As investors it pays to be able to see long runway( structural themes) before majority of folks do, coupled with patience and conviction, compounding may happen and delivers holy grail of outcome. Of course numbers + narrative and rerating has to happen underneath to make it happen.

@RajeevJ has a golden touch in identifying winners and @Vivek_6954 was kind enough to point me in this direction, bonus was to see @Worldlywiseinvestors on board. What more can one ask for to dig deeper

Bear with me for a top down view in this bottom up stock specific thread -

Energy landscape evolution

We all know that world is moving in green energy direction, given humanity survival depends on it - renewables is THE theme for multi decade. Fossil fuel need to be done away to make it happen.

lot of buzz around EV and batteries - equal challanges about storage infra( how scalable battery infra can be when China controls major tech and rare earth material)

How about Ethanol, CNG as alternative for a sustainable middle ground that India has better control on - we all know current policy push supporting these. But they still generate little CO2 though significantly lower(1/6th to 1/10th) than current Fossil fuels, but hey we have these in our backyard. Hence govt push on CNG and ethanol.

What stands out is energy source and energy consumption( both should be CO2 free)

Source of energy - solar and wind is our long term and scalable solution with ample repleshinable resources. This is sorted for India and globally, agreed and is a world mission ( Renewable theme)

Hydrogen when generated from above is fully green and again scalable ( all we need is electrolysis, water &ability to store/transport , and yes making it commercial viable is still in works ) - do read about national Hydrogen mission, Reliance 1:1:1 mission( 1 Lt Hydrogen in 1$ in 1 decade), 10% compulsory Hydrogen usage in Industries by 2024 and so on…

Believe we all get a point on possibilities, but action currently lies in EV space, look at multibeggars after all, here is my submission

We can generate all the energy we need using natural sources( eventually), where are we going to store it for night/time elapsed usage?

Is battery based infra scalable ? Consider dependency on China, rare earth material and so on - India can’t be Atmanirbhar ever right?

How about Hydrogen ( water + electrolysis) storage which is generated by green source, in a tank as alternative solution - well don’t need to agree but give it a thought keeping India context of Atmanirbhar. BTW Hydrogen based mobility, industrial use are all live and not too far behind from Battery landscape.

Where does Kanto comes in picture

Near to med term- 25% CNG from current single digit in country in near future - that’s a 2-3X opportunity on OEM+CNG station+ Replacement market- don’t trust me but see what’s Maruti bet on CNG, see Kento Capex and commentary on CNG, see pace of recent CNG station approved and India coverage.

Longer term- When Hydrogen solution scales - who will be providing cylinders? Far fetched but feel free to assign probability for this humongous Optionality.

Valuation

Capacities to near double from 7L to 13L including brownfield (4) and greenfield(2).

Q2 is 420 cr revenue, 25% opm at 112 cr, 2800 cr mkt cap I.e annualized 1.6X sales, 6X EBDITA

FY 23 will be with brownfield capacities online(7 to 11)- at similar realization can expect annualized 2600 cr revenue 600 cr + EBDITA( can be higher with op leverage), with likely rerating( high growth and tailwinds)at 10X EBDITA we are looking at 6000 cr mkt cap possibilities - ofcourse subject to FY24 + growth momentum being visible.

Return ratios and EBDITA to cashflow has been decent in recent past.

Risks

Mgmt ability to maintain domestic mkt share in CNG( Believe 50%), beauty here is that space is being seen as temp vs structural hence not attractive for new players ( similar story played out in Borosilrenwable in solar glass)

Margins - can continue to be high unless supply exceeds demand, all iz well as it ties back to only current players expanding capacities - for now atleast. Commentary is strong.

Optionality driven by Hydrogen commercial viability, so is battery based large scale storage.

Mgmt quality - unsure but this qualifies for strong tailwinds sector and an average mgmt should suffice.

Invested with small allocation, studying, plan to ramp up as execution builds

They keep pointing out that they have 50% market share. Yet one simple Google check for Rama Cylinders credit rating shows their capcity at more than 5L cylinders. With capacity expansion in place.

