1 Like

2 Likes

This company is on the front foot expanding business, buying strategic businesses, and collaborating with other players for innovation. If synergies and innovation play out well, it can show out-performance over longer term compared to other players that are having uncertain future in the IT industry, which itself is undergoing disruptive changes.

As a novice investor, Prima facie looks like there’s material upside here on the counter from current valuation, inviting useful insights or feedback from Senior VP and other fellow members.

Disclosure – Not invested yet

1 Like

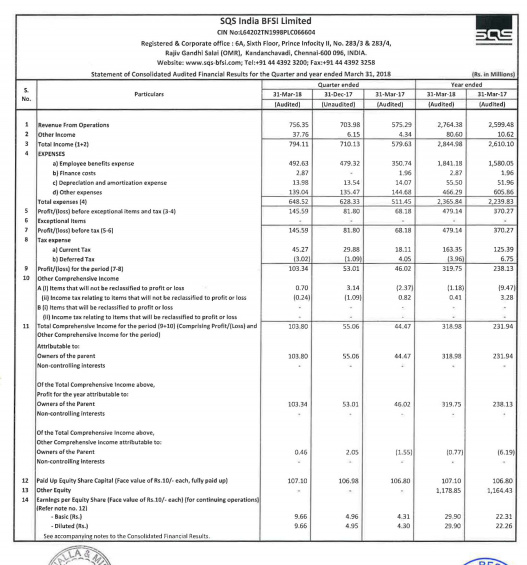

Excellent nos. - Strong revenues and profits growth… plus 20 rs dividend…4+% div yield…

https://www.bseindia.com/xml-data/corpfiling/AttachLive/ef67cfea-c6f1-42c4-8946-38b74b1e2d44.pdf

4 Likes

Summary of Q4 concall

- 10.7 million $ was the revenue for q4

- 10% growth in revenue for the year

- Revenue from Europe significantly

- Revenue from cards and payments and insurance increased. Revenues from bank decreased due to projects coming to closure

- Group clients from 24 to 26. Many have become annuity clients

- US didn’t grow as per expectations

- AT would help to grow and scale up

- Group revenue is 19%

- Head count increased by 50

- Attrition is normal.

- Quarter was better than expected

- Assytems is not focused in BFSI as of now and to have the exposure in BFSI the acquisition was done. PE funds which supported the deal are having connections in BFSI and would be good for SQS.

- Cross selling would be difficult as most of the customers of AT are in automobile or aerospace

- Customers don’t give a 5 year plan.

- Trend, challenges and opportunities are there. SQS offerings are also changing with the changes

- During the year the govt notifies export benefit income. Hence for this year it is yet to be announced.

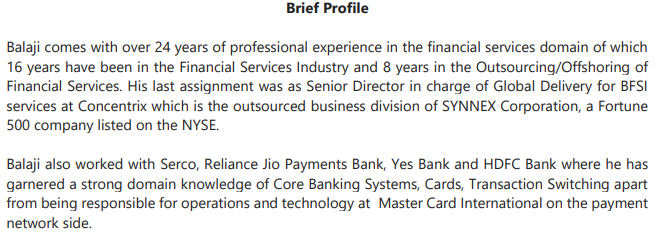

- Have identified a new CEO but cant be disclosed as of now

- Will take a bit more time to scale up US customers. Continue to look at how to get more revenue from US.

- Revenues are slightly lumpy

- Employee utilisation is 72% in current quarter

- Couple of customers paid in April instead of March due to change in their internal processes

- Current headcount is 1015

- 6-7% is the yield on current cash. Cash is kept as FD.

- Rajasthan global securities has 4% stake and suggested the panel to do buy back over dividend.

- Board is looking at using the cash through dividends, working capital and Capital Investment

- Will consider buy back as an option going forward.

- RGS grilled management on offer price.

Regards

Sri Krishna Bhutra

Discl: Invested

9 Likes

Link to the Conf. call ?

Hi Amit,

You can get it at researchbytes.com

Regards

Krishna

AGM is on 26 JUN , Should we expect the DIVIDENDS by then ?

With progress in automation , robotic process automation etc, i was expecting that testing companies would be the first one’s to be impacted negatively. But numbers are showing otherwise. SQS seems to be holding steady so far. Anybody knows how is this happening while everybody is screaming so much about automation in TV channels.

