Good set of nos released by Eris…

https://www.bseindia.com/xml-data/corpfiling/AttachLive/7bddd55e-c936-443f-9b95-4ce0cb921004.pdf

I was wondering why did the Revenue from operations decreased QoQ?

Is it due to seasonality? I tried to find out the reasons but did not manage so far. Would appreciate your views.

Nice coverage. A solid cutting edge company with a long runway for growth with v healthy return ratios, a passionate owner operator who has skin in the game and available at a reasonable price with a PEG <1. Ideal receipe for a multibagger.

Its trading at PE of 35 right now (price 800). even if we consider 30% growth in next 2-3 years , PEG comes around 1.2. what makes you think that its trading less than 1. What kind of growth rate you are assuming and rationale for it.

Good question… The damp results of latest quarter has put a question mark

on its future growth… Hope they pull it off again to growth…

With the integration and consolidation of the strides portfolio, I am expecting a 22-25% CAGR growth in FY '19 and FY 20 in the topline and at least 38-40% CAGR in the bottom-line with the i) outsourcing of the manufacturing of the strides portfolio to their Assam facility ii) expansion of the portfolio to other geographies (given 70% of the 180 cr. sales of the acquired portfolio comes from just 3 southern states) and iii) operating leverage.

Any idea why the latest q results were a bit disappointing…

It is in the concall transcript. They were disrupted by the integration with Strides. Moreover due to demonetization q3 '17 posted good numbers as people were stocking medicines. They said it should get back to normal levels in one or two quarters.

Interested to Invest … at research stage.

Attached is the initiation report from my broker Prabhudas Lilladher. Their research desk has good insights into the pharma industry. Do go through the 36 page long report.

Meantime the para on Valuation is quoted below

Eris being a relatively younger company with a shorter history is in the early stages

of growth. In comparison to the older peers, Eris benefits from its selective entry in

lifestyle drugs in the chronic therapeutic space. The choice of high growth

therapeutic drugs with better profitability has helped the company to achieve the

second fastest growth in the IPM. The marketing background of promoters led to

Eris focusing on the high-growth, high-margin chronic segment with differentiated

products. This has resulted in higher MR productivity and operating leverage. The

contributions of chronic drugs increased to 78% in FY17 from 52% in FY13. With

strong operating cash flow and miniscule capex requirement, the company’s

business continues to generate strong free-cash-flow (FCF) and bolsters its M&A

ambitions in focused therapeutic areas. Eris being a pure domestic play in selected

chronic therapies, we expect its growth to remain higher than the industry average.ERIS-8-5-18-PL.pdf (1.8 MB)

2 Likes

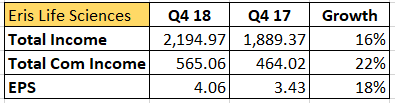

@Yogesh_s Eris Life has come with their Q4 results. Q4 YoY growth seems to be good compared to Q3 YoY. Can you please provide your comments.

1 Like

Results are in line with expectations. Not too happy with the fact that they are borrowing money for the long term for the Strides acquisition when they are sitting on liquid investments. Current year we will see if they are able to raise productivity of Strides MRs.

1 Like

I think the management mentioned that their treasury returns is similar to their borrowing rate. Hence, the borrowing.

The biggest impediment to my conviction is the stellar margins they have at the gross margin level, despite a lot of their manufacturing continuing to remain outsourced.

Also, when one looks at the same in the contex of the market share changes below -

| hba | Market | Market Size | Market Share | Rank | MS - 2017 | Launch Date | Revenue CAGR | Market CAGR | MS - 2013 | Rank - 2013 | Rank Gain / Loss |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Glimisave | Diabetes | 30913 | 1709 | 3 | 6% | 2007 | 29% | 18.6% | 3.9% | 2 | Loss |

| Eritel | Cardio | 19135 | 1022 | 4 | 5% | 2008 | 29% | 21.1% | 4.2% | 4 | Loss |

| Rabonik | Gastro | 12415 | 542 | 10 | 4% | 2008 | 9% | 14.4% | 5.3% | 6 | Loss |

| Remylik | Vitamins | 8428 | 530 | 8 | 6% | 2007 | 10% | 13.7% | 7.1% | 3 | Loss |

