@devaki.tripathy You should substantiate your claim given @Yogesh_s has challenged authenticity of your data.

These are ERIS brands http://eris.co.in/leading-brands/ and check their prices .They are all lifestyle drugs and extremely cheap.

https://www.1mg.com/drugs/rabonik-d-30-mg-40-mg-capsule-sr-166331 .You can check the prices at this link .

Most of the promotors are Market Reps and in generic you only require marketing skills which they have in pleanty.

3 Likes

I think its high time to substantiate my argument with relevant facts.

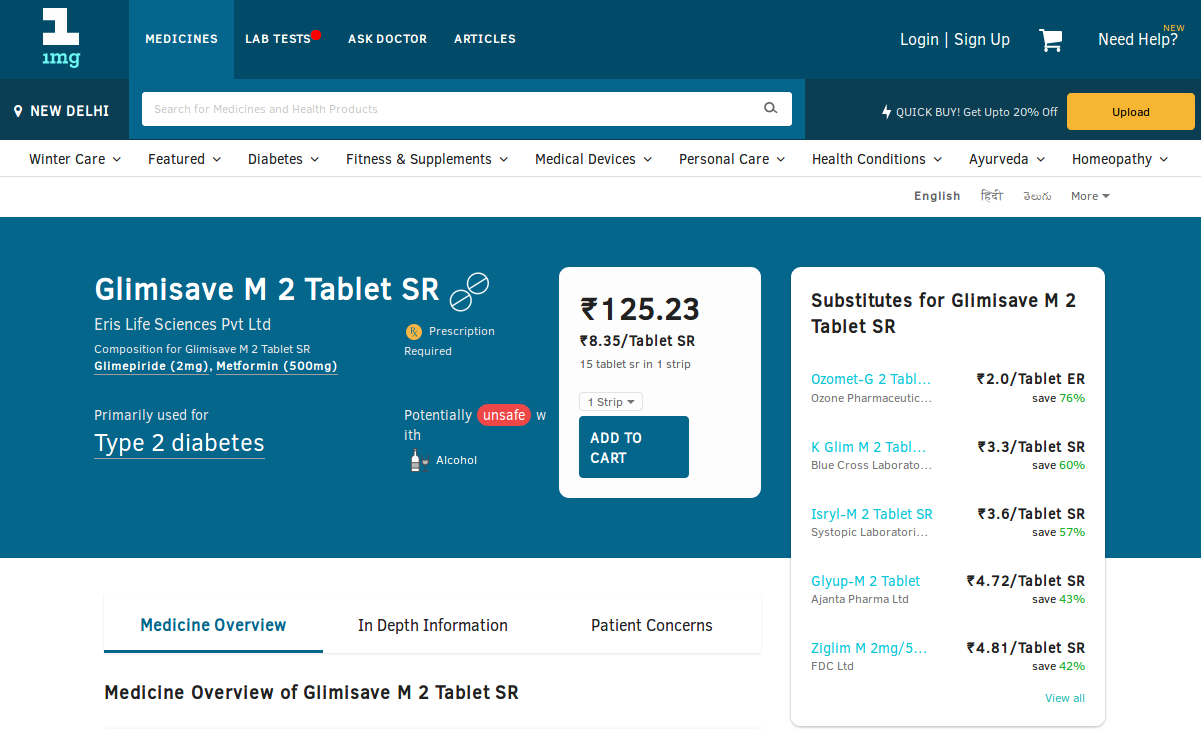

About Eris Life product pricing, here is what I found out. (Source : 1mg.com)

About Tayo and Rlemylin, these are just vitamin D supplements which are added to almost all calcium tablets by default and need not be taken separately.

The marketing strategy of Eris Life is simple. Take run of the mill generics and market them at exorbitant price in collusion with doctors and pharmacies. There is nothing wrong with this business model, only that its not being valued accordingly like a generic drug producer but more like a tier 1 pharma company with an impenetrable moat.

To give you an example, for the sake of argument, lets take the value of Lupin R&D pipeline, strong management with execution records, high reserves, leadership positions in multiple international markets, strong brands as ZERO and just compare Lupin’s domestic revenue to marketcap ratio with Eris. Even in this parameter Eris trades at a 20% premium to Lupin.

Is it justified? Is it rational?

Disc. Tracking positions in both Eris and Lupin. Views are definitely biased.

20 Likes

I check for Glimisave and Eric is actually costlier by around 40% when compared with similar product by Ajanta and FDC.

Thanks for d clarification…but if u read that what stride has said about margins…

Cant discuss all in open forum but in some brokerage reports on stride mentioned about single digit margins…so I just try to find out gap

I was thinking on investing in Eris Lifesciences. Below is thesis I was working on and what changed my mind.

- Eris is focusing on Chronic Segment which means the patient will need to take medicines for longer intervals

- They have tieups with specialty physicians who recommend the medicines of Eris

- Eris mainly concentrates in tier I and II cities as they have focus on lifestyle diseases and there are more patients in these type of cities for such lifestyle diseases

- Eris has started its plant in Sikkim and the plant utilization is at 30-40% and there is no significant capex required for further growth

- Company is growing its topline and bottomline at good rate and ratios are also good and that also with negligible debt

- Promoter is first generation entrepreneur who was very much successful salesman in the last organization he had worked(Intas Pharma) and started his own venture a decade back.