Any1 tracking sqs now?? If yes Pls update

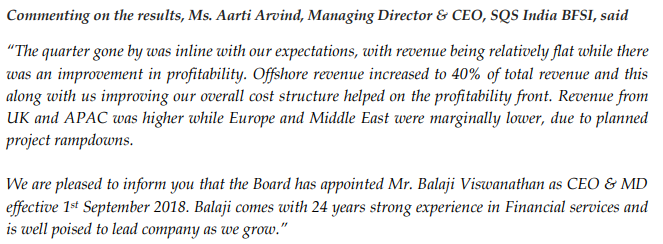

SQS has declared Q1 FY19 results.

Q1 presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f7471a15-6710-4da7-9bf0-97de899f15b5.pdf

On the revenue level results look OK as it would take some more time for revenues from US to flow in. Profits are down QoQ due to no forex gains.

The employee cost has come down due to decrease in number of employees.

Need to know from the concall why the employee strength has come down.

Below is outgoing MD’s comment on Q1 results

The new recruited MD has impressive credentials

This may help the company in future.

Company has nearly 90 Crores of cash reserves.

8 customers have been added and 5 customers have left.

Regards

Krishna

Discl - invested

2 Likes

Q1 FY19 Concall Highlights

- 731 million rupees revenue. Scrip sales of 7.2 million. Planned rampdown by European customer. This is a cards and payments regular customer and they expect the revenue to again increase from the customer.

- Improved profitability is due to improved offshore revenues increased to 40% from 38.5% and also due improved operational efficiency

- No significant changes regionwise

- Group wise revenues is 19% and rest from direct customers

- Slightly higher attrition than previous quarter but this is more of seasonal nature as the quarter generally has higher attrition

- Compensation exercise to be done in July and attrition would decrease then

QnA

-

What is the new management planning to do about SQS India BFSI

A. It is for AS Systems to diversify into BFSI and also in terms of offshore. AS Systems looks upto SQS India as a thought leader. Not many changes are happening at India entity level. Business would continue as it is. Would get more access in Europe and would leverage the parent’s network.

De-listing already happened for SQS AG. Entity getting merged with SQS AG is not listed. -

What would be the employee strength going forward?

A. Not a linear equation. It depends more on the kind of projects. Careful on adding a right mix of people. Difficult to put a number to it would depend on business mix. -

AS Systems vision for SQS BFSI?

A. Won’t be providing direct BFSI clients. Would be able to leverage clients treasury requirements or financial transactions. Also the PE firm can provide some leverage. -

How do you see cards and payments segment in the coming years?

A. The opportunities are there and even there are current clients. Wont attach much weightage to QoQ but growth would be there. -

Are there any plans to diversify to others areas other than QA?

A. Not as of now. What we were doing in QA 3-4 years back and doing now is very different. We now help in process automation. Not pure development and don’t have plans to get into it.

A. customers are breaking down things a lot. Customers don’t have 5 year plans now. They break down things into quarter on quarter. One should try to be preferred vendor of choice. To be the preferred vendor of choice is what is working more for SQS. -

What if developmental partners of the clients offer QA service?

A. This competition landscape has always been there and hasn’t changed now. The maker - checker concept is here to stay. Larger BFSI clients want to have someone else to look out at developmental activities of another partner. -

Group revenue?

A. from 18.2% to 18.7% QoQ. Hasn’t changed much -

Market size of QA?

A. QA is very niche area. Some offer QA part bundled with developmental activities and others are purely into QA also. Market, opportunities and potential is there. -

Software deployment on different models

A. Core is same and hence deployment models such as cloud, on premises doesn’t make much difference. Banks for security reasons don;t do SaaS

No further buyback of shares or buying of additional shares.

Cash on books is pre-dividend

Some raised concerned for resignation of CFO. But he tried allay fear of the investors.

No discussion on US revenues.

Regards

Krishna

Discl - Invested

3 Likes

Sri Krishna bhutra as given exhaustive coverage on Sqs Bfsi. Latest Q2 results give EPS of ₹ 12 plus on Consolidated basis & full year can be in the vicinity of ₹50 levels. Rupee depreciation, Cost control, more of offshore vs onsite revenue have been the reason. With new promoters, ASsystem & Ardian & their financial might, with senior Sqs personnel running the business, this share should easily cross its life time high of of ₹1291