Why were they blacklisted? Simple reason seems to be (hope not). Were they profiteering during the time of covid. As capacities are fungible, margin remained where it was in Q1 as in Q2. Showing the production must have happened for Auto.

Third question, do they have any plans to shutdown the US business. Given it’s been loss making for almost 8 years in last 10-11 years of history.

Fourth Q, what is the linkage with the elevated steel prices? Do they end up getting affected when the steel prices reduce/realizations go down.

From my understanding, per CNG pump set up, Rs. 32lakh of Cylinder cascades are used. Multiplying this simply with the incremental stations shall give us some idea of the opportunity landscape.

Final key question that perplexes me. Why announce a Greenfield before a brownfield?

Disclosure:- Invested and searching for answers. Next leg of rerating will only happen when they actually repay the debt completely. No excuses are left given the cash flow generation (they have reduced the coupon though for promoter debt to 9%)&finally when the expanded capacities kick in.

Markets are skeptical and rightly so. This is why the multiple is dirt cheap. Let’s see how the story evolves

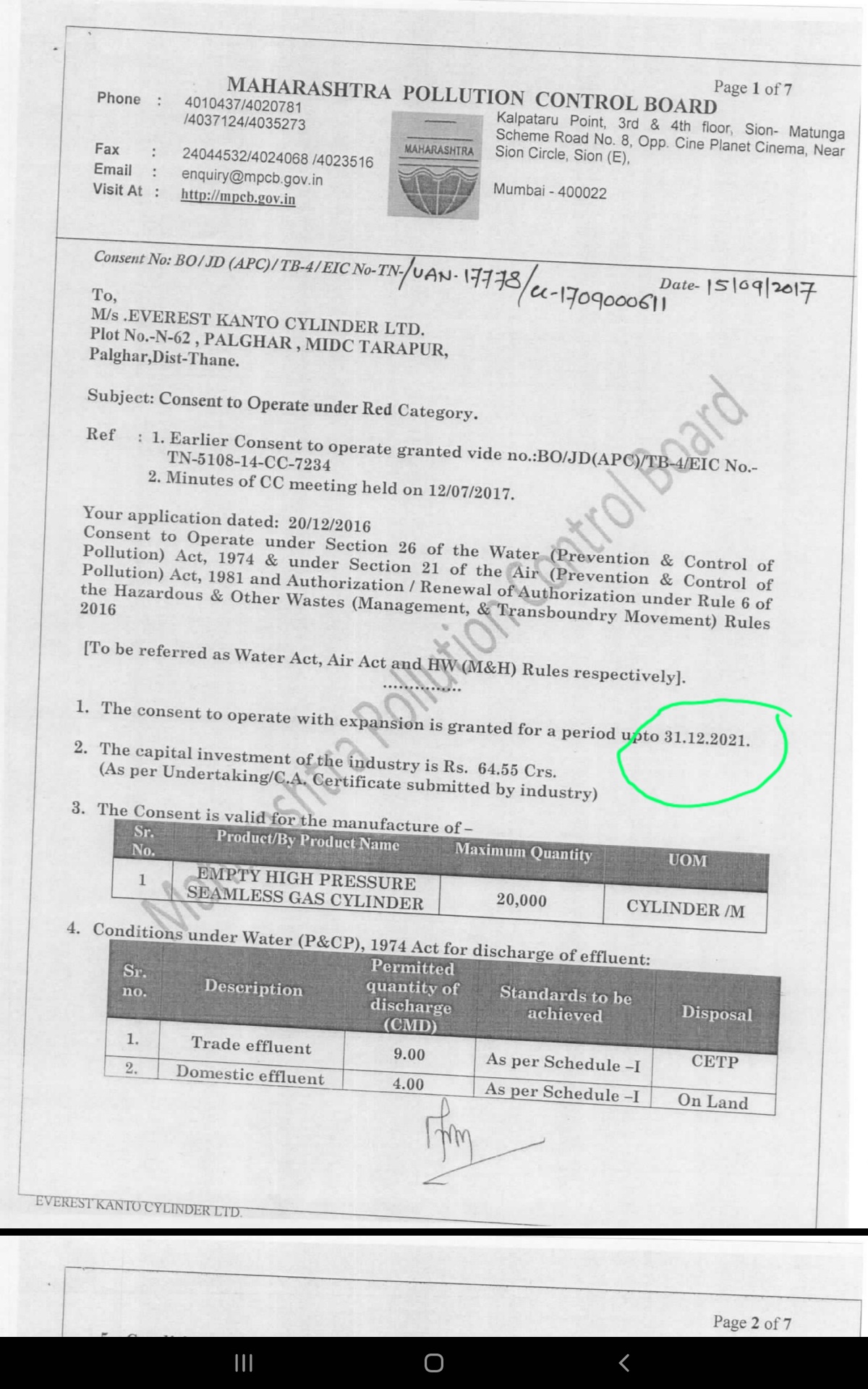

This one on brownfield vs greenfield was indeed intriguing - a quick search - one logical explanation emerges is - MH current production facilities environment clearance seems to be till 31 Dec 21. Couldnt find Guj plant EC details.

Given capacity expansion were announced in H1 21, and they got blacklisted meanwhile. To de risk new investments from current issues - a logical step would be to setup a new plant( assuming scope of blacklisted are existing plants - legal experts can comment). - it’s pure hypothesis and may be wrong. Brownfield was announced much later in year, possibly after they were sure around improvements and backlash diminishing.

Now this is something not easy to explain hence both communication and intent remains unclear, and doubt it is black and white.

Both sides have their stand - Kanto seem to have conveyed clearly that can supply 14000 cylinders out of 44K demand and hence requested tender penal conditions modifications. We all can interpret as we see fit, atleast found them communicating to govt per article. Also prior to May Kanto did supply 1L to govt+others per article.

