC stock. Would request, all boarders , especially, Rohit Balakrishnan & others to share their valuable views.

I also find that Rajasthan global securities is holding 5 percent, another 4 percent by Kalparaj Dharmsi family , one lakh shares held by Nihar Nilekani, son of Infosys executive , Nandan Nilekani , another 4 percent is held by HNI s

If u see latest shareholding dharmashi family has completely exited or reduced the stake less then 1% in the company…

But yes the future looks quiet promising, only worry is they skipped dividend in 19-20 and neither they did a buy back…with the backing of ardian we can see much improvement in topline as well as bottomline in coming qtrs & yrs.