In investors conference call post Q2 results, the management has well laid strategies to mine significant growth, worldwide especially US market in coming years. No decision on interim dividend has been taken, pending further investment in US, along with delisted Sqs parent. Only concern has been revenue growth has been flat, for past several years, despite brexit & pound depreciation & forex losses in after math of brexit, company has reported EPS of ₹24 in 2016 - 17, shows the resilience of this firm. With new & worthy parent, with financial might & clear agenda to mine revenue from worldwide especially US, I anticipate this share to be a 5 bagger in the coming 5 years. Also eminent investors include Kalpraj Dharmsi of Dharmsi securities holding nearly 4 lakh shares in his & family members names, only son of Infosys Nandan Nilekani holding nearly a lakh shares, Rajasthan global securities holding 2.5 %. Further company directors hold nearly a lakh shares of which a lot of 68,000 shares is held by Rajiv kuchal, now executive director of Sqs Bfsi. Shri Rajiv kucchal is also an angel investor & former head of Infosys Bpo. Would kindly request Shri Krishna bhutra to share further information. Discl holding substantial quantity for the long haul.

1 Like

The Q2 results were good, aided by foreign exchange gains. However what was also good to see was operating margins continuing to trend upwards. Growth, however is still anemic. Should that improve, we can expect the market to appreciate the metrics of the company.

I had written a blog on my website recently

Essentially the thesis on margins improving is playing out, hopefully it should continue. However growth is yet to pick up. At the valuations it is currently trading it is one of the cheapest listed MNCs in India.

Disclosure: SEBI Registered Investment Advisor.- VRDDHI Capital Investment Advisor - INA100008832

Expect me and my clients to be invested in SQS BFSI and thus my views would be biased. Please do not treat this as an investment advise. Please consult your investment adviser before buying/selling

@Administrator If you suggest, I can put that blog here. Kindly advise. Thanks

4 Likes

In the latest concall the new MD comes across as a guy who knows his business. He has vast experience in the BFSI space and that should help SQS in pursuing a path of growth.

He has mentioned about formulating plans for the company and probably would divulge in the next quarterly concall. As mentioned by Rohit q2 fy 19 results are looking good bcos of currency benefits. Some amount of cost cutting also has been going on.

The dividend policy till now has been very liberal but according to management it would be made clear going forward. As demanded by Lalit Dua on the concall, I think buyback remains the best option of utilising the cash on books.

8 Likes

Rohit Balakrishnan has done a splendid job. I hear that total turnover of Sqs Bfsi parent, ASsystem group is around 1lakh crore. Software testing market is projected to grow to 550 billion USD in coming 5 years. Of this, Bfsi sector accounts for 25 percent & half of the testing market is in USA. What iam really concerned is growth in revenues has been flat or Anaemic for Sqs Bfsi. Further exclusive divisions focused on testing verticals of SI like Infosys are able to mine 1 billion US dollars revenue per year. Iam certain that the new parent Is hungry & passionate about growth & next 5 years, show potential for generating massive growth by Sqs Bfsi. Would kindly request, Rohit & sri Krishna bhutra, to update us on Sqs Bfsi, on future prospects & potential. Thanks a billion to you, Rohit & sri Krishna bhutra. Warm Regards.

Hi sri Krishna, I’m in value pickr forum just because of you, chasing info on Sqs Bfsi, From all sources, available led me to this forum. Now again, Rohit Balakrishnan has come in, if my memory is right, I have heard him, asking questions at Sqs Bfsi investors concall, on several occasions. I have also gone to his new website, vrddhi capital, & under the blog, gone through his thesis on Sqs Bfsi. Wonderful info. Appreciate & Applaud, Rohit for his integrity, patience & truthfulness. He has bought Sqs Bfsi from ₹550 levels & then averaging till ₹380 levels. ₹366 levels was for a few seconds & life time high was at ₹1290 levels in 2016. It has the potential to cross its life time high, probably in coming 18 months.

1 Like

Thank you, Hitesh, for your valuable views. It’s immaterial, if Sqs pays out dividend or buyback, as long as shareholders are rewarded. Having a small equity capital of 10 crore, with tremendous potential of growth ahead, Dividend always makes shareholders happy. The culprit is DDT & 10 % tax + cess on dividends exceeding 10 lakhs per year. Hope Government assimilate that dividend or returning shareholders funds back to them, after paying all legal taxes ( our corporate taxes are high) is not a sin to warrant DDT & dividend tax at 10 %, for dividends exceeding ₹10 lakhs per year.

Hi Rohit & sri Krishna, I have given a summary of Small cap niche MNC stock, Denora India under stock opportunities, special situations. I have more conviction in Sqs Bfsi, than Denora India & it is reflected in my holding. Would request both of you, or Hiten to give valuable perspectives. The past returns on all parameters have been poor & reasons for the same has been explained. However since the parent has taken full control, it merits a study, as it is a totally unresearched stock by analysts & investors.