We as outsiders will never know. And money( markets) have short memory.

A quick check in AR if they are fulfilling CSR obligations, seems they are,

I really like the explanation on cylinders and capacity and marketshare. But what makes me pause, how bad are you that you get blacklisted? That too by the Gov. where graft is normalised? It’s either very brazen or they hit a honest officer?

Maurti is not one of their customers since they make the cylinders in house according to the representative from EKC

Retrofitting market is much larger in PV for CNG since there are only 8 OEM models with pre installed CNG kits

As per my channel check, only Daughter station(does’t have pipeline connection) is required set up stationary cascade(generally bunch of 40 or 60 cylinders of 75 water liters each), this can be permanently installed at one corner of CNG station and can be refilled. Life time of this cylinder is approx. 10-15 years, hence future recurring demand of cylinders post its installation, is not burgeoning.

@Worldlywiseinvestors - In your post, you have mentioned 30 lakh gaskets, Can you please ponder more thought here (I am sure I am missing something here) to estimate the potential demands for next 2-3 years.

Have mentioned Rs32 lakh of cascades per station. Did the correction^^

Per station the amount thag is to be spent on setting them up. Mentioned the Rupee unit there no.

Basically per cng station, 32lakh rupees of cylinders can be used. Multiplying that by the new stations to be set up can give us an idea. Coming from the IR team, got an idea from them ^. Please do verfiy independently

Bet on CNG is bet on CNG vs Diesel price arbitrage as key thesis, wider it is , better adoption and pace

Some numbers from above article and extrapolation For size of opportunity

H1 22 saw hyper growth- 1L CNG PV.( near 100% YoY), 1.2L CNG CV (60% YoY) , 3W at 60K ( 350% YoY) - approx 2.8L, for year FY 22 let’s say 6L

Tricky but let’s say this growth momentum continues for next 5 years at 30-40% average and moderates as base grows big. So ** FY23 onwards10Lac per year growing at 30%+ over next 5 years CNG new vehicles**

Station infra needs a good amount from 3000 to 10000 stations journey - let’s say 2000 stations every year and may need 50 cylinders per station - so next 5 years 1L/yr cylinders for station infra