Now comes the scuttlebutt part. As the company has its HQ in Ahmedabad. I tried to check the background of the company with few of the pharma friends(infact this started in our Whatsapp group Vpickr for Ahmedabad)

- Company gives large amount of kickbacks to physicians. I found the same URL few konths back which has posted by @devaki.tripathy which reiterates the same. The physicians recommend these medicines and company keeps the prices at high level compared to its competitors and enjoys good bottomline

- Company was earlier doing contract manufacturing and doing just the labeling of the medicines. If you see the medicines are the generic ones and there is no R&D efforts which has been put

- The company started the plant recently to show that it has started its own manufacturing to showcase in IPO

URL

Here comes my conclusion

Management will try to show what it would like to show to the general public. Investors need to be smart enough what the management is trying to show and what it is trying to hide. Also, we will need to check the real reasons behind the growth, the numbers.

Disc: I have not yet invested in this company. My views were based on the discussion I had with friends in Pharma field and may there views may be biased about this company. Please do your own research.

16 Likes

Amit Bakshi sold just 0.5% of his stake in the IPO. If he had short term gains in mind, he could have cashed out. I think he is a good salesman/businessman and the issues mentioned by you are all fixable. Since their brands are now more or less established, they would not have to give freebies to doctors and can maybe bring down the prices gradually with increase in volumes. It was an acceptable practice in the past and now with more scrutiny this practice should decrease. Nothing stops the company from increasing its R&D efforts now.

From: http://www.forbesindia.com/article/12-hidden-gems/eris-lifes-sciences-drug-money/34025/1

In 2007, Eris Lifesciences entered this space with a strategy to identify gaps in super specialties in select categories, such as cardiology, gastroenterology, pediatrics, orthopedics—in the process creating new market segments. For instance, Vitamin D. New research shows it can keep liver and thyroid disorders, and even cancer, at bay. The Vitamin D market was Rs 18 to Rs 20 crore three years ago. In 2012, it added Rs 94 crore to Eris’ revenue of Rs 296 crore. The company has launched diagnostics for Vitamin D deficiency, and has eight such products in its portfolio, including suppositories.

Profile of Amit Bakshi:

disc - invested

4 Likes

Thanks. Had attended the concall and also read through the transcript once again but did not understand one point below:

Anubhav Agarwal**: Amit Bhai, based on the description that you have given for this acquisition, it looks like will it

be fair to say you expecting it to breakeven in just two quarters because that is what if the

gross margin expands and expiry date impact is nullified and the amount of MRs you arehiring, the productivity is already 90 lakhs already, so two quarter a breakeven or will it take

higher?

Amit Bakshi: I would say the breakeven is just around the corner, maybe the first month is a breakeven.

If the acquisition cost is 500 cr. and the annual sale is 180 cr. with c.13-14% EBIDTA margin for the Strides portfolio, how come the breakeven will happen in just 1 month?

1 Like

Anyone having research reports from Citi and Credit Suisse can please share?

Thanks for digging out the data. I can’t deny that some of the Eris’s brand variants are costlier than others. But I also found few other variants cheaper than or at par with other well-known brands. I don’t think Eris is pricing its products significantly higher than other well-known brands across the board. Some variants of some brands could be costlier while others are cheaper. what’s more concerning is that all known brand drugs are far higher than lesser-known brands.

To me it sounds like name brand drugs are costlier than lesser known brands because of related brand building costs which allegedly include kick-backs to the doctors. Eris could be little aggressive here because it is making inroads into the market but I think it could be gaining advantage over lesser known brands but not gaining any significant advantage over other well-known brands who also engage in similar practice. Even pathology labs engage in ‘cut’ practice and hospitals engage in overcharging. Looks like entire healthcare supply chain is milking their customers.

Although costs incurred in distribution should be added to cost of medicines, kick-backs cannot be justified. Ultimately these costs have to be paid by unsuspecting patients. However, mandating doctors to prescribe generics by their molecule name will only shift pharma-doctor nexus to pharma-retail nexus which will be far more dangerous. In developed world doctor prescribe salt and pharmacists (sometimes a vending machine) fills it with any USFDA approved supplier product. Patient never know which company manufactured the generic drug because USFDA ensure quality of product. In India, patient will end up asking the pharmacist which is a good brand for a molecule and the pharmacist is likely to push the one that provide highest margin. that’s a lot worse situation than doctor pushing a brand.

One reason costs can be jacked up is that they are still significantly low compared to rest of world. Eris also focus on mass market cheap molecules instead of pricey TAs like oncology. So a significant price erosion is unlikely.

6 Likes

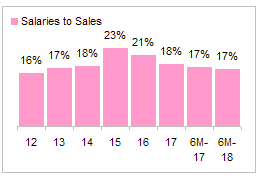

Looking at Eris’s expenses, employee costs as a % of sales have remained more or less at the same level for last 5 years which is reasonable as this is primarily a marketing company so employee costs will rise as much as sales.

Source: Capitaline

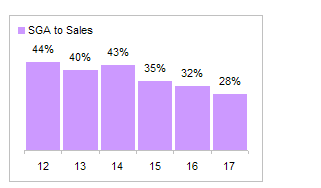

Sales Incentives (for the lack of a better word) should be booked as Selling General and Administrative expenses (assuming these are booked fully) and these are actually declining as a % of sales.

Source: Capitaline

This supports the argument that Eris may cut back on aggressive marketing as brands are established in the market. Lower SGA is largely responsible for growth in its margins.

Source: Capitaline

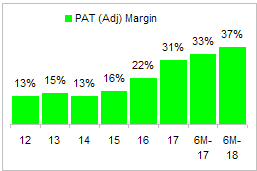

Margins are best in the industry and still growing. Strides deal is a cash deal on a slump sale basis so it is likely to be immediately accretive from Q3, This will have some impact on margins but Eris has a good record of improving productivity of its field force. So in the mid term, this deal is positive. It has about 400 Cr at the end of Q2 so not much debt will be needed to fund the deal.

6 Likes