| Tayo | Vitamins | 10781 | 527 | 5 | 5% | 2011 | 8% | 23.4% | 8.4% | 2 | Loss |

| Olmin | Cardio | 7165 | 487 | 3 | 7% | 2010 | 36% | 19.2% | 4.0% | 3 | Loss |

| AtorSave | Cardio | 10365 | 377 | 6 | 4% | 2007 | 7% | 2.0% | 3.0% | 3 | Loss |

| LNBLOC | Cardio | 3322 | 360 | 2 | 11% | 2012 | 168% | 75.7% | 2.0% | 5 | Gain |

| Tendia | Diabetes | 3995 | 288 | 3 | 7% | 2015 | 448% | 352.0% | NA | NA | |

| Crevast | Cardio | 9141 | 230 | 6 | 3% | 2010 | 20% | 23.2% | 2.8% | 6 | Loss |

it can be observed that the company has been losing its prescription rank in almost all its top drugs despite it gaining market share in some brands, which indicates that the markets for all these brands continue to consolidate among the top players as the long tail of low MRP late entrants discontinue their product.

With double digit market share in only one of its top 10 drug, i have a low conviction on longevity of any of their brands, so giving this idea a miss.

8 Likes

ERIS Lifesciences Ltd

Highlights of Q1 FY19 results

Financials

- Consolidated Results

o Revenue grew by 35 % to 251 Cr compare to last year same quarter

o EBITDA grew by 24 % to 89 Cr compare to last year same quarter

o PAT had a very miserable growth compare to last year same quarter

Q&A - On the cost side , one is personal cost for the company in the standalone business has increased significantly. It was about 35-36 Cr gone to 43 Cr and similar kind of increase can seen in other expenses as well So what led this increase in numbers ?

o It is because of HR level increment which get affected in April so that is largely where company is putting cost on a sequential basis. On YOY basis there are two things which moved up , the other expenditure which is in the tune of around 22-24 Cr and the HR cost which is around 12-14 Cr. So in HR it is simple because of addition of people. For the other expenditure, there are two things, one is the last year base was absolutely low because the environment was such. The second reason is that there is some amount of frontloading in this year. This year is not something which is representative of all the quarters so it will sequentially getting corrected to an extent. - In frontloading , is it the variable contribution to the field force ?

o So it is not, the variables cannot be frontloaded much because they work on system, more of the marketing cost, the selling cost is frontloaded. - Kindly explain the YOY comparison because sequentially personal cost is also up 22 % So how does the sequential increase from 36 Cr to 44 Cr ?

o There is 3 Cr which is in benefit and rest of is in increment. It is on HR benefit, so incentive which has been filed up. These are one-time benefit cost and the rest is the year-on-year increment. -

Is this kind of bonuses which company give for the first quarter ?

o One time . It is at the run rate of 40-41

- The API factories are shutting down in China so how it is impacting the company and second question is on the tax rate before acquisition of Strides, they were around 3.5%-4%, whereas it is now around 8%-9% ? Company was also planning to transfer some of the production of the Strides portfolio to own factory which would reduce the tax rate and what is the situation on that ?

o Company do not have export business but company got impact on input cost because certain intermediaries or large part of intermediaries are imported from China so there is some effect on the cost side for the company .

o In tax rate currently after the Strides acquisition, around 40% of company products are being outsourced from third party and rest 60 % are self made so that are the reason for rising taxes. - Will the contribution from Guwahati moves up in coming quarter ?

o It would gradually go up when company will start, company have moved lot of work in Guwahati , they have not come into sales as of now, but this year 8-9 % should be the tax rate. - Is there any kind of slowdown in the Strides business ?

o When someone acquire a business, generally not everything is something which someone take forward So all businesses have certain amount of sale or certain product category which is not someone strength area and so for example strides is a business which works in hepatitis C , which company took as per the run rate that was around 15 Cr for the year. Now that business was an institution business where the gross margins were in the range of around 22%-25% and the net margins were actually in the zone of making no money at all. So company had completely taken out that business. So one part is which company have taken and which split in the entire business in it. The largest brand which is the Raricap , the Renerve as well as the neuro brand like Serlift, all of them both in prescription and in the sales are showing a very good positive strength… - How will company deploy the cash that generated from the business ?