Let’s add replacement market as well which could show decent growth as well - wouldn’t know size but say it’s 10%-15% of overall industry size( Kanto says 50% : 50% cng vs industrial break up - so 3.5 Lac CNG auto, since CNG they are at 50% mkt share in India so overall India numbers are 8-10Lac, so 10%-15% of that in aftermarket at 1lac) - growth at 20% CAGR so 1Lac per year for next 5 year aftermarket growing at 20%+

Demand vs Kanto supplies

Total auto side CNG 12 Lac/yr growing at 25%+ ( growth rate to moderate/increase and could be evolving considerations) - say FY 23 12 L, FY 24 15L, FY 25 18L

KANTO CAPACITIES- FY 22 7L+ minor debottlenecking, FY 23 11L incl brownfield, FY 24 13 Lac incl greenfield - note these capacities are 60:40 for CNG vs Industrial at Q2 22 level.

Even if Kanto were to maintain its mkt share of 50% in CNG, they should do well and at near double capacities in FY 24

Valuations

FY24 Base case for standalone biz - at current realization 2500 cr revenue and 500cr+ PAT - current mkt cap is 2900 cr. Even at 10 PE ( no rerating) they can be at 5000 cr mkg cap

We haven’t added Global rev of 500 cr and 40-50 Cr profit for buffer.

In optimist case scenario with rerating of 20+PE , magic unfolds and valuations can be 4 to 5X from here, and rerating can be higher if growth is sustainable and runway is longer - we shall know over next few quarters

All of above is for India/standalone and at best back of envelope, could be off

Key monitorable

CNG OEM auto growth rates

Management perception by mkt( walking the talk, transparency, better communication, institutional buyer interest…)

Debt free( next fin yr per mgmt guidance)

Price power wrt RM and Competetion supply , thus margins sustainable above 30%

Fungible capacities leverage per demand, thus high utilization- ideally near full

CNG vs Diesel price spread

Kanto mkt share - maintain/gain

Global subsidiary performance improvements ( margin)

There are 7 authorized manufacturers with Rama having a stated capacity of 6L cylinders/year (EKC current capacity is 7L/year). I guess Lizer is the next largest player with a plant also in Kandla. FJM and Jay Fe are small business units embedded in large group companies (JP Minda and JBM Group)

Maruti Suzuki is pitching hard for factory fitting over retro-fitting. I think factory fitted cars are a little costlier than retro-fitted ones (20-30k as per internet research) but I don’t think this difference is high enough to dissuade customers from getting convinced by Maruti’s pitch of better efficiency, safety and serviceability of factory fitted CNG cars.

Key questions from EKC point of view:

Where is Maruti sourcing the cylinders from? Are they being manufactured in-house? If yes, then this could be a potentially big risk for EKC’s auto OEM demand. Once CNG scale improves, what prevents EKC customers like Bajaj Auto and Eicher from doing the same?

If Maruti is not manufacturing them in-house, then who is supplying? EKC and Rama are both not supplying and they seem to be the largest manufacturers.

Auto OEM demand is a key lever for the projected growth for EKC, so any threat to this thesis can significantly alter future growth I guess. Would invite the experts in this thread to shed more light on this potential counter thesis.

According to IGL/MGL/Adani Total, the cost of setting up a station its around 2cr and there is a 12% cost of setting up the storage so roughly 24lacs

There is a minimum work commitment for 8097 stations as per the last round of GA auctions which means there is a rough market of 1950cr. in just setting up the CNG stations. OEM sales and retrofitting market is anybody’s guess but its safe to say that as the number of CNG stations goes up there will be a multiple fold increase in the number of CNG cars

Confidence Petroleum alone is going to open 100 CNG gas stations in Bangalore in next 2 years and some LPG stations too. I was hearing their investor call and they mentioned EKC name few time as number 1 player in CNG cylinders.

Check the history of promoters of Confidence Petro. I am sure you will have to rethink of your confidence on the company. They are all end of the bull market runners… even if they are doing genuine efforts this time I do not have confidence based on their past

As there is corp governace issue, where managements integrity is questionable, I am bullish as per technical not fundamentally, once a badass is always a badass, just a view,