o Net Debt is zero . In fact company has proponed certain amount of debt because the arbitrates was getting thinner by the day and capital employment, the philosophy remains. Company is still looking at something which can be acquire and grow plus all that money which will be required for organic business to grow the organic business. - What is the yardstick company use to justify or to evaluate an acquisition, is there any specific metric for deciding the buying price to acquire a business ?

o First it is about how much sense does it make to the business , for example this time there is a 27 Cr additional cost which has gone to other expenses and 12 Cr which has gone into HR so after adding 24 plus 12 which is 36 and put it on 90 which company is reporting that means , but just throwing a point that on an apple to apple basis that 61 could be 136. So what happens is if the business is on the right side in last quarter and this quarter company margins have also been stabilized so after consuming the entire portfolio, the gross margin has stabilized to 84-85%. So somewhere in this slot which gives a growth opportunity which really does not take a detour from what the financial metrics are and most importantly right with right therapy and right pocket - As strides gross margin was low so how company had reported a similar kind of margin even after acquiring strides ?

o Strides portfolio was not a bad portfolio In the gross margin company is saying that company has took it at 75 % gross margin. Within that 75, there were couple of areas. Like one of that is that it is illustrated from the Hepatitis C business point of view it was dragging it down. So that was simply one part. And the second part is that once these product get shifted company gain some more percentage point there - Can the margin of Strides business can go up because company has still not clearly shifted all the products Guwahati is now only 60% of sales. So company is not able to shift majority of products ?

o Yes because the biggest lever here is almost 80-100 crore brand in Renerve which company don’t have the facility as of now in Guwahati. So the day that actually shift then that would be a bigger lever than anything else which is now remaining. - So the central Government had actually some point in time said that they would want all the products that are non DPC or non NLEM products. They would want their price increases also to be linked with a WPI index, which will be more based on pharmaceutical components customized index for the pharmaceutical industry. And in non NLEM portfolio currently company is allowed to take a 10% price increase whereas if it gets linked to WPI then it will be restricted to the level of the WPI ?

o In a report there was mention that in the last one decade the price increment in the industry has only been 2%. Because in a silos company think that if this 10% allows, than company can take this 10% every time. But company operate in a real world where there is lot of competition, so competition anywhere has always been a bigger force than regulatory . And so it is not so clean that every year there is a 10% hike for sales. So what company have done in this point of time is far below 10%. And this is a trend which is a real market trend. So it will remain tactically in this door whatever the regulations are. - Does company had seen all the impact of China material inflation the current quarter or the cost inflation impact going forward in the coming quarters?

o That is very little part of portfolio so there will be no major impact. - Will the EBITDA margin will go up from current level ?

o Yes. there is a frontloading which has happened in this quarter, which is going to get even in the coming quarters. So that will always come in Going forward company HR will also swing between 40-41 Cr. So that extra will also come back. So both these components are going to reflect in the numbers going forward. - So the Net debt is Zero so does company has paid 100 Cr of debt till July ?

o Yes company had paid the 2 installments of 25 Cr and then prepaid 50 Cr more because the arbitrage of treasury, the other income in treasury were thin. - How will be the finance cost and other income going forward ?

o Other income will remain for next 3 quarter. because whatever is the increased treasury in liquid that company will use it for repayment. - How is the chronic side witnessing in the first 4 months of the financial year?

o First quarter the April-May-June was okay. But July company is seeing a very sharp turnaround and chronic grew by around 14% in the July and by all means this trend will continue. - How is the attraction looking at the Raricap and Renerve brands because the idea was that these are southern concentrated, in southern India and idea was to expand the presence across India. How has that been clocking and is there a thought of adding more therapy focus apart from the chronic diabetes and cardio that company have in CNS and women healthcare ?

o Things are working out in the right direction. Couple of prescription data points is showing double digit growth in prescription in both these brands which company is talking about and company will be entering into a couple . In fact company has signed an agreement with a company called Biopelle of USA for cosmetology, dermatology. So that’s something which will start happening in sometime from now. So in third quarter company have some more expansion and this will be in the skincare, cosmetology, dermatology and one more in the nutrition side. - Is there any planning of geography expansion ?

o Yes geography, it is stretching out well. So it is a mix of consolidation where it was failing and the stretch which is happening across. So metros have already started doing better and it is catching up. - From last 3 years the average revenue growth was 14-15 % . The numbers used to be about 7-8% volume growth, 2 to 3% price growth and 3 to 4% new product introduction. With the Indian government being more strict or rather more focused on the patent protection of the innovators, does company think the new product launch opportunity has declined meaningfully or is it the 7 to 8% volume growth which used to be there earlier, has that declined meaningfully because price is 2 to 3 % still. So what has declined meaningfully tripling the overall IPM growth down to 10 to 12% which was earlier used to be 13 to 15%?

o So between 13 to 15% and 10 to 12%, it is the base effect which had been climbing up. But the stratification which you gave is completely alright. But going forward the bucket will be start shifting from one to other. So there are too many products to be launched then the penetration in the existing products will actually make up for lesser launch. And this is the better strategy for the brands as well as for the industry. - In company prescription trends with the specialty practitioners and the consultant practitioners, are the prescriptions going double digit with those doctors and company as well ?

o Yes , the growth from the prescription point of view the growth is largely in line as per the industry. Company don’t see anything changing from this side to the other side even in the prescription data. - What percentage of total prescription would come from specialty and consultant practitioners?

o It was in vicinity of 90 % including Kinedex and Aprica - At the time of acquisition of Strides it was largely specialty or was it GP portfolio?

o No it was the prescription was largely specialty - Does some of the larger companies, Pharma companies in India have started partnering or in licensing products from MNCs and does it make sense to the company?

o Yes, it make tremendous sense for a company and help the organization and the management is working quite aggressively.

4 Likes

The Q result is avg not bad not good but due to the new acquisition (stride) and gets that nos in this quarter the comparison betn last Q and mid year revenue is showing difference or cant compare for now. Or is there any other unknown reason for this fall. BTW now the share price is at IPO level and its measure support @600.

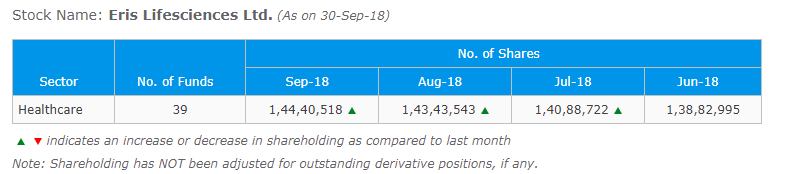

But a good sign that the MFs are continuously buying from last couple of months.

Abbott India on a sales base of 3200 Cr does an EBITDA of 600+ Cr and a PAT of 400 Cr. Majority of their production is outsourced and they have a single plant under the listed entity

Eris Life on a revenue base of 850 Cr does an EBITDA of 360 Cr and a PAT of almost 300 Cr. Majority of production here too is outsourced.

In terms of product portfolio too I do not see anything great about what Eris has, it is the usual therapy areas like CVS, CNS, GI, Gynac, Vitamins etc.

What is it about Eris that they are able to either get so high realizations or operate at a much lower cost compared to a company that has been in India for almost 4X the number of years and operates at 4X the scale?

I just cannot see the answer with a cursory glance, will look deeper over the next month or so, any insights on this in the meanwhile welcome

11 Likes

Eris’s manufacturing facility in Guwahati has zero tax till 2025 i think. Plus they have very good relations with specialist doctors.

That explains the high EBITDA to PAT conversion. However my Q is why is Eris able to pull off a 40% EBITDA margin while MNC’s which have a more mature and proven product portfolio are all working at lower levels? Other than Pfizer and Sanofi India, no one else is getting past the 25% EBITDA mark.

This can be viewed both positively and negatively. Question is whether this is sustainable and what prevents the other players with a similar portfolio from doing this as well? They have been in business longer, do higher volumes and have better known brands.

Industry leading EBITDA margins, highest growth while the rest of the market is happy growing at 12-15% and making EBITDA of 20% looks too good to be true/too good to last for too long.

On a different note, raising debt to buy the Strides Shashun India business while they are sitting on cash is a bit surprising. Strides has made some very strange moves in the past and keeps doing continuous M&A/divestment which I am just not comfortable with by nature. Anyone who gets into a deal with an M&A heavy company like Strides who does not need too much of a push to buy/sell businesses needs to be analyzed in detail.

I can see that some people on this thread have already voiced similar concerns. Has anyone done a detailed scuttlebutt and gotten opinions of the specialist doctors as to how Eris brands stack up against competition and how they seem to be getting such high realizations?

5 Likes